Simply stated, an operating deficit is the result of a shortage of current income relative to operating expenditures during a fiscal year. The actions required to reverse a deficit—either cutting expenditures or raising additional revenue—are never easily accomplished, but they are especially difficult for nonprofit institutions. Cutting expenditures is problematic because nonprofit operating costs tend to rise at an unremitting rate. Increasing operating income is difficult because a significant portion of a nonprofit's revenues often comes from contributors who choose to restrict the use of gifts and grants to specific purposes. These restrictions force nonprofit institutions to do more than just balance the flow of funds into and out of their overall accounts. They must match various sources of funds with specific uses and carefully manage the growth of unrestricted income to ensure that there are adequate funds to pay for general operating expenses.

The financial struggles of The New-York Historical Society provide a rich and dramatic illustration of these complex issues. Expenditures at the N-YHS have risen steadily since World War II, and at a rate consistently higher than inflation. Revenue growth did not keep pace, and by the late 1960s, the Society was having difficulty balancing its budget. In the twenty-four years between 1970 and 1994, the Society suffered deficits nineteen times. These deficits put pressure on what had traditionally been the Society's largest and most reliable revenue stream, the income from its endowment, resulting in policies that sacrificed the endowment's future revenue-generating potential. This chapter reviews the key aspects of this evolution in an effort to draw out lessons of general importance to nonprofit managers and board members.

Since 1960, the total operating expenditures of the Society have increased at a nominal rate of 9.7 percent per year, which is equal to a real rate of 4.6 percent per year. This rate of growth is surprisingly high when one considers that the average annual growth in GDP over the same period was just 2.7 percent. By no means all of this growth in expenditures was the result of programmatic expansion. For example, between 1960 and 1970, operating expenditures at the Society more than doubled, from approximately $402,000 to $887,000,[162] even as the salaried administrative staff at the Society declined from forty to thirty-one persons.

Other than expansion, what else could account for the Society's high expenditure growth rate? Research has shown that costs for institutions with labor-intensive processes for producing "output" tend to rise at a rate faster than the overall price level. This phenomenon, often referred to as Baumol's disease or Bowen's law, is caused by the fact that productivity in labor-intensive industries does not increase as fast as productivity in capital-intensive industries. If wage rates and the prices of other inputs remain in relative balance throughout the economy, the unit costs for institutions with low productivity growth will rise relative to unit costs in general.[163] The Society's activities are unquestionably labor-intensive, and hence Bowen's law offers one explanation for the Society's persistent growth of expenditures over the years.

Although it is possible that there are purely internal explanations for the Society's rising costs, it is likely that the causes are primarily external. The strongest evidence for this is the fact that other nonprofit institutions share this tendency toward inexorable expenditure growth. A recent study of thirty-two prominent nonprofit institutions found that total expenditures rose at a nominal rate of 10.6 percent between 1972 and 1992.[164] Similarly, a study of five major independent research libraries (institutions very similar in many ways to the Society) showed that between 1960 and 1993, their total expenditures rose at an average nominal rate of 9.9 percent per year.[165] The data clearly testify to significant upward pressure on costs at these types of institutions. Given such pressures, it is unlikely that these organizations can hope to balance their budgets through sustainable decreases in total expenditures without significant reductions in services.

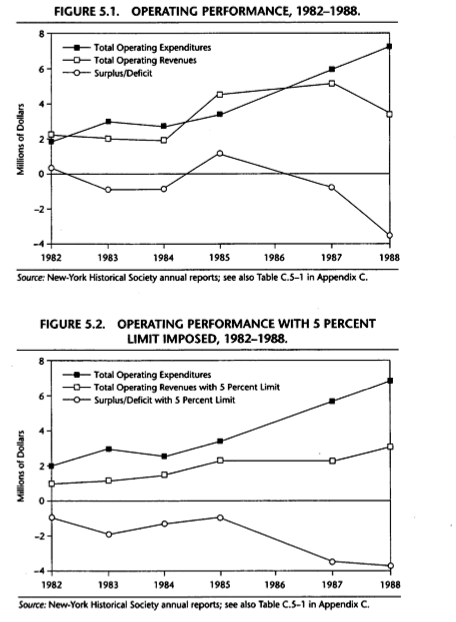

Further evidence supporting this assertion emerges from the Society's 1992-1993 financial crisis. Facing mounting deficits and a growing threat of bankruptcy, the Society cut operating expenditures by 17 percent in fiscal 1992 and by 20 percent in fiscal 1993. To accomplish these cuts, the Society reduced its total workforce from a peak of 125 employees in the 1980s to a skeleton staff of just 35 employees in early 1993. The Society closed its galleries and suspended all public programs. There is a limit, however, to how much an organization can cut, year after year. For organizations with valuable collections and fixed assets, overhead and other fixed costs exist that cannot be avoided. Even though the Society had drastically reduced programs and services, its total operating expenditures in 1993 were still $5.3 million.

Such austerity measures have consequences. Most important, it is extremely difficult, if not impossible, for an institution like the Society to generate significant contributed income while it is inactive. Such institutions are expected to offer exhibitions, public education programs, and community outreach services. After a certain point, reductions in expenditures decrease the capacity to generate revenue, both earned and contributed. In the case of the Society, the 1992 and 1993 cuts did not balance the budget; in fact, the deficit actually increased in 1992 and was still $1.5 million in 1993.

The implication of the unremitting pressure on costs is clear: if institutions like the Society are to remain financially viable for the long term, their revenues must grow steadily—and presumably faster than the overall inflation rate.

Generating revenues that keep pace with an ever-expanding expenditure base is made more complicated by the fact that all nonprofit revenues are not created equal. Unlike the for-profit sector, where dollars received can be used for whatever purposes management and the board may choose, nonprofit revenues often come with strings attached. A donor may stipulate that funds given to an institution be used only for a specified purpose, spent over an established period of time, or retained in perpetuity as capital. The types of revenues generated by a nonprofit institution can be as important as the absolute dollar values, especially in a time of crisis.

To recognize donor-imposed restrictions in the financial statements of nonprofit entities, a special form of accounting called fund accounting, which links resources and their intended use, was developed. Although straightforward in concept, fund accounting can be extremely confusing in practice. An attempt to clarify the mysteries of fund accounting would take us too far afield; however, there are two issues of broad importance that are illuminated by the Society's accounts. First, the distinction between restricted and unrestricted revenues is a fundamental fund accounting concept that, if misunderstood, can lead to serious confusion concerning the financial health of an organization. Second, the difference between current and capital financial flows, particularly as it intersects with principles of endowment management, continues to perplex not only observers of the nonprofit sector but also many nonprofit administrators and board members.

In 1988, Barbara Debs took over an institution in acute financial crisis. The Society had run deficits in eleven of the previous thirteen years, and its fiscal 1988 deficit was its largest ever: 83.7 million on a total budget of approximately $7 million. During her four years in office, Debs, her staff, and the Society's trustees managed to raise over $23 million—an extraordinary accomplishment. That success notwithstanding, the Society still ran significant deficits in each year. In fact, when Debs stepped down in September 1992, the Society was financially worse off than it had been when she assumed office. Although annual deficits had been reduced, endowment available to help pay for general operating expenses had declined, and the Society had incurred an external debt of $1 million.

The Society's fiscal 1990 financial records exemplify the complexities involved in trying to ascertain the financial condition of a nonprofit. In that year, the Society brought in approximately $11.1 million, while it spent only $8.2 million. Nevertheless, the Society had an operating deficit of $ 1.8 million. How did this happen?

The answer lies in the nature of the funds flowing into the Society and the fact that only a portion could be used to pay for ongoing operating activities. Of the $11.1 million raised, $2.4 million was a capital inflow, designated for the endowment. Since only investment income from an endowment can be used to pay for current operating expenditures (and then only if the expenditures match any restrictions), very little new money actually flowed to the operating account. Although the remaining $8.7 million could be categorized as current revenues, $4.1 million was restricted to specific uses. These funds were dedicated to such purposes as the Society's "Why History?" program, public outreach initiatives, library and museum collections conservation, and museum exhibitions. Only $4.6 million, 42 percent of the total funds raised, remained to pay for the Society's general unrestricted operations. Operating expenditures (including administrative salaries, building maintenance, utilities, insurance, security, consulting fees, and general administration) amounted to approximately $6.2 million. Hence the nearly $2 million operating deficit.

The relatively low percentage of revenue available to pay for unrestricted general operating expenditures in this instance is not at all unusual for a modern nonprofit institution. In recent years, funders have increasingly tended to make restricted grants, and often only to fund new programs and initiatives. As all nonprofit managers and trustees know, this trend is fraught with danger.

First, it can be difficult to ensure that total expenditures on a restricted program do not exceed the amount of money provided by a grant. Managing a restricted grant will use time and facilities that may not be fully covered, even if there is an allowance for indirect costs. Sophisticated cost accounting allocation estimates are required to get it right. Anything short of superior management of such a grant can end up costing an institution more money than it brings in.

Even if an institution is extremely well managed and has tight financial controls, restricted grants can encourage institutional growth or special projects that cannot be sustained. A recent report on the Society's library documented numerous examples of cataloging and preservation initiatives that had been started with targeted grants but could not be completed due to lack of funds.[166] It is difficult to rebuild enthusiasm for projects that are left only partially completed, no matter how important they may be. More dramatic are situations in which a new program is initiated for which staff must be hired. When the term of the grant expires and the funder has moved on to other priorities, the nonprofit institution has to deal with the task of either releasing employees or finding a way to continue the initiative with funding from other sources (including some unrestricted funds).

The Society has also exhibited clearly the most profound problem related to the distinction between restricted and unrestricted income: when funders want to provide only restricted grants, there may be no way to pay for the basic costs that keep an institution alive. This problem generally becomes even more pronounced when an institution begins to encounter financial difficulty. Typically, donors are unlikely to offer unrestricted funds to institutions perceived to be in trouble because of a very real fear that the funds will serve no long-run purpose. Of course, this sequence of events represents a vicious circle: the institution got into financial trouble in the first place because of a lack of unrestricted resources.

This study has documented numerous ways in which nonprofits differ from their for-profit cousins, but a fundamental need they both share is the need for cash. In the corporate world, it is not losses that put companies out of business but rather a lack of cash to pay creditors. For nonprofits, it is usually a lack of unrestricted funds to pay employees that closes the doors. For nearly a year leading up to the closing of the Society in February 1993, its leaders desperately searched for cash that would enable it to stay open. First, a $1 million loan was secured from a private foundation, funds subsequently rolled over into a debt assumed by several members of the board. Later, a $1.5 million loan was negotiated with Sotheby's. Meanwhile, the Society removed all board-designated restrictions from funds and applied for cy pres relief from the courts in order to use certain special funds. As long as the Society was able to find cash, it could remain open. The Society's story implies that nonprofit institutions need to be every bit as expert, if not more so, at managing cash flow as their for-profit counterparts.

The fact that the Society delayed its closing by finding cash through loans and other means was by no means an entirely positive development. These loans were obtained even as the Society continued to run significant operating deficits. The natural consequence was that the Society continued to dig itself into a deeper financial hole. Simply put, it is one thing to borrow money to cover temporary shortages of cash when one can predict future receipts with confidence; it is quite another to borrow cash simply because one has run out of it.

Beyond the distinction between restricted and unrestricted revenue streams, there are also different types of unrestricted income. The major sources of nonprofit operating income can be broken down into four categories: earned income, government appropriations, private contributions, and investment income.[167] Is there a proper balance among the various forms of unrestricted revenue for particular types of institutions? If so, what are the implications for the "marketing" strategies that should be pursued?

Over the course of its history, the Society has depended almost exclusively on private contributions to support its activities. As was explained in Chapter Nine, the Society's collections do not generate revenue, so earned income has never played a major role. Earned income from such things as admissions, contributions, royalties on publications, gift shop sales, and facility rentals have averaged only 8 percent of total revenues since 1960. As for government support, except for $2.6 million in transitional funding appropriated following the Society's 1993 crisis, the public sector has provided essentially no unrestricted support in recent times. The responsibility for supporting core operations of the Society has fallen on private giving. The annual revenues from these gifts break down into two different forms: (1) investment income earned on previous endowment gifts and (2) unrestricted contributions.

Before discussing the implications of these two types of income streams, it is important to point out that when private contributions are received by an organization, its board may have some discretion in determining whether each gift should be categorized as a current gift or a capital gift. For the most part, unrestricted gifts are spent when they are received; however, when an organization receives a large one-time gift or bequest, the board should consider categorizing the gift as capital and adding it to the endowment. After all, the large bequest is not truly operating income; it will not be received in subsequent years.

An example will help emphasize the importance of this point. Over the course of eighteen months in 1985 and 1986 (the Society converted to a June 30 fiscal year in 1986), the Society received more than $2 million from the estate of Clara Peck. The cash received from this gift was recognized by the Society as current unrestricted operating income. Consequently, in the year-end statements for 1985 and 1986, the Society registered a significant surplus.

Technically, there is nothing wrong with representing the gift in this way; however, this characterization of the Society's financial activity can have undesirable consequences. From an internal perspective, the additional income can relieve the pressure on Society staff, thereby lessening their resolve to control expenditures and maximize other revenue sources. From the standpoint of an uninitiated outside observer, such a representation could lead to the erroneous conclusion that the Society had finally brought its recurring expenditures in line with revenues. As soon as the Peck bequest had been spent, the Society was running large deficits once again.

The decision about the proper way to treat large one-time gifts comes down to a question of timing. By spending the Peck bequest in its entirety, the Society chose to emphasize current spending over future revenue-generating potential. A similar question of timing must be faced by a board as it contemplates how best to manage its endowment, an important issue to be addressed later in this chapter.

Although investment income and unrestricted contributions both come from essentially the same source (private benefactors), maximizing the value and growth of these revenue streams involves distinctly different management processes and depends on different factors for success. For example, once an endowment has been established, the revenue stream derived from that financial base should be relatively predictable. If the endowment is invested and managed wisely, it has a good chance of growing at a rate exceeding inflation. Unrestricted contributions, by contrast, are a far more volatile revenue source. If an institution somehow falls out of favor, contributions can decline precipitously. Moreover, increasing these contributions on an annual basis requires extraordinarily loyal supporters, perseverance, and fundraising skill.

Obviously, other things being equal, all nonprofit managers would like to have a large endowment base to support their operations. This is rarely possible. Moreover, looked at from the broad perspective of the well-being of the nonprofit sector, it may not be desirable. For some institutions, their characteristics and the nature of their missions make having an endowment important; in other situations, this is less appropriate. It is in the best interest of society to concentrate the limited capital resources available in those institutions that need endowments the most.

Compare, for example, The New-York Historical Society and a dance company run by its founding choreographer. The dance company's principal asset is the creative gift of its founder. Though it is possible that the founder can institutionalize his or her talent through training young dancers and choreographers, in many cases, this does not happen. The "product" is more ephemeral and is validated by the contributed support it receives on an annual basis, as well as through ticket sales and other forms of earned income. By contrast, the Society's library and museum collections are not ephemeral; they are material objects that constitute an irreplaceable resource. Although few people question the cultural value of the millions of manuscripts, books, prints, and other historical documents and artifacts held by the Society, they are not the kinds of assets that inspire and excite contributors. The effort of the Society to generate private contributions, especially over the past five or six years, illustrates that fact. An institution like the Society needs a source of support that both matches the inert nature of its collections and has the potential to grow at least as fast as its expenditures. It must have an endowment.

The importance of endowment to the Society's long-term financial viability makes the events of the past twenty-five years especially tragic. In 1969, the market value of the Society's unrestricted endowment was $15.7 million, a figure 21.5 times larger than that year's total operating expenditures. Investment proceeds from the endowment exceeded the Society's total operating expenditures. Even if the Society had not generated a single dollar of contributed or earned income, it would have had an operating surplus.

By 1989, the Society's endowment base had been almost totally eradicated. Nominal endowment had fallen to just $5.5 million, $1 million less than that year's annual total expenditures. Whereas investment income accounted for 91 percent of total revenues in 1969, it represented just 13 percent of the total in 1989. Obviously, the magnitude of this decline has the most profound implications for the Society. Documenting the causes of that decline offers a classic illustration of the complex and sometimes confusing issues that endowed institutions face as they strive to balance the need for current income with the desire to protect the real value of their endowments over time.

The growth of an endowment depends on three primary elements: investment performance, the addition of capital gifts, and the amount of investment income spent on operations or otherwise drawn down. Before addressing the Society's experience in each of these categories, it is helpful first to summarize briefly some basic principles of endowment management.

The return on a capital investment has two fundamental components. The first component, the current return or yield, usually comes in the form of dividends and interest and can be spent without affecting the nominal value of the capital base that generated it. The second component, capital appreciation, is not fungible unless some part of the underlying capital asset is liquidated. Selling units of capital generates realized gains or losses, which are the difference between the selling price and the price at which each unit of the capital in question was purchased (or if a gift, the market value at the time it was received).

In the 1960s, most institutions, including the Society, operated under the assumption that it was inappropriate to "invade" the principal of the endowment by spending realized capital gains. Only dividends and interest generated by the portfolio could be spent. As operating costs rose, so did pressure to generate more current spendable income. For many institutions, maximizing current yield became their investment managers' primary objective. This emphasis on current returns led many managers to sacrifice the long-term growth of their investment capital.

In 1967, the Society adopted a "total return" investment policy for its endowment. The primary objective of this policy is to maximize the total return on the portfolio, independent of whether that return comes in the form of interest, dividends, or gains from capital appreciation. A total return approach is based on the premise that the decision regarding how much of the total return should be spent in a given year can and should be separated from the decision about what assets the portfolio should be invested in.

A total return investment policy must always be paired with a spending rate, a formula that governs what percentage of the market value of the endowment can prudently be spent on operations in a single year. Established by an institution's board of trustees, the spending rate should strike a balance between short-term spending needs and long-term capital growth. In order to increase the predictability and reduce the volatility of the investment income stream, spending is usually determined by multiplying the spending rate by a multiyear moving average of the value of the endowment or by using some other smoothing mechanism.

The failure of the Society to protect its endowment can be attributed to a mix of factors. The following analysis reviews the Society's performance in each of the three areas of endowment management.

The Society was a leader among institutions of its kind in adopting a professional approach to the management of its investments. In 1964, during the presidency of Frederick B. Adams Jr., the Society hired Fiduciary Trust International, Inc., to manage its investments. Fiduciary Trust remains the Society's investment manager today. Overall, the performance of the Society's investments has been in line with market indexes. Since 1980, the Society's total fund has earned a compound annual return of 12.4 percent. This figure compares with a compound annual return of 13.5 percent for the Standard & Poor's 500 and a 15.1 percent return on the Dow Jones Industrial Average.

Table 10.1 shows the Society's annual investment performance from 1981 through 1993 as compared to total annual return benchmarks published by Cambridge Associates.[168] The table reveals that the performance of the Society's portfolio was quite respectable. It is clear that the erosion of the Society's endowment during the 1980s was not due to poor management of the investments.

The second element of a comprehensive endowment management policy is capital fundraising. New gifts provide a boost to an institution's financial base when investment returns are good and help it maintain that base when they are not.

For institutions dependent on endowment, the 1970s were extremely difficult. The loss of endowment principal in the early part of the decade, coupled with high inflation, fundamentally altered the budgetary equation. Investment returns were falling just as costs were rising, and deficits became the rule. The historical narrative presented earlier documents not only the Society's mounting deficits but also its poor record of private fundraising. Capital fundraising was no exception.

Given the struggle to balance the operating budget, it should come as no surprise diat the Society did not raise capital gifts during this period. Except for 1977, when capital gifts totaled $259,000, the Society raised a total of just $85,000 in sixteen years, an average of just $5,300 a year.[169]

The final element of endowment management concerns the use of investment returns to help pay operating expenses. When the Society adopted a total return philosophy in 1967, the spending rate established by the board of trustees was 5 percent of the three-year moving average of the market value of the unrestricted endowment.

An example will help illustrate how a spending rate works in practice. At the end of 1971, the three-year moving average of the market value of the Society's endowment for 1969, 1970, and 1971 was $13.88 million. At a spending rate of 5 percent, the Society was authorized to spend $694,000. Dividend and interest income, however, amounted to only $450,000. To make up the difference, the Society spent an additional $244,000 of realized gains and thereby reached the authorized spending limit.

An estimate of the Society's total return in 1971 is 16.4 percent.