Credit Scoring

You've Heard of Credit Scoring, But What Exactly Is It?

Credit scoring is a scientific method that uses statistical models to assess an individual's credit worthiness based on his or her credit history and current credit accounts. Credit scoring was first developed in the 1950s, but has come into increasing use in the last two decades.

In the early 1980s the three major credit bureaus, Experian, Equifax and Trans Union all worked with the Fair, Isaac Company to develop generic scoring models that allow each bureau to offer a score based solely on the contents of the credit bureau's data about an individual. Creditors, especially those in the mortgage industry, frequently use the scores when deciding who receives loans. They can order your score, commonly called a FICO score, from one of the bureaus, but it only draws upon information from your credit report.

Now individuals can use credit monitoring services and see the same scores lenders use when deciding whether to give you that loan. Along with your personal credit score, you can also received personalized analysis and tips that can help you improve your credit rating.

What Does It Mean?

Each credit bureau has its own unique system for compiling credit scores. However, the scoring models have been normalized so a numerical score at one bureau is the equivalent of the same numerical score at another. Thus, a score of 700 from Equifax indicates the same creditworthiness as a score of 700 from Trans Union or Experian, even though the calculations used to determine those scores are different at each bureau.

A computer-generated score is compiled using information from an individual's credit report, such as how much money is owed and whether payments have been made on time. Then that score is compared to the credit performance of consumers with similar profiles. The scoring system awards points for each factor that helps predict who is most likely to repay a debt. A total number of points (the credit score) helps predict how likely it is that you will repay a loan and make payments on time.

Credit scores range from 375 to 900 points, but those numbers means little on their own. They become meaningful and useful within the context of a particular lender's own cut off points and underwriting guidelines.

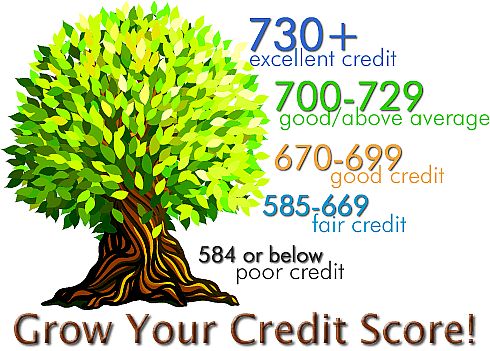

What’s A Good Score?

In general, you are likely to be considered a better credit risk if your FICO score is high. Under mortgage lending guidelines, for example, a score of 650 or above is considered high and regarded as an indication of a very good credit history. People with these scores will usually find obtaining credit quick and easy, and will have a good chance to get it on favorable terms.

Next… scores between 620 and 650 (average FICO scores fall into this range) indicate basically good credit, but also suggest to lenders that they should look at the potential borrower to assess any particular credit risks before extending a large loan or high credit limit. People with scores in this range have a good chance at obtaining credit at a good rate, but may have to provide additional documentation and explanations to the lender before a large loan is approved. This means that their loan closing may take a little longer, making their experience more like that of borrowers in the days before credit scoring, when every individual was researched.

A score below 620 may prevent a borrower from getting the best interest rates, as they may be considered a greater credit risk-but it does not mean that they can't get credit or will be automatically turned down… but they definitely will not be automatically approved either. Their application will be scrutinized much more closely and the process will probably be lengthier and, as noted, the terms may be less appealing, meaning they are usually charged a higher interest rate. But often credit can still be obtained.