Our Government and the main street media don’t want to talk about the retirement crises that’s unfolding right before our eyes. They don’t want to shine a spotlight of truth on the looming retirement train-wreck in America.

Why you ask? They don’t want to scare everyone to death. Make no mistake about it. It’s out there. If you listen quietly and pay attention, you’ll hear it. It’s coming. And coming fast. It’s like an out-of-control freight train. And it’s headed right for us. And if you don’t prepare for it, it’s going to slam right into you.

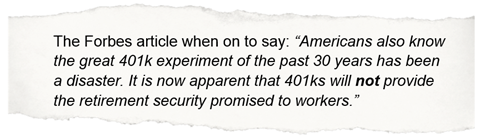

Forbes.com ran an article on 3-20-13 called “The Greatest Retirement Crisis in American History.” The article stated, “We will witness millions of elderly Americans, the Baby Boomers and others, slipping into poverty. Too frail to work, too poor to retire, will become the ‘new normal’ for many elderly Americans.”

The average 401(k) balance for 65 year olds is estimated at $25,000 by independent experts, (or $100,000 if you believe the retirement planning industry). Economics Professor Teresa Ghilarducci estimates that 75% of Americans nearing retirement in 2010 had less than $30,000 in their retirement accounts.

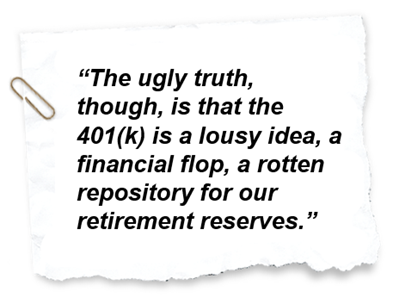

Did you see the TIME Magazine cover, “Why It’s Time to Retire the 401(k).” In the article it said;

In this eye-opening article, they also spoke of what they thought was the solution. We agree with their recommended solution, but more on that in a bit.

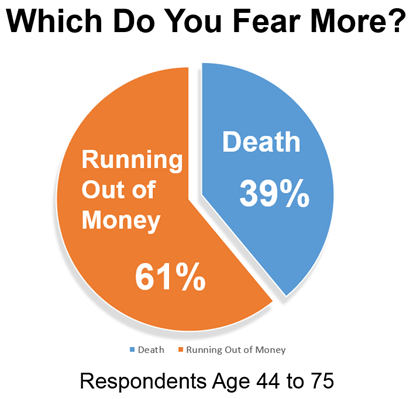

I know this is some seriously scary stuff. Most Americans are vastly unprepared for retirement and for some, they’re literally scared to death. In fact, check out this recent survey. It found that 61% of Americans FEAR running out of money when they retire MORE than they fear death itself! Wow. Is that a sobering statistic or what?

60 Minutes ran an eye-popping story about what a huge disappointment 401(k)s have been and how they have failed so many Americans.

I encourage you to take a few minutes and what this shocking 60 Minutes story. You can view it by going to: www.BarefootRetirement.com/60minutes

A massive 28% of the American population are baby boomers. Some reached retirement age a few years ago. Now 10,000 baby boomers are retiring every single and every day. Even so, the vast majority of boomers are not yet there. There are 88 million more boomers on the way. That’s a good thing because most of them are nowhere near ready for retirement.

Heck, over half of all Baby Boomers are still supporting their adult children. Others are supporting their elderly parents. How are they supposed to adequately save for their retirement when they’re still supporting others and trying to survive themselves?

Make no mistake about it. There IS a retirement crises in America. As it plays out over the next few decades, people are going to be shocked at how dramatically this is going to change our way of life.

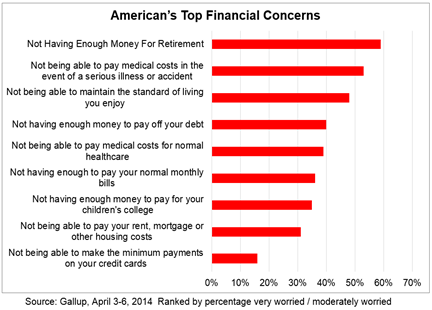

Here’s another survey by Gallup that shows you how the fear of running out of money during retirement stacks up against the other fears out there:

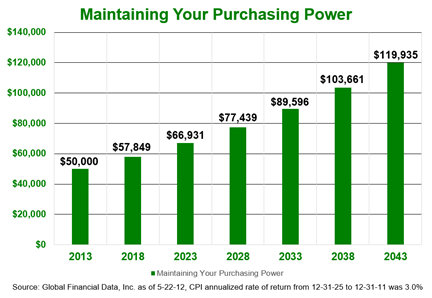

Another challenge we all face is inflation. Too many people don’t stop and seriously consider the longer-term effects of inflation. Especially if you’re on a fixed income. Since 1925, inflation has averaged 3% a year. (Source: Global Financial Data, Inc.)

As you can see in the chart below, if you had an income of $50,000 per year in 2013, you would need to have an income of $89,596 to maintain the same purchasing power just 20 years later. When planning your needs during retirement, be sure to factor in inflation.

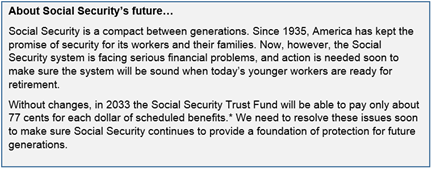

As I’m sure you know, many financial and economic experts both inside and outside of our Government have expressed doubt about the Social Security program and its ability to survive long term. If you are counting on Social Security as one of your main sources of retirement funds, it may be wise to seek some other options just in case these experts are right.

In fact, most people never even notice this, but this is the exact statement you will find on the very first page of your 2014 Social Security statement:

Two points on this. First, if this is what the actual agency is saying about their own financial health, it leads one to wonder just how accurate this is. The Government seems to be handing out the “Free Government Cheese” as fast as they possibly can, to everyone they can, regardless if they are legal US citizens or not. So at the rate they are burning through all of that Government money, it makes you wonder how long the Social Security Trust Fund will really last.

Second, it stinks that the Government promised you this benefit and will, in all likelihood, not be able to come through with it. You have done what was required of you and paid a lot of money into the Social Security system. You upheld your end of the bargain. Now you get the short end of the stick. This is especially bad for younger people. They will have to continue paying their full amount into the system knowing full well that they may not receive anything back in return for it. So if you are relying on Social Security for your “Retirement Program," you may want to take matters into your own hands and develop a Plan-B, just in case.

You’ve probably heard about all the pension fund problems there are with Government pensions as well as some corporate pension programs. Hopefully, they will survive and thrive but their future is looking dim.

Pension plans are similar to Social Security in that they are nothing more than promises that can be broken.

During the years from 1996 through 2007, 25% of all the Fortune 500 company pension plans have been terminated, closed or frozen. That’s a staggering number.

In a study conducted by Hewitt Consulting (now Aon Hewitt) it was found that if the same rate of decline in pension funds that occurred from 2002 through 2008 continues, (something the company considers unlikely), there will be no more open-plan pension funds in the Fortune 500 by the year 2019.

I sat beside a guy on a flight years ago, who was one of the top Federal officials in charge of the Federal Pension Benefit Guarantee Corporation (PBGC).

A lot of people feel a great sense of security knowing that the PBGC is there to back them up in case their employer’s pension fund goes belly up. I remember how shocked I was when this fellow told me about the tiny fraction of pensions that they could bail out if there were large numbers of pension failures. It would be like trying to bail out the ocean with a thimble. If the problem is small, they can handle it. If it becomes widespread, you had better have another plan.

Most middle and upper-middle-class Americans are pretty much in the same boat and have been down the same pathway. We’ve been faithfully following the rules and doing what all of the “experts” have been telling us.

Things like: “Contribute to your IRA, invest in your company 401(k), invest in solid mutual funds, stay the course, buy and hold, hang in there, keep the faith, just keep on investing and over time, the stock market will deliver the best return, and you’ll be able to retire comfortably and enjoy your retirement years the way you deserve to.”