I Got Sick and Tired of Being Sick and Tired.

I got tired of being whacked down every time I started getting ahead. I was feeling like I was a little pawn in a giant chess game, and the big guys were just using all of us in their economic games. I finally had enough. Plus, I was running out of time. After all, how many 40% to 50% hits can you take to your life savings and still be able to retire as you had planned?

Did you know that it takes a 100% gain to recover from a 50% loss? It’s true. Also, a 50% loss will wipe out a 100% gain. How long do you think it takes most people to recover from a 50% loss? As I am writing this (Summer of 2014), it has taken from July of 2009, until now, for the DJIA (Dow Jones Industrial Average) to climb back up approximately 100% to where it was in July of 2009. That’s almost 5 years, and that was during a good stock market time period. And that’s just to break even and be in the same place you were about 5 years ago.

Plus, you can never get those years back nor their lost earning potential. My investment friend who lost 65% would have only recently gotten back to where he was almost 6 years ago if he stayed in the markets. Who wants to delay retirement plans that long? Playing catch up all the time just plain stinks.

Yep, let’s not forget about our old friend inflation. If you go to:

www.usinflationcalculator.com you can see that we’ve had over 10% inflation since 2009.

Plus, we’ve had a whopping 37.2% inflation since the year 2000. That takes a huge bite out of your dollars’ purchasing power!

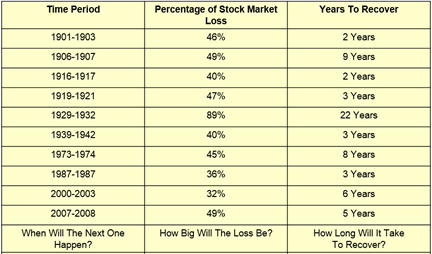

When you’re planning your retirement, timing is everything. Take a look at the chart below. We know for sure that every so often, the financial markets crash. They then take years to recover. If you’re young, time is on your side. If you’re nearing retirement, a loss such as the ones shown below can be devastating, and can turn your retirement dreams into a nightmare, overnight.

Losing money stinks!

Losing 47% every 11 years, is downright stupid.

And, these kinds of losses will keep you from having the retirement you want and deserve.

The best single thing we can all do to preserve our wealth and, best prepare for retirement is to faithfully follow Warren Buffett's #1 rule for investing success.

Seriously, if you’re trying to plan for something as serious as your retirement in an environment like this, how can you succeed?

The truth is, you can’t.

If you’re an average person playing by the mainstream rules that Wall Street, and the major investment firms are encouraging you to play by, you won’t win, and you can’t win.

This is often true. Many wise investors know, according to the Standard & Poor’s, over 99% of mutual funds consistently under perform the S&P 500 Index. That’s why a lot of smart investors put their funds into something like a Vanguard S&P 500 Index Fund. It has a low expense ratio, and simply follows the S&P 500 index, which outperforms 99% of the managed mutual funds.

How SAFE are you feeling about being in the markets now?

Take a look at the chart below. It shows the performance of the S&P 500 from the year 2000, up until summer of 2014. Around the year 2000, the S&P 500 began a decline which ended in a 48% drop. Around 2008, the index began a decline which ended in a 56% drop. (Some people call these drops, retirement killers.) Take a look at where it is now. It certainty looks like the S&P 500 could begin another huge drop, at any time now. Don't you think?

Here’s the problem. People have been saying the same thing every day, since 2011. Since that time, a lot of “experts” have been telling people to get out of the market NOW, before it falls off a cliff again. Had you taken their advice, and gotten out back then, you would have missed a huge up-side gain. Most of us are the same. We don’t want to miss the up-side gains, but we are also scared to death, that it’s going to crash again, and we will lose another 50% of our portfolio. Who can afford to go through that again?

I’m here to tell you there is a better way. A MUCH better way. The Barefoot Retirement Plan allows to you participate in most of the up-side gains… and TOTALLY eliminates any and all losses due to market declines. With our program, you don’t have to watch the financial channels 24/7, and worry about when the next crash will really happen. You just relax and live your life. If the markets go up, your account will go up. If the markets crash, you are completely safe due to market downturns.

Caution. Please don’t wait too long to get your Barefoot Retirement Plan set up, and in place! You don’t have to be a financial guru to look at the chart below, and tell we’re way overdue for another big correction, and/or crash.

Jeremy Grantham, co-founder and chief investment strategist of GMO, a Boston-based firm with $117 billion in assets under management, was recently quoted as saying, “Another horrific stock market crash is coming, and the next bust will be “unlike any other” we have seen. We have never had this before. It’s going to be very painful for investors.”

You can choose not to participate in the next big crash.

When you finish reading this book, you’ll have more information than about 99% of other Americans have, on how to protect yourself, your family and your retirement. Don’t wait until it’s too late. Give us a call today, and let’s take the first step to getting you protected.

“If I had to give advice, it would be keep out of Wall Street”

John D. Rockefeller

According to Dalbar, Inc., the nation's leading financial services market research firm, over the last 20 years the average equity mutual fund investor has only earned 4.25% per year. (Asset allocation funds and fixed-income funds performed dramatically worse over this same time period.) That is less than half the return that the S&P 500 returned over the same time period. Plus, that 4.25% return only beats inflation by a puny 1.28% a year.

Morningstar conducted a similar study, and the results were even worse. A 12.01% mutual fund return over 6 years, resulted into an actual return of just 2.2% for investors.

If you find this interesting, I found a great little website, I think you will like. You simply enter any date range you want, and it will show you the AVERAGE returns versus the ACTUAL returns of the S&P 500. Plus, if you check the little box that says, “Adjust for Inflation,” it will make you want to cry. Most of us don’t want to really think about our actual returns because it makes us feel like a looser. Like a failure. If you want to build wealth, you just can’t do it with the puny actual returns that average investors achieve. To check out the site, go to: moneychimp.com/features/market_cagr.htm

Let’s not forget about all the fees that are charged by the various mutual funds and financial institutions. Some financial analyst estimate that over 90% of all financial advisers and planners can't even beat the S&P 500. In spite of that, you still get to pay all the relentless fees they charge for such poor performance.

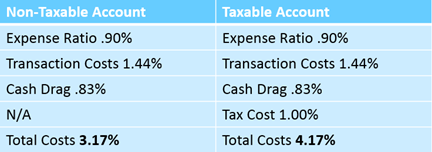

Most people don’t even realize this is going on. Forbes.com featured an article by Ty A. Bernicke, CFP where he did an in-depth analysis of mutual fund fees. The article was titled: The Real Costs of Owning a Mutual Fund. His findings are summarized below, and I think they speak for themselves.

Below is a summary of quantifiable costs and fees of the average mutual fund. The advisor costs and soft dollar costs are not included below due to the wide range in advisory fees and the difficulty of quantifying the soft dollar costs. If you work with a financial advisor, it is most important to add the advisory fees to the costs listed below to get an accurate view of your total potential costs.

Over your life time, fees like this can absolutely kill your retirement. When you look at the average real returns investors are earning and the fees that are charged, it’s enough to make you sick.

Demos, a public policy organization recently estimated that over a lifetime, a median-income two-earner family will pay nearly $155,000 in 401(k), and IRA fees. This amount consumes nearly 1/3 of their ENTIRE investment returns. Higher-income dual-earner families pay as much as $277,969 in these types of fees. No wonder if feels like the deck is stacked against you.

• 50% of Americans can’t afford to save money for retirement

• 1/3rd have ZERO saved!

• 63% of your wealth is eaten up in fees over 5 decades.

• Average family will pay $155,000 in FEES to a 401k plan.

• 79% of mutual funds don’t even beat the S&P 500.

John Bogle is the founder of Vanguard, the largest mutual fund company in the world. He is on record for saying, “Fund investors do not earn the full market return… because fund investors incur costs, and costs are subtracted directly from the gross returns funds earn.” Bogle also said this about the 1990s bull market, “The 6.5% annual return earned by fund investors was 3.3% behind the 9.8% annual return reported by the funds themselves.” Funny that they don’t advertise the fact that investors made 1/3 less than what the funds show as their earnings.

Heck, just last month CBS 60 Minutes featured a story titled: Is Wall Street a Rigged Game? Michael Lewis thinks so. In the financial writer's new book titled Flash Boys, he blasts the so-called high-frequency traders he says are gaming the market. It’s always the same-old story. The big guys win and screw over the little guys.

The story revealed how the big banks, stock exchanges and high-frequency traders have spent billions to game the system by using a technique called front running. They have sophisticated systems in place that can sniff out slower trades, jump in front of them, and make additional profits on the trades you are placing. These systems insure they win on every trade. These front running trades happen 100 times faster than the blink of an eye. Believe it or not, this is all perfectly legal. They went on to say that human beings have now been completely removed from the market place.

Wall Street is starting to look more like professional wrestling these days. You know it’s fake. You know it’s rigged, but some are still drawn to it. How can any average person, with average intelligence, and average information win in a rigged game like this? The truth is, they can’t. Many of my friends now call this rigged stock market, The Wall Street Casino, and I agree with them.

Even though we are currently in one of the longest and strongest bull markets in history, US stock ownership is at a record low. Although less than half of Americans trust banks and financial services, many are forced to turn to fixed income options. Due to the government's low interest rate policy, fixed investments like money markets, CDs, etc. that used to pay solid guaranteed returns, NOW only pay a tiny 1% to 2% or so in returns.

Everyone knows itty-bitty returns like this, just won’t cut it, and they certainly won’t help you reach your retirement goals. Plus, after you factor inflation into the mix, you’re really going backwards. And if you’re just fed up with it all and decide to leave your money in a bank savings account, they’re currently only averaging 0.06% interest, according to CNN Money. Over the last 24 years, our program has produced an average annual return of 9.28%. That means our program has produced 154 times more than the banks are now paying you!

If you choose to put your funds into a qualified plan like an IRA, or a 401(k), you are voluntarily choosing to subject yourself to an unending amount of restrictions, limitations, penalties, and requirements. They offer you the “cheese,” in the form of being able to put before taxed dollars into your retirement accounts. After you take the cheese, the door slams shut, and you are then locked in to all the requirements and restrictions imposed by these programs.

After all, have you actually read all the rules, regulations, requirements, restrictions, and legalese about these programs? They are similar to the tax code, in that they just go on, and on, and on, with a seemingly unending amount of rules, regulations and restrictions.

Putting your money into traditional qualified plans is somewhat like voluntarily locking your money up in money jail. Once they are locked up, they are then subject to these rules. You lose a good deal of your freedom-to-choose, and to make your own financial moves, based on your individual and unique needs. When you choose to put your money into these qualified plans, you are basically putting the Government in charge of your retirement.

When you voluntarily lock up your money in the usual qualified plans, you are subjecting them to a great deal of limitations and restrictions such as:

• Limited contribution amounts

• Limited investment options

• Early withdrawal penalties

• Limited, to no loan options

• Forced distributions

When you choose to put your funds into the Barefoot Retirement Plan, you are basically giving your money, and your access to it, FREEDOM. As you will discover shortly, our plan offers:

• Unlimited contribution amounts

• Unlimited investment options

• No early withdrawal penalties

• Unlimited loan options

• No forced distributions

We will show you how to “legally” break your money out of money jail, and give your money, and yourself, the freedom you deserve! Our program, gives the control to YOU.

The average life expectancy for someone entering retirement today is currently 84 years of age. This age is just an average. Over half will live beyond that — some will live into their 90s and even into their 100s. In fact, the Social Security Administration states that 25% of people turning 65 today will live past 90 years old and one out of 10 will live past 95.

While living longer is a wonderful thing and much better than the alternative, it’s also causing retirees to try to figure out creative ways to make their retirement savings last an extra 10, 15, and 20 years. That’s a tall order, especially at a time when health care costs are rising so rapidly. Even if you have the health and desire to work, jobs for the elderly are very scarce indeed.

A few years ago, I was in Sarasota, Florida having lunch with clients. Sarasota is a big retirement area, and it’s packed with retirees. It’s a beautiful area. Lots of sun, gorgeous beaches, great restaurants, and a slower pace of life.

During lunch, we were talking about life in Sarasota, and one of my clients said, “Yep, many of them retire at 65, and go back to work at 80.” It was one of those phrases that didn’t register in my mind when I heard it, until a few moments later, so I said, “Wait, hang on a moment… and say that again please.”

They said it was a pretty big thing there. Many people retire at 60 to 65 and move to Sarasota to soak up the sun and enjoy retired life. However, when some of them get around 80 years old, they find themselves running out of money. Sadly, many of them have no other options, so they have to try to find a job just to survive. Yikes! I had just never thought about that before, but it really weighed heavily on my mind. It used to be that when you retired, you stayed retired. Now, it’s not necessarily the case.

Let me just say I totally understand the people who “want” to continue working as they get up in age because they love it. It keeps them sharp and gives them purpose. I get that. However, I can’t imagine that represents a large percentage of retirees. I bet most of them have worked their guts out their entire life, and cherish the time to finally stop working, slow down, and enjoy doing the things “they” want to do.

Can you imagine how sobering it would feel to be 80 years old and wake up one morning and discover you have to go back to work? Heck, they probably haven’t worked a job in 15 years. Their work skills are probably not exactly up to par, so it can’t be easy to even find a job that anyone would want to do at that age.

I’m a ways from retirement myself, but I know how I feel some mornings waking up and having to get my body moving. I simply can’t imagine how it must feel to be 80+ years old and have to wake up early every day, to go to a job that you don’t want to do, but have to do, just to survive every day. Plus you’ll likely be bossed around by a boss, who’s a fraction of your age.

17% of retirees believe they retired too early, and should have kept working longer. I can’t imagine this scenario is the vision that very many people have for retirement. But what are you going to do? If you run out of money, you’ve got to do something. That’s why we’re on a mission to help as many people as we can, properly set up a Barefoot Retirement Plan, so they will be able to make choices during their retirement and won’t be forced to go back to work if they don’t want to.

When making your retirement plans it’s critical to factor in what your taxes will be, as well as cost of living increases. Some advisors will tell you that your taxes will go down in retirement because you’ll be earning less money. This is not necessarily true and the time to figure this out is when there’s still time to do something about it.

If your home is paid off you’ll lose your mortgage interest deduction. If your kids have finally moved out on their own or aged out, you can no longer claim them as dependents, so you’ll lose that deduction. There are a host of similar factors to consider but by far the biggest one, that’s staring all of us square in the face, that most people don’t what to talk about, is the overwhelming indebtedness of America. Let’s see…

Our national debt is over 17 Trillion Dollars and rising fast

47 million Americans are on food stamps and climbing

Obama Care costs likely to skyrocket out of control

Entitlement programs soaring like never before

49% of Americans (voters) currently receive Government benefits

Fed is producing 85 billion of new money every month

Social Security, Medicare & Medicaid going broke

Plus, as many as 1/3 of the largest cities in American are facing possible bankruptcy.

I hate to be Mr. Gloom & Doom here, but this stuff is a really big deal! Someone has got to pay for all of this. Even if the Government were to tax all the super-rich fat cats at a 100% tax-rate, that won’t even put a dent in it. The only way they’re going to be able to pay for all of this is to raise our taxes. Desperate times call for desperate actions, and you can’t ignore the transformation that’s happening right in front of us.

We’re in uncharted waters. No country in the world has experienced debt of this magnitude before. We have the largest government in the history of the world, and they are manipulating the largest economy in the world, and twisting the global market in ways that have never been done before. At some point, something has got to give, and when it does, watch out. Uncle Sam will be forced to raise taxes just to keep the Government Ponzi scheme going.

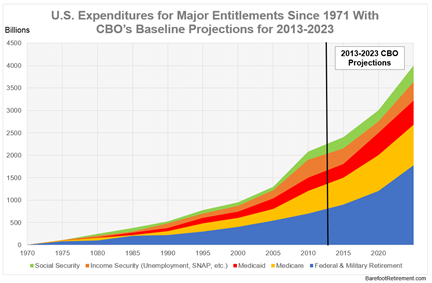

Take a look at the chart below. It was created by using the CBO (Congressional Budget Office) expenditure estimates. Looking at this chart, do you really see any way that taxes will EVER be able to go down in our lifetime? Hardly!

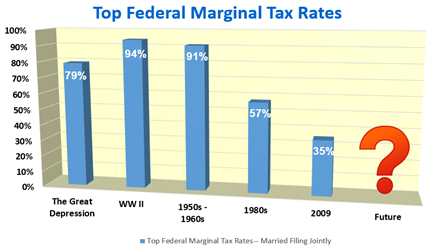

Obviously, no one knows just how high tax rates will go in the future, but we do know a few things. We know that history usually repeats itself. We also know that most people have very short memories.

Can you believe that the top Federal Marginal Tax Rates in the 1950s and part of the 1060s was 91%? Could rates ever get that high again? That’s up to you to answer for yourself.

It seems pretty obvious to me that if our Federal debt is at an all-time high and considering all the other economic challenges we are burdened with, at some point the Government will be forced to consider ALL options. If/when they can look back and say, “We’ve done it before….” Do you really think they won’t think of this? The past history of rates being that high could give them precedence they need to do it again.