Some people think that credit cards are evil and that keeping kids on the other side of the moat is the only way to keep them safe. But that assumes that credit card companies will never breach the castle. Hey, it’s only a matter of time. Far better that kids know what to do with plastic when they finally have some in their hot little hands. And who better to teach them than you?

The first time most kids learn about credit is when they go off to university and the credit card companies start throwing cards at them. With no experience and very little understanding of the long-term negative ramifications, kids start to charge. And they charge, charge, charge until they’re in a hole. That’s because they’ve had no prior experience with how a credit card works, or how to use one so that it’s a tool and not a Debt Pit.

All it takes is a little time and a thoughtful approach to help your children see credit for what it is: useful when used correctly, deadly when it isn’t. When you use your credit card to purchase gas or pay for a new bathing suit, take the time to explain how credit cards work. Show your children that you’re only putting on the card what you can afford to pay off when the bill arrives. Explain that you use your card for good reasons, not just to scratch your consumer itch, because this debt has to be repaid.

Even relatively young kids can get in on this lesson. Issue your 10-year-old a credit card on the Bank of Mom & Dad. (Have her design it herself, if you like.) Draw up a cardholder’s agreement that both of you sign. It should clearly state:

It’s important that you use a fairly high interest rate in your agreement. If you wuss out and charge just 5% a year, the lesson that using someone else’s money can be expensive is likely to get lost. Charge a whopping amount of interest (hey, department stores charge more than 24%), and the lesson will be made more real for your kids.

Your child can now use her credit card when she goes shopping with you. If she sees something she wants to buy, she gives you her card and you make the purchase on her behalf using your money. You give her a charge receipt.

Remind her that if she doesn’t have the money at home ready to pay the card off in full when the bill comes in, she’ll have to allocate her future allowance (or babysitting money) to pay the bill when it arrives. Make the point clear: she is spending money she hasn’t yet earned, and she’ll pay interest to do so if she can’t come up with the money in time.

If she spends more than she can afford, or makes her payments late, you’ll have to charge her interest on the balance. Use 24% as your interest rate for this exercise, and don’t give in. To calculate the interest, multiply her monthly balance by 2% (which is the equivalent of 24% a year). So if she owes $16.50, the calculation would look like this: $16.50 x 2 ÷ 100 = $0.33.

Point out that she is paying that 33¢ for having used your money for a month. It is like she “rented” the $16.50 for a month, and the cost was 33¢. And if she doesn’t pay it off soon, it will continue to cost her money every month to keep “renting” the money she’s charged on her credit card.

Once your child is 16 or so (you’ll have to gauge his maturity), you may wish to get him an actual credit card (it will have to be in your name since only those 18 and older can have a credit card of their own) and start him using it and repaying it regularly. This is a habit, and one well worth the effort to form. By the time your child is 18, he should have a card in his own name so he can start building a credit history.

As you teach your credit lessons, don’t skip steps because you think they should be obvious to your teenager. Start by explaining how credit cards work.

Not all kids will be suited to using plastic. Not all adults should be using plastic. Be honest about your kids’ organization and sense of discipline. If Molly just doesn’t have the wherewithal to manage credit smartly, tell her that she isn’t well suited to using credit cards and that, until she develops some discipline, she should avoid them like the plague.

Your own values will also come into play when it comes to teaching kids about how to spend money. Whether your family lives on cash or uses plastic, talk with your children about the choices you’ve made and why. And remember that they’re always watching, so be mindful of how your use of plastic influences your children.

Advances and Loans

Whenever I talk about allowances, inevitably questions come up about whether or not I think giving kids loans or advances on their allowances is a good idea. In this case, we’re not talking about a lesson in credit so much as a way of managing kids’ expectations and behaviours. My take on it is that it’s really a matter of personal choice. However, there are some things you should think about when making the decision. Each occasion will warrant consideration on its own merit—there are no hard-and-fast rules—and every experience has the potential to teach a lesson, good or bad.

How often does your kid hit you up for money?

If Boyo is always asking for an advance or loan, he may be having trouble learning how to budget and how to plan for the future. Adults manifest the same lack of skill when, rather than saving for an item, they apply for a loan or use their credit card and carry a balance. The desire for immediate gratification outweighs their patience in implementing a planned spending approach.

However, the cost of this borrow-spend-repay strategy is very high. Every cent in interest paid on a loan (including on a credit card balance) is money wasted. So, do you want your child to become a borrower or to be skilled at planned spending? If Boyo doesn’t ask for a loan or advance with any regularity—if it really is a case of an emergency or a special occasion—then using it as a lesson on how to borrow, and the costs associated, can be worthwhile.

What are your expectations in giving the loan?

If you go to a bank to borrow money, you’re expected to pay the money back. All of it. Not only will the lenders expect you to repay the principal, they’ll also expect you to ante up some interest. And you have to make your payments on time. If you want your child to learn about borrowing, you need to set some expectations.

Are you going to charge interest?

Now don’t come hissing and clawing at me with terms like “usury” and “profit.” I’m not suggesting you build your retirement plan on the back of your child’s borrowing. I am suggesting that if you want children to experience the true impact of using someone else’s money to meet their spending desires, then interest must be a part of the equation. With the lack of cost would go the deterrent to borrow (as small a deterrent as it sometimes appears to be). If you teach them it costs nothing more to acquire that scooter than the ticket price, even when they’re tying up your hard-earned money, are you really preparing them for the credit cards and personal lines of credit that are in their futures? If this is to be a real money lesson, charge them 24%, which translates easily into 2% a month.

What if Sweet Pea won’t repay the loan or allowance advance?

Make the point that inconsistent repayment affects a person’s ability to borrow in the future. If she doesn’t repay the loan, there will be no future borrowing.

You may decide to withhold a part of her allowance and apply that to the repayment of the loan. (In the real world, this is referred to as having your wages “garnished.”) But before you take this step, think of the message you are sending by removing the responsibility for making the repayment from your child. A better lesson would be to insist upon repayment as soon as you have given your child her allowance. Create a chart showing how much she owes. Then each week reduce the amount owed so she can see her progress in repaying the loan.

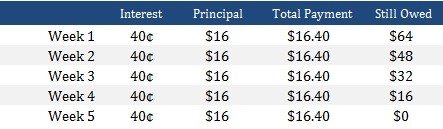

Let’s say your daughter wanted to buy a new gaming system. She had saved $65 of the $185 she needed. There was a great sale on and she got the item for $145, with a loan of $80 from you. Now that she has the game, you’re having trouble getting her to pay you back. Time to make the chart.

At 24% a year in interest (which works out to 2% a month), your kid’s $80 loan will cost ($80 x 2 ÷ 100) $1.60 a month or 40¢ a week in interest. If you expect that loan to be paid off in five weeks, then she’d also have to give you back ($80 ÷ 5) $16 a week towards the principal (the amount you lent her). So you would draw up a chart that looks like this:

If your child is wishy-washy in keeping her commitments—she repays the loan eventually, but at her own pace and with a fair amount of grumbling—there’s fallout: before you will give her another loan, she must offer you some form of collateral. It may be her bike, her telephone, or her laptop. Make up a loan agreement and include a paragraph that clearly spells out that if the loan is not repaid on time, you have the right to take whatever collateral she has given you until the loan is repaid.

A child who does not repay a loan on time needs to see the consequence of developing a bad credit history: no more loans. And the child who is constantly borrowing may benefit from having a loan request declined, to teach how constant borrowing reduces her ability to repay (and therefore qualify for) yet another loan.

Borrowing itself isn’t a bad thing, provided that we’re borrowing for the right reasons. Knowing when to borrow and how to manage credit are important lessons well worth a few discussions at home where they can be learned in safety.