Here the relationships between the various elements of an economy are developed in order to reach a clearer understanding of the things we are particularly interested in like material wellbeing and growth or decline, and the things that influence them. However the analysis is only relevant for the economy as a whole, it gives no indication of the distribution of wealth and wealth entitlement.

The chapter includes a lot of maths, which is necessary to illustrate the derivation of standard economic equations. These equations are used to provide a very simplified way of picturing what in reality is an immensely complex web of interactions. Understanding it is not necessary for subsequent discussion so if maths isn't for you then just skip it.

Economic growth and material wellbeing are discussed in terms of what it is that delivers them. It is not intended to imply that they are desirable ends in themselves unless they are delivered sustainably - i.e. with insignificant impact on natural resources and the environment - see chapter 7.

Each country prepares National Income Accounts, which set out its economic activity within a certain timeframe. It lists all sources of domestic income and records how that income is allocated. It allows the country's gross domestic product (GDP) to be determined. The UK's accounts are recorded by the Office for National Statistics (ONS).[100]

First it is necessary to define the terms used and to be consistent and as precise as possible whilst recognising that complete precision is not possible. Fioramonti discusses the problem in his book (Fioramonti 2013 Chapter 2). Definitions in economic texts tend to differ and are often not set out explicitly, so they are often difficult to understand and it's hard to gauge their impact on overall growth and material wellbeing. It is hoped that the definitions used here allow growth and material wellbeing to be understood in terms of their component parts. Some of the terms have been mentioned before. I have used the general term 'wealth' where products may be goods or services:

Capital wealth is that which facilitates the production of finished wealth (see below) without becoming part of that wealth. Examples include tools and machines, skills, techniques, organisation, research and development, education and training. It encompasses the knives and wheelbarrows used in the simple economy - see chapter 4. It also includes new capital wealth used to replace that which is no longer working. New replacement wealth is needed to compensate for depreciation, but depreciation is excluded from GDP, in fact that's what 'gross' means. If depreciation is subtracted from Gross Domestic Product then we have Net Domestic Product.

Consumer wealth is that which directly sustains or improves people's lives.

Finished wealth consists of things that are directly usable and ready for sale as opposed to things that are still in the process of being made or things that have been sold. It encompasses unsold capital and consumer wealth and also unsold outputs, including raw materials used as inputs in other manufacturing processes.

Intermediate wealth includes everything that is awaiting assembly or in course of being assembled into finished wealth, and administrative services necessary to produce finished wealth such as production management and stock control. Intermediate wealth eventually becomes finished wealth. Examples include raw materials bought from suppliers, unassembled or partly assembled components, and associated administrative services. It excludes things that are needed for production but have not yet been obtained by the producer. For example boxes of screws awaiting sale from a screw manufacturer represent finished goods, but when bought by a furniture manufacturer they become intermediate goods. It also excludes things needed to maintain wealth-creating capacity - these are overheads.

Overheads consist of everything needed to maintain the wealth-creating capacity (as opposed to production itself) of an economy. Overheads represent a type of investment wealth, but a type that maintains wealth-creating capacity as it is rather than increasing it. This is a term seldom used in analyses of economic growth and GDP but Fioramonti draws attention to its importance in his book (Fioramonti 2013 p60). It includes all consumables required for operating capital equipment and administrative services directed at maintaining wealth-creating capacity such as maintenance scheduling. It also includes government expenditures such as national infrastructure repair works, policing, security services, environmental protection, healthcare and many more, since all these things maintain the wealth-creating capacity of the economy in terms of healthy people and well-functioning infrastructure. Just as human beings and all living things need to consume wealth in order to stay alive and functioning, capital wealth also needs to consume wealth in order to remain functioning. This type of consumption has a different nature to human consumption because in itself it doesn't sustain or improve lives, so we give it a different name to avoid any confusion. In the simple economy in chapter 4 wheelbarrow maintenance and knife sharpening are overheads, though the term wasn't used during that discussion to avoid unnecessary complication.

Investment wealth consists of capital, intermediate and finished wealth, and overheads.

Inventories consist of intermediate goods and stocks of finished goods (services can't be stockpiled so inventories just consist of goods).

Of particular concern are changes from one accounting period to the next, so time is taken into account in terms of production, consumption and so on within a particular accounting period, normally a quarter or a year. The basic economic elements are consumption, investment, saving, government spending, taxation, exports and imports, all within the period of interest. GDP represents overall (economists prefer 'aggregate' when referring to the whole economy) economic output in the period, which is the production of all new wealth, so it includes the value of all consumer and capital wealth that is sold in the period and also changes in inventories from the beginning to the end of the period. We are only interested in changes in this wealth because the period starts with a substantial amount already in place, so that must be subtracted from the amount that is in place at the end of the period, giving the change which can be positive or negative. Transfers of existing wealth and transfers of money other than for new wealth are ignored because in themselves they don't affect aggregate economic output. In fact transfers for any purpose other than for the sale of new wealth are ignored, because our only interest is in aggregate economic output - i.e. new wealth. This can be confusing. Borrowing is a money transfer, but what about interest? That might be considered payment for the service of making money available[101]. In the case of business borrowing it is assumed to be for investment purposes so it is counted and lumped in with private investment. In the case of consumer borrowing it is counted and lumped in with private consumption. In the case of government borrowing however interest is regarded as a money transfer, being a transfer from society as borrower back to society as lender - aggregate output not being affected. The essential point is to ensure that all new wealth creation and consumption is counted somewhere, but only counted once.

Transfers of money without anything in return are known as transfer payments, examples being benefits, pensions and subsidies, but I think it is clearer if we extend the definition of this term to include all money transfers for other than the sale of new wealth, and that is the sense in which it will be used in this analysis.

First we derive the equation for GDP in terms of spending on new wealth - this is known as the expenditure equation, also known as the output equation and as the national income identity. We need only consider consumer and investment wealth, because together they account for all wealth changes over the period. Note that a change in intermediate wealth over a period will be reflected as a corresponding change in investment wealth.

Consumer wealth - (here denoted by 'C') can either be consumed domestically or consumed abroad, and can either be produced domestically or produced abroad. The same applies for investments (here denoted by 'I'). We are only interested in domestic aspects for our own economy, so things that are both produced abroad and consumed or invested abroad don't concern us.

Wealth (for consumption or investment) produced domestically will be denoted by 'pd', and produced abroad by 'pa'.

Wealth consumed domestically will be denoted by 'cd' and consumed abroad by 'ca', and wealth invested domestically will be denoted by 'id' and invested abroad by 'ia'.

Gross domestic product (wealth expressed in money terms - also known as gross domestic output) consists of all wealth produced domestically, and is denoted by 'Y'.

Therefore:

Y = Cpd + Ipd = Cpdcd + Cpdca + Ipdid + Ipdia

This says that GDP consists of all wealth produced domestically wherever it is consumed or invested.

But Cpdca + Ipdia is the totality of exported wealth, so we can denote this by 'X'.

Therefore:

Y = Cpdcd + Ipdid + X

We can further develop this in terms of total domestic consumption and investment (Ccd and Iid) by noting that:

Ccd = Cpdcd + Cpacd and Iid = Ipdid + Ipaid

Therefore:

Cpdcd = Ccd - Cpacd and Ipdid = Iid - Ipaid

Rearranging the above equation we have:

Y = Ccd + Iid - (Cpacd + Ipaid) + X

But Cpacd + Ipaid is the totality of imports, denoted by 'M', so:

Y = Ccd + Iid + X - M

This tells us that GDP consists of domestic consumption (wherever produced), domestic investment (wherever produced), together with exports less imports.

This is the expenditure (output) equation. Here Ccd + Iid include all domestic consumption and investment, but textbooks normally include a separate entry for government expenditure, so we can split Ccd into two components where Ccd = Ccd(gov) + Ccd(non-gov), and similarly Iid = Iid(gov) + Iid(non-gov).

Note that government expenditure excludes pensions, benefits, subsidies and so on[102], because these are transfer payments whose effect on consumption and so on are included in the other components; failing to exclude them leads to double counting. Borrowing also represents a transfer payment from lender to borrower, so government borrowing is also ignored. If we now let:

G = Ccd(gov) + Iid(gov)

we have

Y = Ccd(non-gov) + Iid(non-gov) + G + (X-M)

which is the output equation, normally expressed as:

Y = C + I + G + (X - M)

where 'C' denotes Ccd(non-gov), i.e. private consumption, and 'I' denotes Iid(non-gov), i.e. private investment.

Expenditure (output) equation: Y = C + I + G + (X-M).[103] This means: GDP = private consumption (wherever produced) + private investment (wherever produced) + government expenditure excluding transfer payments + the excess of exports over imports.

Next we derive the income equation.

Gross domestic income (or national income) - GDI - is the same as gross domestic product (or output) - GDP, because the money used to buy wealth is the same as the money value of that wealth, so it is also denoted by 'Y'. As discussed above all private income is allocated to individuals, so company incomes aren't included in the income equation because all such income is allocated to individuals in the form of wages, purchases, dividends, interest, shareholder equity and so on as mentioned earlier.

Recall the private saving definition from the last chapter: private saving = after-tax income not spent on consumption. Here after-tax income is gross domestic income less tax, where gross domestic income is denoted by 'Y' as discussed above, taxation is denoted by 'T', private saving by 'S' and private consumption by 'C'.

Therefore:

S = Y - T - C

or, rearranging:

Y = C + S + T

This is the income equation.

Note that tax in this context excludes that which funds transfer payments, as government expenditure excluded transfer payments earlier. Although in reality much of taxation goes on pensions, benefits and subsidies etc., those elements are already accounted for in this equation when they are either spent on consumption or saved by individuals, i.e. in the C + S elements.

Tax is also paid by companies from profits, but since all income is allocated to individuals companies' gross profits are regarded as allocated to individuals, with individuals paying all tax, whether levied on individuals or on companies.

Income equation: Y = C + S + T.[104] This means: GDI = private consumption (wherever produced) + private saving + tax (excluding transfer payments).

Now since both equations represent gross domestic product we can combine the two so as to express investment in terms of savings:

C + I + G + (X - M) = C + S + T

Subtracting C from both sides gives

I + G + (X - M) = S + T

So overall we have:

I = S + (T - G) + (M - X)

This is the savings identity.

The savings identity: I = S + (T - G) + (M - X).[105] This means that private investment (wherever produced) = private saving + public saving (tax less government expenditure) + excess of imports over exports.

This says that domestic investment is bought by the money that is saved privately and by government out of national income, plus the money from national income that is spent abroad. Note again that saving can be by direct purchase of investments (good investment), or by failing to buy goods and services that are offered for sale - thereby causing unsold stock, unbought services and increased inventories (bad investment). If imports exceed exports then there is a net outflow of spending abroad[106], which would otherwise buy domestically produced goods and services, so this money contributes to bad investment. Also if taxation exceeds government expenditure then money is lost from circulation, and again this contributes to bad investment. Note that to prevent unnecessary complication all bad investment is allocated to private investment since most unbought stock and services are produced by the private sector.

The savings identity is normally expressed as above, but this hides the good and bad investment aspects, so we can go further and split S into saving that takes money out of circulation 'Soc' (equivalent to bad investment) and saving to buy new investments 'Sni' (good investment for future production), giving:

I = Sni + Soc + (T - G) + (M - X)

Note that Soc includes imported investments, since although these will be utilised to increase production in the future the immediate effect is to take money out of circulation.

Of these terms [Soc + (T - G) + (M - X)] represents transient saving in that if overall it is positive then it corresponds to bad investment and shrinkage of the economy as firms cut back on production and hence on the workforce. As the economy shrinks (less national income) people become fearful for the future so there is less aggregate spending. Less spending means more paying down of debts, less tax revenue, less good investment, and also less bad investment - people have less money so can't keep as much in cash or in banks and can't import as much. Overall in these circumstances the transient element diminishes until it is zero and a steady state is reached when I = Sni, but I and Sni after the transient has gone will be considerably less than they were before because good investment has diminished along with all other spending.

This is the mathematical version of the paradox of thrift insight that was recognised in chapters 13 and 15 for the simple economy and the real economy:

When people cut back on spending and take money out of circulation the only way to avoid economic contraction is for the government to spend in order to compensate. Government must put as much new money into circulation as private individuals have taken out. If the government instead imposes austerity then it does the opposite and the economy shrinks even faster.[107]

If however the transient saving element [Soc + (T - G) + (M - X)] is negative overall, then the economy expands until all spare capacity is used up, and then if it remains negative there is inflation - see chapter 18.

We can now return to a point that was made earlier in chapter 4 that change in GDP is taken to imply change in material wellbeing. A problem is that changes in investment wealth are counted as changes in GDP, but this wealth in itself does nothing for immediate material wellbeing, though capital wealth should enable it to grow as it delivers additional wealth in the future.

So how can we measure material wellbeing? At first sight and using the designations given above this would seem to be the same as Ccd for a given accounting period. This is the quantity of consumer wealth consumed domestically in the period. However it is deficient as a measure to the extent that some of it is imported, which will only make us poorer in the future unless it is offset by sufficient exports to pay for it (if not then the country is living beyond its means which leads to grief eventually as Mr Micawber pointed out[108]). Therefore a better measure is one that takes account of exports and imports and is Ccd + X - M. This measures Ccd together with national income coming from or going abroad, which is the degree to which the country is well off in terms of both consumed wealth and entitlement to foreign wealth - which might be negative. We might of course choose to spend some of the current entitlement on foreign capital wealth rather than on consumer wealth, but that would affect a future accounting period. So far as this period is concerned we are well off to the extent of how well we have lived plus the extent to which we have accumulated in the present entitlement to live in the future.

Let's call the measurement we are after AMW for Aggregate Material Wellbeing, noting especially that this is a measurement for the country as a whole - as indeed are all the other measurements, it tells us nothing about how wellbeing is distributed between individuals within the country.

From the above discussion:

AMW = Ccd + X - M

Aggregate material wellbeing is domestic consumption plus exports minus imports. A more significant measure is AMW per capita, which gives the wellbeing per person rather than for the population as a whole. It is easily derived by dividing AMW by the population.

Now from the expenditure equation (before we brought in government taxation and spending)

Y = Ccd + Iid + X - M

so

Y = AMW + Iid

and

AMW = Y - Iid

This makes sense because it strips out all investment wealth from GDP, because investment wealth has no immediate effect on aggregate material wellbeing, though capital wealth should allow it to grow in the future.

Bringing back government aspects for completeness we have:

AMW = Ccd(gov) + Ccd(non-gov) + X - M

Aggregate material wellbeing is private and government domestic consumption plus exports minus imports, or, in terms of GDP:

AMW = Y - Iid(gov) - Iid(non-gov)

Aggregate material wellbeing is GDP minus private and government domestic investment.

Aggregate material wellbeing for a given time period can be expressed as private and government domestic consumption together with exports less imports, or, in terms of GDP, aggregate material wellbeing is GDP less private and government domestic investment.

Growth or decline in aggregate material wellbeing can easily be determined by changes from one period to the next.

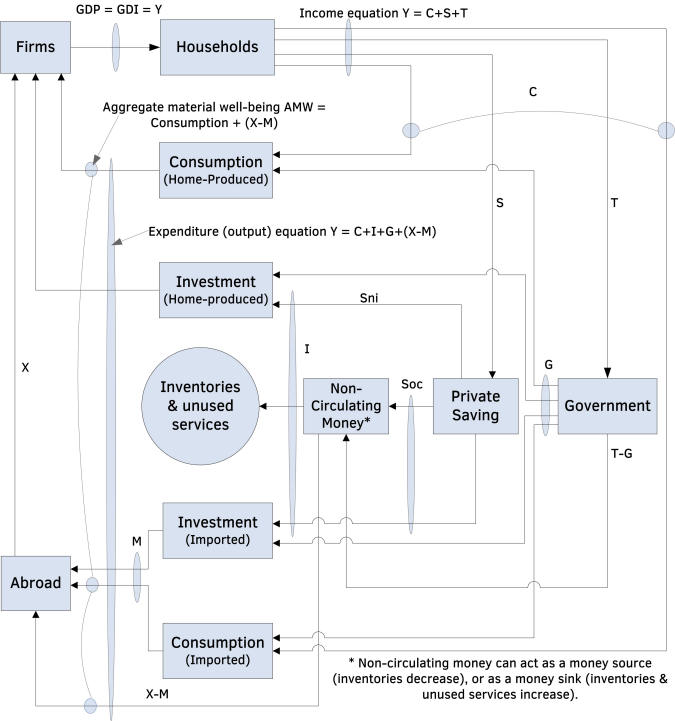

All the foregoing can be shown on a money flow diagram - see figure 26.1.

This shows the flow of money in relation to new wealth production in the national economy. By any standards it is complex! To make sense of it all elements must be strictly defined. I haven't been able to find any textbook or other source that defines all the terms fully or presents the relationships in a fully developed diagram so I have worked this up to show the validity of the equations and identity. I present it here in case it's of any interest to others.

Figure 26.1: The circulation of money used for new wealth production in a national economy

Note that services that aren't used are wasted, they can't be stored for later sale as can inventories, so they can't act as a money source.