A moral hazard is an incentive to do something that is beneficial to the person or company that does it but is harmful to others, and the unfettered market economy is full of them - see chapter 29. For example when a salesperson is paid a bonus for every customer they sign up for a particular product (as most are) they have every incentive to emphasise the benefits and hide the disbenefits, even when the product is likely to be detrimental to the customer. What's more the most successful of such salespeople are often those least hindered by conscience.

Moral hazard is a prominent feature of the banking system as it is currently set up, and it became very much worse as banking regulations were progressively weakened and removed from the 1980s onwards.

To illustrate the fertile ground for moral hazard that the banking sector presents I ask three simple questions that were first asked (along with many others) by James Robertson (Robertson 2012 Chapter 3).

i. Who should create money?

ii. How much money should be created?

iii. Who should decide where to allocate newly created money?

In a truly democratic society the answers should surely be:

i. A public body, acting in the public interest, independent of both government and private interests, operating transparently to criteria set by government.

ii. As much or as little as is judged by experts, who are fully accountable for their judgements, to be in the best interests of the public.

iii. The government of the day.

In stark contrast, the answers currently in place are:

i. Banks, acting purely in their own interests (banks have created 97% of the money in circulation - bank money - whereas the BoE has created just the remaining 3%, as notes and coins).

ii. As much or as little as best serves the interests of the banks.

iii. The banks themselves, with the object of maximising their profits.

In light of these answers how can anyone can believe that the system serves the public interest? Yet there are such people, and they aren't just those who profit by it. Neoliberals believe that banks operate in a free market and anything that the free market does is bound to be in the public interest. They are wrong on both counts.

Ultimately it is the government that is responsible for the economy, so the government always provides the backstop for any mismanagement by the banking system. In this respect banks enjoy a very privileged position relative to any other private business. The government permits banks to operate in this way and to create the country's money supply with very little restraint, yet the value of that money and the validity of the corresponding debts (no matter how toxic) are guaranteed by the taxpayer, as the 2008 bailout clearly demonstrated. This creates a very severe moral hazard. Sir Mervyn King recognised this when he said: "Of all the many ways of organising banking, the worst is the one we have today."[176]

We entrust private banks with the responsibility of creating the national money supply, and permit them to do so in the manner that best suits themselves, but the value of the money they create is guaranteed by the taxpayer. When operating successfully the banks enjoy huge profits, but when reckless lending leads to widespread defaults it is the taxpayer that suffers the losses.

Heads the banks win; tails the taxpayer loses.

This effect is a severe negative externality. The banking service benefits the banks, its managers and shareholders, but when things go wrong it severely harms everyone. It is in effect a polluter, and although the pollution isn't visible until crises erupt, at those times the pollution unleashes its toxic effects on everyone.[177]

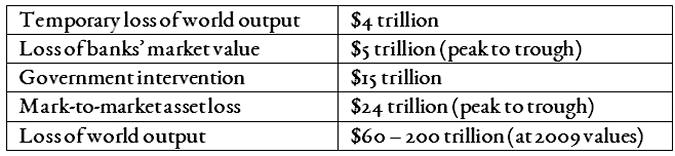

Andrew Haldane - Chief Economist and Executive Director, Monetary Analysis and Statistics, BoE - in a speech to the Institute of International and European Affairs in 2011, estimated the cost to the world of the banking failures in 2008.[178]

He presented the following estimates (US dollars):

Table 50.1: World cost of 2008 banking failures

Let's just take a moment to digest that last figure. Between $60 and $200 trillion in wealth value lost to the world. That represents the wealth that would have been created if the crisis hadn't happened, and is now irrevocably lost. To put it into context world output in 2011 according to the World Bank was $71 trillion[179], so if Haldane's estimate is right then between one and three years' worth of world wealth creation was lost. That's a staggering loss.

With that wealth we could have stabilised carbon emissions at sustainable levels,[180] guaranteed clean water for everyone,[181] ended world poverty,[182] and stopped the destruction of the biosphere.[183] That's the level of catastrophe that the banking system unleashed.

In fact the real damage of the 2008 crash may well be environmental. Because of it we have devoted precious efforts and resources just to keep economies afloat and environmental concerns have gone on the back burner, making eventual catastrophe all the more likely.

Haldane in the same speech also estimated the total implicit subsidy to UK banks as £10 billion in 2007, £55 billion in 2008 and £100 billion in 2009. The subsidy is implicit because it manifests as much lower costs to banks than would be the case if banks rather than taxpayers bore the risks involved. For example when depositors (including you and me) know that banks will be rescued if they fail then we don't worry about what the banks do with their money and we are satisfied with a low rate of interest on our deposits. If on the other hand we knew that no rescue would occur, and that in the event of bankruptcy we would lose our money, then we would take great interest in what banks did and would want a much better rate of interest before taking the risk of trusting banks with our money. Note that the above subsidies don't include the subsidy from society to banks for lending real wealth whereas banks take all the profit (see chapter 48), and they don't include the interest payments from taxpayers to banks for the government bonds that they own when there is no need for any such payments - see chapter 44. Also, and more importantly, these subsidies represent a completely separate cost to the cost of the damage to world output that the banking failures caused. The subsidies are what society pays to banks so that they can continue to provide services at great profit to themselves, whereas the lost output is what it cost society when banks over-reached themselves. For comparison purposes the cost to the UK taxpayer of the NHS is about £120 billion per year (2016/17).

Banks have every incentive to grow as big as possible, because the bigger they are the more likely they are to be bailed out when they fail. They try their hardest and largely succeed in becoming 'Too Big To Fail' because doing so represents for them a major safeguard. In fact it isn't just size that makes them more likely to be bailed on failure, at least as important is interconnectedness. The more likely it is that one bank failure will lead to other bank failures again the more secure is the entire sector and the more insecure is the taxpayer.

Sir Mervyn King put the point very succinctly on page 15 of his talk referenced above:

It is hard to see why institutions whose failure cannot be contemplated should be in the private sector in the first place.

Other helpful references on bank subsidies include the Positive Money website[184], and a BoE paper in May 2012 that addresses the different ways of estimating the subsidies.[185]

What was it that changed banks from the old regime when they took great pride in integrity and probity? A regime that prevailed until the 1980s and was characterised by the phrase 'my word is my bond'; when reputation was everything both for individual bank managers and for the banking system as a whole. Banking was always profitable, and the profits represented easy and unjustified money, but the profits were nothing compared to those in more recent times, and bank managers and directors were paid no more than people with similar qualifications, experience and responsibilities in other professions. As globalisation gathered pace with the removal of restrictions on global capital flows it became easier and more profitable for banks to set up businesses in other countries both to compete with existing banks in those countries and to get round their own country's restrictions. Countries with lower regulatory and taxation burdens were very attractive to foreign banks, and this put pressure on home governments to reduce their own regulations and taxes to avoid losing business to foreign countries. This began the 'race to the bottom' in terms of regulation and taxation (Kay 2015 p20 and Rodrik 2012 pp263-264).

One of the major relaxations was in the rules relating to securitisation - the packaging up of banks' long-term loan contracts and selling derivatives based on them in the market to investors. Until that time banks had to take great care with regard to whose debts they were willing to finance because they retained those debts until they were paid off, so they were on the hook for the duration of the loan in the event of the borrower defaulting. This caution provided a natural brake on banks' enthusiasm to take on more and more debt - the more debts they took on the more profit they made, but the more likely a significant default would break the bank. After securitisation banks could be a lot less cautious about borrower creditworthiness because the buyers of the securitised loans were at risk of default, not the banks themselves. There was then almost no restriction on the amount of debt they could finance without risking their own security, though they were risking the security of the whole financial system - see chapter 54.

As profits grew, so did bank management and director salaries and bonuses - to almost unimaginable levels - as there was little to stop them. Indeed so much was taken from banking profits in management payouts that the initial bailout of £50 billion for UK banks following the 2008 crash was equal to just 10% of those payouts between 2000 and 2007 (Brown 2011 p106). At this time greed took over from probity as the defining feature of the banking sector. So deep was the culture of greed that bankers were quite willing to break the law in the interests of even more profit - mis-selling of payment protection insurance (PPI), money laundering, LIBOR fixing, predatory lending, forgery, fraud, foreign exchange manipulation and much more.[186]

And who was and still is it that pays for all those profits, salaries and bonuses? It is ordinary people, those who take on debts, either by choice or necessity. To pay the banks people have to work longer hours, have two or more jobs, have both partners in a relationship working, and even then still have to rely on credit cards (yet more profit for banks) to make ends meet. An increasing number of people have become slaves to stress and misery as a result.

It is a sobering thought that if all associated costs of the banking sector were to be paid by the sector itself banking would very likely not be profitable at all. This is what John Kay said:

If banks had to pay for the insurance provided by the doctrine of 'too big to fail', the trading activities in which they privately engage simply would not take place, or at least would not take place on the current scale. Much, perhaps all, of the profitability of these institutions comes from the willingness of lenders (including other financial institutions) to make finance available on terms that would, in the absence of such public support, be regarded as too risky. (Kay 2015 p140)

It is worth pointing out that Kay doesn't include the interest charges in excess of default risk that society pays as argued in chapter 48, so if we were to deduct these from bank profits then I think we can be quite confident that the banking system as it is currently structured - with such a high degree of integration and therefore so high a risk premium - would not be profitable.

We can therefore regard ALL of the banking system's profits, together with the salaries and bonuses of everyone employed in other than the everyday banking services that society needs, together with all the crisis insurance paid by society, as a massive subsidy from society to banks. Subsidies are transfer payments - in this case by wealth extraction - and as such represent a massive and completely unjustified burden on society.

All this begs the very serious question put by Mervyn King above: Why is banking a private sector activity when it receives such massive support from society? No-one would dream of providing such support to any other private business. I suspect it is because the support is largely hidden, but no less real for that.

A very pertinent and telling quotation attributed to Mayer Amschel Rothschild sums up the situation well: "Give me control of a nation's money and I care not who makes its laws."[187]

If ever an event showed the economy's dependence on and vulnerability to the activities of the banking sector it was the 2008 crash. To avoid similar and potentially worse events in the future radical overhaul of the banking system is therefore urgently required. But such is its power and hold over world governments that all that has happened and is intended to happen is some minor tinkering around the edges.

The banking sector puts up massive resistance to any proposal to restrict its activities and it does itself no favours by doing so. Surely its leaders can see for themselves the damage that their activities have already caused both to society and themselves, and will cause again on an even bigger scale in the future if they are left to their own devices. Perhaps they believe that they have learned all necessary lessons from the last crash and can avoid a future one by self-restraint? If so they are deluding themselves by forgetting the main factor that promotes success during economic expansion, which is risk-taking. Those banks that take the biggest risks attract the most profits, and any bank that exercises restraint is left behind. In fact if a cautious bank is left too far behind then it becomes a target for a hostile takeover by a more profitable bank, which then continues its risky strategy but on a bigger scale. A strategy of exercising caution on the part of a single bank sets up what is in effect a positive externality - see chapter 29 - in that the whole sector becomes safer because the degree of interdependence is less fragile (the extent depending on the size of the single bank), but the single bank bears all the costs. Other banks can enjoy the safer climate without any cost to themselves. In effect they become free-riders on the cautious bank's back. It is the same as if a single household pays for street lighting on the road where they live. The lighting benefits everyone on the road but the costs are borne by the single household. I don't know of any single household that provides street lighting, and I don't believe that any single bank will exercise adequate caution when the others don't.

It is this feature of banking - the bigger the risks the bigger the profits - that drives all banks to take bigger and bigger risks, in the current climate banking competition enforces it. Managers that are inclined to caution either suppress it or suffer from competition with more profitable banks that don't exercise caution. If their banks suffer then they are sacked and replaced with someone less cautious. It's the effect of banking freedom allowing bad practices to drive out good practices that was discussed in the Introduction. A comment by Charles "Chuck" Prince (former chairman and chief executive of Citigroup) sums up the situation:

As long as the music is playing, you've got to get up and dance. We're still dancing.[188]

When restrictions are imposed from outside the sector all banks are subject to them so competition driven by risk disappears, and this benefits not only society but the entire banking sector by becoming safer. Other industries that impose risks on society are subject to restrictions, and everyone including the industries themselves recognises the need for them. Banking should be no different, indeed if anything the restrictions should be more severe for banking because the potential damage is so much greater.

Can it be that bankers don't care about safety, knowing that whatever damage their activities cause to society as a whole they themselves will likely keep their gains? I sincerely hope not. Selfishness on that scale is truly frightening. A very notable feature of the 2008 crash is that no bank directors or managers suffered any penalties other than disgrace after their reckless lending. I am convinced that sending the worst offenders to jail for their misdeeds would help to concentrate all similarly placed minds very forcefully. Benefits would be weighed much more carefully against costs if those costs included significant jail terms!

In any other walk of life if someone is asked to guarantee a debt that responsibility is taken very seriously. Yet governments guarantee bank debts (bank money), not only for existing debts but for any future debts, and banks are free to take on whatever debts they wish.

Banking is generally regarded as only one factor amongst many that contributed to the Wall Street Crash of 1929, but bank credit fuelled the excesses in production during the 'roaring twenties' and fuelled much of the investment in the stock market during its meteoric rise in that decade. Share prices were rising not because companies were worth more but because buyers were much more willing to buy than sellers to sell - and their willingness came from the fact that easy credit fuelled share price rises - a vicious circle that created a massive bubble. Banks created the money to buy them on the collateral of the shares themselves - a classic positive feedback mechanism - see chapter 52. The bust came as busts always do when new buyers were no longer available, at which point investors started selling shares to avoid losses and share prices started to drop. Banks then forced investors who had borrowed in order to buy shares to sell yet more shares to avoid them becoming overdrawn, and that accelerated the price drops in an ever steepening downward spiral. Hence without the activities of banks in fuelling the over-expansion of production and the stock market bubble the crash would either have been very much less severe or wouldn't have happened at all.

Following the 2008 crash there has been a strengthening of the Basel III accords (a global voluntary regulatory framework) consisting of three linked limits - minimum capital adequacy ratios, minimum leverage ratios, and minimum liquidity ratios. They are intended to allow banks to survive for longer during periods of stress such as that experienced during the 2008 crash. They may well succeed to some extent, but at best all they will achieve is to extend banks' survival time, they certainly won't fix the system (Ryan-Collins et al. 2012 Sections 5.1.1, 5.1.2 and 5.2 pp95-100). What they also don't take into account is banks' ability to find ways round regulatory limits. Banks have every incentive to circumvent limits because the result is increased profits (often massively increased profits), whereas regulators have practically no incentive to increase regulation. Banks employ armies of well-paid experts to plead their case to regulators and politicians and to show that what they propose will be good for the economy, and that what regulators propose (if banks don't like it) will be bad for the economy. Regulators stand no chance against such massed might. Banks have shown themselves to be very adept at such practices in the past and there is no reason to hope that they will be any less so in the future. For these reasons it is very unlikely that restrictions, however stringent, will provide a cure for the severe dangers that are inherent in the system. I believe that nothing less than a complete and radical redesign of the systems that create and allocate money will provide a permanent cure.

Without an effective and permanent cure for the ills of the banking system we can expect another great crash, when in all likelihood the sector will be 'too big to bail'.

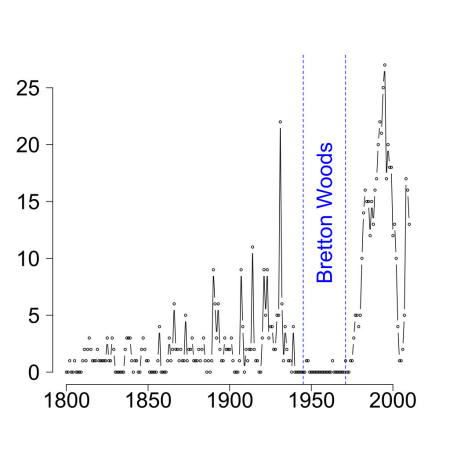

In addition to major crashes, such as happened in 1929 and 2008, minor crashes (known as downturns in the business cycle - driven by positive feedback in money creation - see chapter 52) and lower level banking crises happen all the time. These are also very damaging to society in causing loan foreclosures with loss of homes for individuals and loss of output and jobs for businesses. The following chart, figure 50.1, shows the number of countries having a banking crisis in each year since 1800. Note especially the Bretton Woods period after the Second World War. This represents a very unusual and stable period in economic history and is examined in more detail in chapter 67.

Figure 50.1: From Wikipedia 'List of Banking Crises' By DavidMCEddy (his own work) [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons. Source data taken from Reinhart and Rogoff 2009.

In summary, in its current form, banking has the following characteristics:

i. it is based on deception;

ii. it does major damage to society on a regular basis during business cycle downturns; and

iii. it does almost unimaginable damage to society when there are major economic crises.

For all that we get services that can easily be provided by other means - see chapter 55.