The economics of international trade, in spite of its complexity, rests on some basic foundations:

There are many very significant advantages to be had from international trade. Markets are much bigger so there is more demand for products and greater opportunities for economies of scale, and higher levels of specialisation are possible thereby improving efficiency. For consumers there is a much greater choice of products, including products that are completely unavailable in the home country. Consumers enjoy lower prices because of increased levels of competition from a wider range of suppliers. The economy as a whole also benefits. Exports bring in money that stimulates the economy without having to rely on domestic demand, and imports bring in wealth at less cost than would be required to produce locally. All this arises from the fact that the effort to create surplus wealth differs greatly in different countries and in different environments, so the UK buys bananas from Colombia because it would be very costly for us to grow them here, and Colombia buys gas turbines from the UK because it would be very costly for them to build them there.

However there are also disadvantages. Dependence on external markets can backfire if for any reason imported foreign supplies dry up or foreign consumption diminishes for exported goods. Domestic suppliers and their employees can be especially hard hit in specialised industries such as coal mining or shipbuilding when external competitors are able to undercut prices significantly. In such cases there are great temptations for the home government to apply protective measures such as import tariffs, limited quotas, outright bans or home currency devaluations - known as trade barriers - in order to protect workers, or to grant subsidies to enable home producers to sell products competitively. If this happens similar measures tend to be applied in retaliation by foreign trading partners in a tit-for-tat response, damaging both sides of the trade. In effect there is a paradox of thrift at the international level. Just as an individual can save effectively in isolation but if everyone tries to save at the same time then their efforts are ineffective because they stifle trade (see chapter 15), a country in isolation that applies trade barriers will find them helpful, but if all countries try to apply such barriers at the same time then they will be ineffective because they stifle international trade. In the past trade restrictions were extensive and commonplace, but in more recent times such barriers have been reduced significantly, though not completely. Neoliberalism strongly discourages any form of trade barrier and backs up that position using the 'Theory of Comparative Advantage', which purports to prove that countries are always better off by trading with each other rather than not, but as will be seen in the next chapter there are some serious objections to the assumptions that underlie that theory.

Problems also arise if there is a serious imbalance between a country's exports and imports. If exports exceed imports then foreign consumers benefit at the expense of home consumers, and if imports exceed exports then debts are incurred to the exporting countries - see section 65.5 below. Also spending on imports without balancing exports (more sellers of the currency than buyers) depreciates the home currency which shrinks the economy as spending power leaves the country.

For the world as a whole the sum of all international trade is zero - every export from one country represents an import to another country. Countries generally prefer to export rather than to import, because a country that exports more than it imports is like an individual that creates more wealth than he or she consumes - it increases wealth and power, but countries that pursue that policy, as do Germany and China amongst others, can only do so provided that other countries are willing to import their products.

An overall trade balance between exports and imports is a healthy state, but it isn't necessary to maintain a balance with every country that is traded with. Imports from China can be balanced by exports to Europe. This is exactly the same as individual trade, where buying from one person can be balanced by selling to another. I have a dreadful trade balance with the owner of my local garage. I regularly pay for servicing and repairs from him but he never buys anything from me - but neither of us loses any sleep over it!

A particular currency can only be used to buy wealth from those who accept that currency - normally those within the issuing country, so domestic currency normally only buys domestic wealth. Also wealth suppliers are usually only willing to accept their own currency in exchange, whether the buyer is domestic or foreign. In the absence of an international currency therefore exchange dealing is a necessary element of international trade. This doesn't apply to the same extent for reserve currencies - see 65.10.

With fiat currencies a country that imports more than it exports borrows the difference from the exporter even though the goods are paid for. This is not obvious, but imagine two desert islands, one that specialises in growing coconuts and the other in growing mangoes. They agree to trade coconuts for mangoes. Now if the first island imports mangoes before its coconuts are ready, what can it trade with instead? The answer, in the absence of anything else of equivalent value, can only be a promise to pay, which is precisely what fiat money is. In other words the first island pays for the mangoes in money - coconut currency - which, being fiat money doesn't have intrinsic value (if it did it would be an equivalent value export and no debt would arise) and is therefore nothing more than a promise to pay the equivalent back in coconuts in the future. In the meantime it is in debt to the second island. It is the very fact that the goods are paid for in fiat currency that creates the debt. Note that in this case the local currency of the importer is acceptable to the exporter, which is important because whenever this can be arranged it gives the debtor a great deal of control over the debt. The alternative, if the exporter won't accept the importer's local currency, is for the importer to borrow the exporter's local currency and pay for the goods with that. This is much less favourable to the importer because now the exporter has control over the debt. Both cases involve borrowing by the importer.

In this simple example there is a difference in these two ways of borrowing. If the person who imports mangoes pays in coconut currency then it is the importing country that has borrowed and the exporting person who has lent. The importing person has given coconut currency to the exporter and for the importer the transaction is complete. The exporter can use it to buy coconuts from anyone in the coconut country so it is the country as a whole that carries the obligation to send coconuts to the exporter rather than any particular person in that country. In effect the exporting person has lent mangoes in return for a coconut IOU from the importing country. If the importing person borrows currency from the exporting country then it is the importing person who has borrowed and a lender - a third party - in the exporting country who has lent. In this case the importing person has borrowed mango currency and used it to pay the mango exporter for mangoes, for whom the transaction is complete. The importing person retains an obligation to the lender, and can only discharge it by selling coconuts for mango currency and repaying the loan with that.

The real world doesn't work in either of those ways. Most currencies float freely against each other and are traded on foreign exchange markets, where currency dealers continuously balance sales and purchases of currency, changing the offer and bid prices in order to maintain that balance as closely as possible. In that way the individuals doing the exporting and importing don't need to bother about lending and borrowing, once the importer has arranged for the home currency to be exchanged and paid to the exporter the transaction is complete for both. In this case the importing country borrows and the exporting country currency dealer lends[247]. This type of exchange is explored in more detail in chapter 68. With countries that trade without floating currencies, China and the US for example, the importing country (US) buys in its own currency, which is exchanged by the central bank of the exporting country (China) for its home currency, so again the importing country borrows and the exporting country lends. Trade between the US and China is considered further below.

With fiat currencies a country that imports more than it exports must borrow the difference from the exporting country.

Let's consider further the point about debt in the importer's home currency being acceptable to the exporter. At the present time the US - the importer - is heavily in debt to China, because China holds massive quantities of the US home currency (largely in the form of government debt - treasury bills and bonds) in return for the goods that it has sold to the US.[248] At any time the US can reduce the wealth value of this debt by engineering a depreciation of the dollar - making it worth less in terms of tradable wealth - or by reducing the value of its bonds. It can depreciate the dollar by creating and circulating more dollars, thereby encouraging inflation; it can sell dollar currency in the market and buy other currencies, thereby reducing the demand for dollars and hence the value of the dollar; or its central bank can sell treasury bonds in the secondary market thereby directly reducing the value of China's bonds. All these actions have the effect of reducing the US wealth debt to China, whereas China can do very little on its own to maintain the value of the dollar. Ironically China has more economic interest in maintaining the value of the US dollar than does the US itself.

Conversely if the importer's debt is in the exporter's or some other foreign currency, then the value of that currency is out of the hands of the importer. If its value increases then the debt will grow, sometimes to enormous proportions. This has happened in the past in the case of developing economies and was ruinous for them - see chapter 73.

When gold was used for direct international transactions no debts were incurred because the same value of wealth was both exported and imported in each transaction, one side in gold and the other in goods or services.

Nowadays all countries trade with other countries, and all use fiat currencies. There must therefore be arrangements for exchanging currencies with other currencies, but these arrangements differ for different countries.

Most countries allow their currencies to be freely traded with other currencies, and there are two types of free trade. The first and now the most common is floating currencies, where the relative value of each is determined in the foreign exchange market by supply and demand. Values of floating currencies change all the time in response to many factors - see chapter 67 subsection 67.4.2. The other type of free trade is fixed or pegged exchange rates, where the rate is fixed by the government or central bank of the country in question relative to a stronger currency such as the US dollar or Euro. In this case the country's central bank holds a quantity of the stronger currency, and uses it to buy or sell its own currency to change the level of demand for it and thereby to maintain as far as possible the fixed exchange rate. If the amount of buying of its own currency by the central bank is excessive it’s because other people are selling it excessively – more importing than exporting - so the currency is devalued (the exchange rate moves downwards - less of the strong currency for one unit of the domestic currency) or, for excessive selling – more exporting than importing - it is revalued (the exchange rate moves upwards - more of the strong currency for one unit of the domestic currency).

Countries that don't allow their currencies to be freely traded arrange exchanges at state level by the government or central bank. Imports or exports to and from the country are paid in an external currency, usually the US dollar, and the state manages the exchange with the domestic currency. China is the most obvious case in point and avoids free exchange so as to keep the value of its own currency low (it would rise significantly if traded freely because China has a large excess of exports over imports). Chinese international trade is discussed further in section 65.8.

Even though currencies float, at any point in time they are tied together by the value of internationally traded wealth. If any currency is even slightly out of balance in this respect arbitrageurs - traders who make profits by searching for and exploiting price differences - rapidly bring them back into balance again. For example if zinc is trading at £1,000 per tonne and also at $1,500 per tonne, but the exchange rate is $1.4 per £1, a trader can buy 100 tonnes of zinc in the UK for £100,000 and immediately sell it for $150,000 in the US (transport costs can be ignored - see below), then exchange the $150,000 for £107,143, making a risk-free profit of £7,143. But this opportunity won't last long because every time dollars are sold and sterling bought the dollar is made weaker and sterling stronger, so the exchange rate soon approaches $1.5 per £1 at which point balance is restored. Traders in these markets buy derivatives (futures) linked to commodities rather than commodities themselves to avoid having to deal with physical goods. Arbitrageurs are also on the lookout for any anomalies between currency values themselves that are offered by the various brokers. Again any opportunity to make money is soon taken and as before the effect is to keep currency values in balance.

Imbalances between imports and exports tend to self-correct, provided that either a common currency is used or currencies are freely exchanged. If these conditions aren't met, such as when an exporting country retains the currency of the importing country, then the self-correcting tendency is absent. When these conditions are met a country that exports more than it imports finds that its exports become dearer in importing countries so export demand for them drops, and imports from foreign countries become cheaper so domestic demand for them rises, as explained below. The opposite happens if a country imports more than it exports. However, in order to work properly there must be adequate spare capacity available to expand export production when foreign demand rises.

Consider the case of a common currency such as gold, with two trading countries A and B, A exporting to B more than it imports. With an excess of exports gold is accumulated in A and diminished in B. An accumulation of gold tends to depreciate its value in relation to A's home wealth, so in A prices rise, which makes exports to B dearer for B and imports from B cheaper for A. Conversely for B gold is in short supply so its value in relation to its home wealth rises and prices fall, further strengthening the effect of making imports from A dearer for B and exports to A cheaper for A. Therefore exports from A diminish and imports to A increase, tending to correct the earlier imbalance.

With the same two countries using free exchange and floating rates there is more demand for A's currency when A exports more than it imports. B has to sell more of its currency to buy A's currency than A has to sell to buy B's currency, so A's currency increases in value relative to B's, and exports from A again become dearer for B and vice versa, again correcting the earlier imbalance. With free exchange and fixed rates B has to sell more of its reserves of A's currency in order to buy back its own currency from importers who sell it to buy A's currency, so as to maintain the value of its currency. Losing reserves prompts B to cut back on imports and promote exports, thereby correcting the imbalance, or, if it doesn't, then eventually it runs out of reserves and is forced to devalue its currency with the same result as with floating exchange rates, again tending to correct the imbalance.

Another condition can lessen the imbalance-correcting effect however and that is when populations are free to move easily from one country to another. In this case people who are able to move tend to do so to enjoy the greater prosperity available in the richer country - generally the one with excess exports. These people are generally wealth creators so a country that finds demand for its exports rising is less able to meet that demand. Free and easy population movement between countries is not common in the modern world though an exception is for populations within the European Union. This is considered in chapter 72.

The effect doesn't occur if there is no common currency and currencies aren't freely exchanged. For example China exports goods to the US but doesn't allow its currency, the renminbi[249], to appreciate against the dollar as it would do if it was freely traded. Instead China's central bank handles all renminbi currency exchange on behalf of the government by taking dollars from US importers and investing them in US securities, and paying out renminbi to its export workers, which it obtains by borrowing from its own population at low rates of interest. The Chinese population have little in the way of job or health security and so save heavily, but have very restricted investment opportunities available other than lending to the government. The exchange rate between dollars and renminbi is thereby completely controlled by China's central bank, and that prevents the dollar from falling in value against the renminbi but builds up massive investments for China in the US. This explains why both China and the US are heavily in debt - China is in debt to its own population and the US is in debt to China. The perverse effect is that the population of China, still very poor in spite of the country's recent growth, lends money in great quantities to the US (via the Chinese central bank), one of the richest countries in the world.

Most trade is carried out within a country's domestic economy. Very often, relatively poor countries whose currencies have low valuations have much cheaper domestic prices than the exchange rate would imply. This is because the exchange rate reflects the value of internationally traded wealth, not wealth that is only traded domestically. Most services are purely domestic and many locally sourced products, especially when perishable, are only available in the domestic market. In order to take account of these factors another comparative rate, more realistic in terms of the value of a currency to its own people, has been devised, called Purchasing Power Parity (PPP). This reflects the relative values of different currencies when used to buy representative baskets of goods. For example in 2015 the international exchange rate between Mexican pesos and US dollars was 16 pesos to the dollar, whereas for a representative basket of goods in each country one US dollar would buy the same in the US as 8.4 pesos would buy in Mexico, showing that in PPP terms the peso is worth almost twice the international exchange rate. The OECD publishes tables of PPP values as well as exchange rates.[250] In 2011 the World Bank published a report stating that the size of the world economy was $90 trillion in terms of PPP but much less at $70 trillion in terms of exchange rates, indicating the higher value of domestic wealth when calculated in terms of a common currency based on domestic exchanges rather than on international exchanges.[251]

A reserve currency (also known as an 'anchor currency', 'hard currency' or 'safe-haven currency') is a currency that is held in significant quantities by governments and institutions as part of their foreign exchange holdings. The reserve currency is commonly used in international transactions because it is acceptable to many other countries in addition to their own domestic currency.[252]

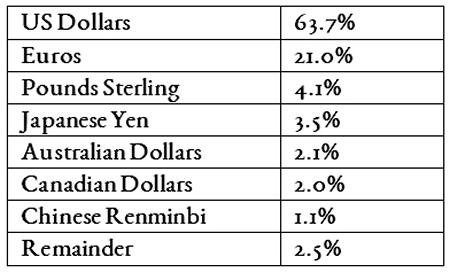

The distribution of reserve currency holdings at the end of 2014 were as follows[253]:

Table 65.1: Reserve currency distribution in 2014

As can be seen the US dollar is by far the world's most favoured reserve currency, meaning that central banks hold significant quantities of US dollars in preference to any other currency. Additionally many commodities are bought and sold principally in US dollars because it's easier to trade in a common currency, and after the Second World War the US dollar was the only viable currency for this purpose and it has retained that position ever since. When exchanging less common currencies it is usually easier to change the first for dollars and then change the dollars for the second, because all exchangeable currencies can be converted to and from dollars whereas they can't all be converted to or from each other. Chapter 71 deals with reserve currencies in more detail.