Free capital movement - the ability to buy and sell foreign assets including currencies and debts freely and in any quantity - was one of the changes ushered in after the collapse of the Bretton Woods agreement. It is strongly supported by neoliberal ideology.

The damage that can be done to poor countries when capital is allowed to move freely across borders has been discussed in the last chapter, but it also damages rich countries. Keynes and White recognised only too well the dangers during the Second World War when designing the post-war international trading arrangements - see chapter 67 section 67.2. What they wanted was to stimulate trade in goods and services, which benefits everyone provided that those benefits are shared fairly, and they saw clearly that free movement of capital can and does damage that trade. Keynes and White argued that freedom of movement for capital conflicted both with a nation state's freedom to pursue economic policies based on its own domestic circumstances - for example by stimulating a sluggish economy or by calming a racing economy, and also with the semi-fixed exchange rate system that was widely agreed to be important to maximise international trade in goods and services.[295] Since then White has been forgotten and everything that Keynes ever said and wrote is treated with contempt by neoliberals.

Many benefits are cited for free capital movement: money can be allocated to where it can do the most good; it enables investment in developing countries to aid their growth; it allows financial markets to expand; and it reduces the cost of capital because of increased lending competition. Before the crises that affected developing countries in the 1980s and 1990s it was widely regarded as unarguably beneficial, but since then it is becoming increasingly controversial, with even the IMF accepting that it might not be the universal good that it had believed it to be following the Bretton Woods breakdown.[296]

Joseph Stiglitz tells us what's really going on:

As a matter of simple economics, the efficiency gains for world output from the free mobility of labor are much, much larger than the efficiency gains from the free mobility of capital. The differences in the return to capital are minuscule compared with those on the return to labor. But the financial markets have been driving globalization, and while those who work in financial markets constantly talk about efficiency gains, what they really have in mind is something else-a set of rules that benefits them and increases their advantage over workers. The threat of capital outflow, should workers get too demanding about rights and wages, keeps workers' wages low. (Stiglitz 2012 Chapter 3)

The crux of the matter is that all economies depend on the circulation of money, as was shown in chapter 14. Anything that threatens that circulation threatens wealth creation, and wealth creation is what everyone depends on because we all need to consume wealth both to stay alive and to live a normal life. The free movement of capital across borders allows money to be transferred to where it can 'do the most good' - i.e. the most good for the owner of that capital[297] - which is not at all the same thing as the most good for trade or for individual countries.

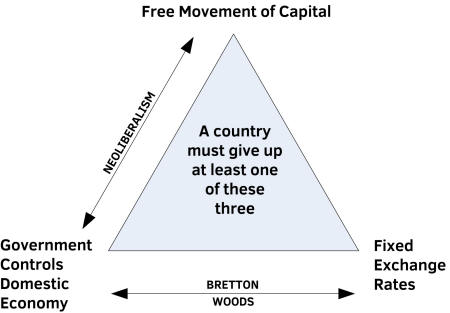

It was recognised as a result of bitter experience after capital controls were loosened that there are three policies that can't all operate at the same time:

i. free movement of capital;

ii. government control over the domestic economy (ability to set interest rates and control domestic demand); and

iii. fixed exchange rates.

At most only two of these three can exist together - this is known as The Impossible Trinity[298] (and also the Monetary Trilemma), shown in figure 74.1.

Figure 74.1: The Impossible Trinity

Before it was recognised there were several financial crises as countries attempted to maintain all three. The UK example occurred on 16 September 1992 when it was forced out of the European Exchange Rate Mechanism (ERM) by the action of 'the markets' on what became known as 'Black Wednesday'.

To see why it is true imagine the UK attempting to adopt all three policies at the same time with a sterling interest rate set by government at 5%. If in the US the interest rate is 10%, UK investors sell their UK investments, exchange the money for dollars at the prevailing rate and invest it in US bonds because they get a much better return on their money. As UK investors continue to do this UK investments fall in value and therefore the interest they pay rises in real terms, until it is the same as the US interest rate. Hence the UK government has lost control over UK interest rates, which are forced to match the dollar interest rate. In fact but for different expectations of inflation in different currencies and abilities of governments to repay, all interest rates would have to match each other with free capital movement and fixed exchange rates.

What most countries have chosen to give up since Bretton Woods is fixed exchange rates. China is an exception, giving up instead free movement of capital but keeping control of interest rates and exchange rates. This is the same as applied during the Bretton Woods era. This is significant.

The economy that has grown the most (now world number two) and lifted the most out of extreme poverty during the neoliberal era is China's, but China plays by Bretton Woods' rules, not neoliberal rules (Chang 2008 p27).

However it isn't as simple as that, as Rodrik shows (Rodrik 2012). When Bretton Woods collapsed and floating exchange rates took over, it was thought that rates would stay fairly stable, with supply and demand for traded goods and services setting the price in terms of exchange rate as they are supposed to do in other markets. What hadn't been considered was the effect of setting up a new gambling forum with speculators able to bet on exchange rate movements in the hope of making profits. Even that wouldn't have mattered so much if gamblers were completely independent of each other as they are assumed to be for market predictability - see chapter 34. But, as already discussed in chapter 57, financial markets are anything but independent; they are driven much more by what others in the market are doing than by objective assessment of value. As time progressed and speculation mushroomed, any exchange rate signals that there might have been from trade in wealth were drowned out by speculative transactions. In 2007 the daily volume of foreign currency transactions had risen to $3.2 trillion, whereas the volume of wealth trade was $38 billion (Rodrik 2012 p107) - eighty-four times as much speculation as genuine trade!

Another factor is that with free capital movement the raising or lowering of interest rates has a much smaller effect on the domestic economy than it would with capital restrictions. This was discussed in chapter 70 but in summary a government induced rise in interest rates, intended to slow a racing economy by reducing the money supply, will instead cause an inrush of spending from abroad for investment purposes, thereby offsetting much or even all of the intended decline.

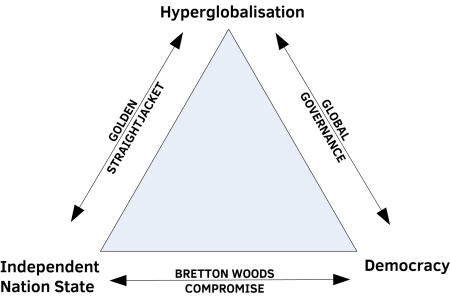

Therefore although the triangle gives the impression of three equally balanced factors, the free movement of capital is by far the most dominant.

Rodrik expresses this as another triangle, but here, instead of merely free movement of capital he takes it further, calling it 'hyperglobalisation' - which is the situation that neoliberalism drives us towards, consisting of:

· free movement of capital across national borders;

· opening up to foreign trade and investment of all national markets;

· enforcement of intellectual property rights across the world;

· disempowerment of national bodies for economic policy-making and regulation of health, safety and welfare standards;

· disappearance or privatisation of social insurance;

· low corporate taxation;

· removal of social compacts between business and labour; and

· subordination of national developmental goals to market freedom

(Rodrik 2012 Chapter 9).

The other two factors are Democracy, where government authority derives from the will of the electorate, and an Independent Nation State, where there is national rule, but any thought of government controlling its own economy has gone. This is The Political Trilemma of the World Economy, shown in figure 74.2.

Figure 74.2: Political Trilemma of the World Economy. Source: Rodrik 2012 p 201.

If we have hyperglobalisation then all matters relating to money and markets are determined at the world level and can't be set independently by an individual country. This is the same as a single region within a country, which must abide by the monetary policy and the markets of the country as a whole. The only way in which a nation state can be governed in these circumstances is by maintaining global monetary and market rules even when its population is severely disadvantaged by them. In effect the government is a dictatorship.

Rodrik cites Argentina between 1990 and 2002 as a good example, beginning with Cavallo's tying of the country's currency, the peso, to the US dollar in order to bring confidence back in its economy. At the same time privatisation and deregulation were accelerated, and the economy was opened up to world trade. Things went very well indeed for several years until the Asian crisis in the late 1990s, when investors' appetite for emerging market investments suddenly dried up. This was followed by Brazil devaluing its currency by 40% in 1999, thereby picking up exports at Argentina's expense. Soon the peso was under severe pressure and Argentina's creditworthiness collapsed. Strict austerity policies were applied in 2001 in an effort to shore up foreign investor confidence, but the internal strife that was unleashed proved decisive. There were strikes, riots and looting. Eventually the government was forced to abandon its monetary policies; it froze foreign bank accounts, defaulted on foreign debt, re-imposed capital controls and devalued the peso. In short democracy won the day over hyperglobalisation (Rodrik 2012 pp184-187).

Keeping hyperglobalisation and the nation state is known as the golden straightjacket, where the state is forced to follow the dictates of the world market. During hard times when productivity is low it can only do so by impoverishing the population. Democracy is sacrificed in these circumstances because a democratic country wouldn't tolerate the harsh conditions that world markets can inflict. The name evokes the gold standard that tied all economies together in this way before the First World War, when fully democratic politics hadn't yet emerged. In effect this is the situation that European countries using the Euro are in with respect to the European Union as a whole. Individual nation states still exist but they have largely lost democratic control over their own economic affairs. The conflict between democracy and European hyperglobalisation has been most sharply seen in Greece, where the population is reacting with great hostility to the straightjacket that they are forced to wear. The European special case was considered in chapter 72.

The Bretton Woods compromise retained the nation state and democracy, but severely restrained globalisation in terms of free capital movement and other international factors. The focus then was on trade in goods and services, and it worked very well until the Nixon shock in 1971 when the dollar was unpegged from gold. Had Keynes' Bretton Woods proposals been adopted instead of White's we would have retained the benefits in terms of world trade and democracy, and there would have been no Nixon shock - see chapter 84.

The other alternative is full globalisation, with democracy, a world government, world central bank, world judiciary and robust global regulatory institutions. This is an appealing prospect in many ways but the difficulties that would be faced are enormous. In particular if one or more countries wanted out because they strongly disliked the rules then how could they be stopped? Would the rest send in armed forces as in colonial days? I doubt that there would be widespread support for such a measure - I certainly hope there wouldn't. A world government would need very strong and lasting world support to retain legitimacy. However a world government would have responsibility for all people, so any who were disadvantaged as a result of changes in trade patterns and improvements in technology would be looked after (hopefully) until they could find new employment. In addition to this global safety net there would be a global lender of last resort, a global monopoly watchdog, and a series of global regulators for all health and safety aspects of the global marketplace. This is the same as happens in existing developed countries where all such governance measures are in place in some form.

At present we have a world economy that mirrors practically all the characteristics of a single country economy, but without any of the safeguards.

As Rodrik said:

...markets and governments are complements, not substitutes. If you want more and better markets, you have to have more (and better) governance. Markets work best not where states are weakest, but where they are strong. (Rodrik 2012 p xviii)

Rodrik is right and we need to face the problem that emerges from his insight. We must recognise that the more we drive towards hyperglobalisation the more we drive out democracy. Allowing the rules to be set by strong business interests, i.e. undemocratically, is dangerous. Not only are the majority of people severely disadvantaged for the benefit of the very few, but there is no way that such a system can face up properly to the social dangers posed by climate change. Private interests will never voluntarily pay for public goods or pay to avoid public or environmental harm, they will and indeed can only pay for things that deliver private profits. On occasions when they do appear to pay for such things voluntarily they are really paying to enlist public support so as to enhance profits.

To quote Rodrik again:

So we have to make some choices. Let me be clear about mine: democracy and national determination should trump hyperglobalisation. Democracies have the right to protect their social arrangements, and when this right clashes with the requirements of the global economy, it is the latter that should give way. (Rodrik 2012 p xix, his italics.)

Voices in favour of restrictions on the free movement of capital are becoming more widespread. A report by the New Economics Foundation[299] written on behalf of the Green New Deal Group[300] stated:

In June 2005, the Bank for International Settlements, perhaps one of the most conservative institutions in the financial system, addressed the problem of global imbalances and suggested that the international financial system could 'revert to a system more like that of Bretton Woods'. It added that 'history teaches that this would only work smoothly if there were more controls on capital flows than is currently the case, which would entail its own costs.'

Such controls would not be hard to police. Large financial movements are tracked already by national authorities, in the name of 'anti-money laundering measures'. They use the technology that makes possible almost instantaneous money transfers and split-second dealings in cash and securities around the world. Moreover, there is a low-tech reinforcement for this high-tech equipment. Contracts or deals entered into in offshore jurisdictions, or anywhere else, in defiance of financial controls could be declared void in British law. This 'negative enforcement' is highly attractive. It requires no police; it relies simply on British courts not doing something, i.e. recognising and enforcing financial arrangements made without authorisation.

Both these methods of enforcement also give the lie to the objection that financial controls can work only with international agreement.

Michael Meacher cites the above in his book (Meacher 2013 p172) as well as a BoE report issued in December 2011.[301] Meacher states:

A Bank of England paper released in December 2011 points out that under the Bretton Woods system (1944-71) of fixed exchange rates and capital controls, compared with floating exchange rates and deregulated capital flows that followed after 1980, growth was higher, recessions were fewer and there were no financial crises. It notes that governments were able to pursue their domestic objectives without the constant fear of destabilising flows of hot money. The paper concludes that 'the period stands out as coinciding with remarkable financial stability and sustained high growth at the global level.' In terms of trading balance enabling governments to deliver strong non-inflationary growth, the capacity to allocate capital efficiently and the achievement of financial stability, the paper argues that 'overall the evidence is that today's system has performed poorly against each of these three objectives, at least compared with the Bretton Woods system, with the key failure being the system's inability to maintain financial stability and minimise the incidence of disruptive sudden changes in global capital flows.'

The free movement of capital hands wealthy people and corporations a very strong lever over governments in that they can move their wealth out of the country very easily and thereby damage national economies. Fear of this power forces governments to respond to their interests rather than the interests of the society that elected them.