10 The investor perspective on business models

(Written by Christian Nielsen, Associate professor, PhD)

[Please quote this chapter as: Nielsen, C. (2012), The investor perspective on business models, in Nielsen, C. & M. Lund (Eds.) Business Models: Networking, Innovating and Globalizing, Vol. 1, No. 2. Copenhagen: BookBoon.com/Ventus Publishing Aps1st ]

Disclosure of information on strategies, business models, critical success factors, risk factors and value drivers in general has gained importance in recent years. Both policy makers and academics have argued that the demand for external communication of new types of value drivers is rising as companies increasingly base their competitive strengths and thus the value of the company on know-how, patents, skilled employees and other intangibles.

In parallel with the focus on disclosure of value drivers, the concept of business models has gained popularity. However, business models in terms of “ways of doing business” have always existed. The business model reflects the way of competing of the specific company, whether it concerns being unique or being the most cost-efficient company in the industry. The supply of information on the value creating processes and value drivers of firms has actual y been increasing in various reporting media such as annual reports, IPO prospectuses and the reports of financial analysts. Furthermore, some firms, especial y in the Nordic countries, have started developing Intellectual Capital (IC) reports that communicate how knowledge resources are managed in the firms within a strategic framework, and new models for reporting on stakeholder value creation and CSR are gradual y emerging. Despite this, an explicit recognition of value creation as a central part of a business model is general y lacking in this literature.

It is also noticeable that even though disclosure of information from companies has been increasing, there are no clear signs that the particular information demands of investors and analysts have been met. The paradox is therefore that while there are well-developed arguments for disclosure and evidence indicates that companies are disclosing more and more information, there are also indications that disclosure quality is insufficient at the present. This leads us to consider whether we are facing a reporting gap, or rather an understanding gap. This is where the business model can be applied.

There is a multitude of evidence that the nature of the business environment is changing. Among the factors that drive this development are the globalization of markets, greater mobility of the workforce as well as monetary and physical goods and the application of information technology and technology in general. As the above factors and greater integration of capital markets cause changes in the nature of value creation, and new competitive elements gain importance, new types of disclosure and reporting that are argued to be so vital for conveying transparent pictures of the corporate well-being are unfortunately not without problems, as these types of information are somewhat more complex than traditional financial information.

It could very well be a problem that the capital market agents simply do not understand non-accounting information. Perhaps business models enable the creation of a comprehensive and more correct set of non-financial value drivers of the company and are therefore a useful reference model for disclosure. In the near future, western-society citizens will be questioning not just the future of the financial sector of the western world, but also the sustainability of the industrialized western society as a whole.

On the one hand, pressure from under-burdened western society taxpayers (voters) who crave an average working week of 35-37 hours and retirement 40-50 years prior to their death will be on the rise. On the other hand, eager hardworking Asian and Indian consumers with surprisingly well-educated workforces will lead us to be questioning our chances of economic survival in a truly globalized world all throughout 2012.

One possible answer to this problem is that western societies to a greater extent need to rely on human capital in the quest for private sector value creation, innovation and competitiveness. However, human capital will not make the difference alone. Only when complemented by triple-helix based innovation structures, creativity and unique business models that commercialize innovation and human capital will this be an avenue to future sustainability.

It is in this connection that the financial sector needs to start understanding new types of business models and hence also new types of information. Environmental, Social and Governance (ESG) information is a good example. It is today solely used by the buy- and sell-side in ex post audit society screening manner. We need to ambitiously pursue ex ante screening as a first step and then quickly move to actual active use of ESG information and information pertaining to sources of value creation in investment decisions. We should be hoping to see the first modules on analyzing business models and ESG information on post-graduate, MBA and CFA levels soon. At least for the sake of sustaining western society as we know it, we hope so!

10.1 Information needs of investors and analysts

While disclosure of information has been increasing, there are no clear signs that investors and analysts’ demand for information has been met. Eccles et al. (2001, 189) conclude that managers “genuinely believe they try hard to give the market the information it wants. But most analysts and investors believe managers could try harder”. Literature is abundant with well-developed arguments for better disclosure, and empirical studies document that improved disclosure is related to e.g. increased analyst interest in the firm, lower cost-of-capital and decreased bid-ask spreads.

Back in the 1990’s various studies of investors and analysts’ request for information indicated a substantial difference between the type of information found in company annual reports and the type of information demanded by the market, and more recent studies show only limited improvements with respect to disclosure practises in the firms.

Companies have clearly become aware of the importance of managing their external communication systematical y, and the importance of investor relations is increasing. Also, investors and analysts are becoming more aware of the importance of factors not included in the financial statement, although traditional financial information is still considered to be of greatest importance. The general tendency emerging both from surveys of information needs and normative reports is that the capital market actors request more reliable information on e.g. managerial qualities, expertise, experience and integrity, customer relations and personnel competencies since these factors are considered important for the ability of the company to generate value.

Much of this information is, however, too complicated to summarise e.g. in annual reports. Furthermore, experiences from the management literature with respect to new strategic reporting models as for instance the balanced scorecard approach or intellectual capital reports show that it is just as complicated for management to define what factors are actual y the few most important drivers of future performance, as it is for external stakeholders to understand such information when it is disclosed.

Related to this a recent report (KPMG 2003) based on answers from a sample of non-executive directors in the U.K indicated that while 94% of the respondents considered themselves to have considerable knowledge of financial performance measures, only 60% considered themselves sufficiently knowledgeable with regard to non-financial measures such as critical success factors, strategy etc.

Major questions regarding how this information should be defined, how it should be structured, and how it should be communicated to the market still remain to be answered? Furthermore, from the perspective of the capital market, similar questions arise:

• How should the information be used?

• How can it be trusted?

• How should it supplement traditional financial information?

• What overall framework can support the evaluation of the firm’s strategy?

10.2 Background on the market for information

According to Ball (1996, 11), the theory of efficient markets is an imperfect and limited way of viewing capital markets as the prescriptive theories of finance on which the Efficient Markets Hypothesis is based, widely ignores the human nature of the participants that constitute the capital market and especial y the three groups of opinion-formers:

• Company management

• Sell-side analysts

• The fund management function

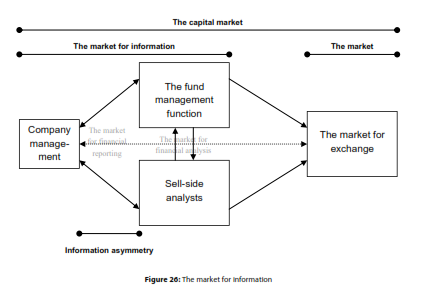

In order to understand the functioning of the capital market correctly, we must make a distinction between the market for exchange and the market for information (see figure 26). This distinction was first introduced by Gonedes (1976), who argued that many of the assertions of traditional finance theory were misleading, because they did not deal with the relevant part of the capital market, i.e. the market for information. By relevant, Gonedes (1976) meant those groups of actors that were the major opinion-makers with respect to valuation, and he, furthermore, argued that “failure to explicitly consider the market for information may induce unwarranted inferences about the capital market” (1976, 628).

Barker (1997), depicting the relationships between companies, analysts and fund managers, argues that there are two ‘information markets’ co-existing in the market for information, namely the market for financial reporting and the market for financial analysis. In his subsequent study, Barker (1998) concludes that the market for financial reporting is of considerably greater importance than the market for financial analysis. With respect to the market for financial reporting, other disclosures from the company than merely the annual report must also be considered, e.g. press releases, earnings announcements and conference cal s. The market for corporate disclosure might therefore be a better description. The market for financial analysis can be perceived almost as an intermediary function, however not neglecting that investors too receive information directly from the company itself.

Barker (1998) analyzes the economic incentives with respect to information flows between these actors, arguing that these incentives must in some manner also reflect the tasks carried out. Barker (1998, 16) finds similar economic incentives between management and fund managers, “both having a similar time horizon on a benchmark of relative share price performance, and both take great care to avoid negative surprises”. Barker also concludes that because of the economic incentives connected with the turnover– based commission income of the analysts, the analysts in contrast favour share price volatility rather than stability (Barker 1998, 16). Despite the fact that fund managers consider financial reporting and formal meetings with company management more important than the analysts, their role in the market for information is seen as a “news agency and a source of valuation benchmarks” (Barker 1998, 16).

Holland & Johanson (2003) problematize the abilities of the market for information participants to incorporate new types of information on e.g. intellectual capital and the value creation process of companies into valuations. They argue that because the fund management and analyst functions have difficulties understanding even their own value creation process and intellectual capital, then how can they be expected to understand those of the companies they are analyzing and investing in (Hol and & Johanson 2003)? Furthermore, Hol and & Johanson (2003) argue that ambivalence towards using new types of information is attributable to the institutionalized nature and culture of these actors. This is accentuated by Ikäheimo (1996, 30), who argues that “[t]he value of a share is derived from a consensus based on the institutionalized conception of how the value of the company should be perceived”.

The statements above bring relish to a dilemma and unexplored avenue in relation to the decision-making of the market for information participants. To minimize uncertainty and risks in investments, market for information participants and other actors in the capital market wish to base their decisions on full information, i.e. from a rational, consequential set. However, as indicated above, they do not understand new types of information otherwise regarded as highly value relevant. Therefore, although they want their decisions to look consequential, they are in fact characterized by the logic of appropriateness. Furthermore, as practices and rules-of-thumb to incorporate and understand new types of information are not presently institutionalized, the market for information participants face grave difficulties when packing and unpacking such disclosures.

Hol and has conducted a number of studies in relation to the market for information participants and the dissemination of voluntary information between them. Hol and (1998) concludes that private information disclosed to institutional shareholders is a significant part of a larger corporate decision concerning public versus private voluntary disclosure. Furthermore, Hol and & Doran (1998) have examined financial institutions’ application of private information channels, finding that these invested much time and effort in cultivating relationships in order to gain an information edge over the market.

In a later study, Hol and (2002a) has found that the limitations of finance theory and the limitations of corporate disclosures and other public domain information sources cause uncertainty in stock selection and in asset allocation decisions for fund managers. Final y, Hol and (2004) argues that the fundamental mosaic is the cornerstone of communication between the ‘market for information’s’ participants. According to Hol and (2004, 67), the fundamental mosaic: “provides a coherent means to tie together this information in a broader picture and to assess the impact on corporate valuations and it provides a means to check corporate promises against reality”.

In 2009 John Hol and refines his thoughts on the mosaic of information even further in his paper ”Looking behind the veil”: invisible corporate intangibles, stories, structure and the contextual information content of disclosure. Here he depicts three archetypes of value creation processes used for telling the business model story, namely 1) hierarchical (from top management), 2) horizontal (operational value creation), and 3) network (or alliances and strategic partnerships).

Hol and explains: “The hierarchical aspect of the corporate value creation story concerned common structures and categories of strategic drivers across companies. The hierarchical narrative concerned the story of the board, its directors, and board committees as the primary internal corporate governance mechanisms. This narrative explained how the board chose top-management and incentives schemes, how top-management in turn developed and implemented a coherent strategy and how this was monitored by the board. … The hierarchical narrative revealed top-down drivers of the value creation process. These primary drivers included top management qualities, coherence and credibility of strategy, management remuneration schemes, and corporate performance systems based on shareholder value.”

Further, Hol and writes that: “Each case company also articulated a concept or idea of its ‘horizontal’ or operational value creation process consisting of input sourcing decisions, transformation decisions and processes, and output decisions. This value creation process was normal y conducted at middle management and employee operational levels. It was often the critical part of the corporate value creation story showing how a case company differentiated its economic transformation processes from those of its competitors in the same sector. … The network value creation narrative sought to explain how the company sought to create many shared knowledge intensive competences at the boundary of the company. This normal y involved the sharing both of tangible and intangible value drivers via supply, production and marketing alliances at various points in the corporate horizontal value creation process. It often involved sharing of unique or otherwise unobtainable intangibles.”

Final y, Hol and concludes that the business model narrative, or strategic story, normal y connected many of the key elements in the value creation process. This was communicated external y to investors via a narrative connecting hierarchical, horizontal, and network value creation processes and the concept of an intangible, and its relative ranking, was given additional meaning by being placed and linked within the larger value creation story during the private question and answer sessions. This provided evidence and gave credibility to both the story and the relative ranking of the unobservable intangible factor. The combination of the narrative about the three value creation processes, the use of benchmark indicators or measures, their placing and linking within the story, all helped case companies provide the required ‘full story’ or ‘big picture’ to investors.

10.3 Gaining a competitive edge in the market for information

There is an intricate and rather delicate relationship between analysts, investors and management, which at the same time is located in an extremely competitive context (Fogarty & Rogers 2005). It is an environment of secrecy amongst the competing analysts, who all seek to gain some sort of competitive advantage in relation to their peers. The notion of having been or being able to gain a competitive edge over the market can mean a variety of things. For the financial analyst, there are basical y three ways to do this; it can e.g. pertain to having information that others do not have access to, having a unique perspective, or simply to having better analytical skil s.

Firstly, possessing a piece of information about a firm that none of the competitors have, is an obvious competitive advantage. As there are strict rules and regulations with respect to having price sensitive insider information, this sort of competitive edge is typical y mobilized through expert contacts, e.g. specialists in the specific field of a specific company or through col aboration across offices within the larger investment banks. In this manner, having an information edge is more likely to mean having a more detailed account of existing information, rather than new information that nobody else has.

In this respect, having a good relationship with company management teams and investor relations departments is a key to gaining a competitive edge, as more details on specific elements of the firm (Barker 1998, 16) or e.g. an alternative management perspective on a piece of information might be shared through private dialogue. According to Francis & Philbrick (1993), the analyst relies on his relationships with corporate executives for information and analysis that is not widely disseminated. Such relationships, which may be conducted through visits to corporate headquarters, telephone cal s with senior executives, or in group settings, are crucial to the analyst in establishing his claim to expertise (Philips & Zuckerman 2001, 393), i.e. competitive edge.

Also in relation to new information, the ability to be quicker to the market than competitors with newly disclosed information, e.g. in connection with earnings announcements, is another important competitive advantage. Typical y, trading is stopped for 2 minutes around an earnings announcement. Within this interval the analyst must download and skim the report and be able to point out the direction in comparison to previous expectations to the sales-desk. For some analysts this is a crucial part of their job, while others do not see their value adding tasks in this situation. With respect to analyzing the company, having a competitive edge can either come through being the fastest, e.g. in connection with earnings announcements, or having the best analytical capabilities.

A key competitive edge, an analytical edge, is being the best at interpreting existing information. Frankel et al. (2002) find that analyst research helps prices reflect information about a security’s fundamentals. This indicates that while the analysts’ role may restrict itself to merely pre-announcing earnings numbers in connection with annual earnings announcements etc., their real value-adding activities relate to the more fundamental research and understanding of the company value creation logic, strategy etc.

Typical y, the analysts create informativeness in comparison to the fund managers themselves and thus justify their existence by specializing by industry (Al-Debie & Walker 1999, 262) and by utilizing synergies between research functions within the investment bank. In relation to this, Desai, Liang & Singh (2000) find that stocks recommended by analysts following a single industry outperform those recommended by analysts following multiple industries. Hence, also the precision of their forecasts, which is a key point on which they are evaluated by investors, is a competitive edge.

Analysts seem to have their raison d´être where complexity is greatest. However, there is also evidence that even analysts have difficulties in making forecasts in certain situations, e.g. where knowledge– resources constitute a major part of the company value (Lee 2001), difficulties that could pertain to the inadequate applicability of conventional measurement and valuation approaches for such purposes (Lee 2001, Garcia-Ayuso 2003). Plumlee (2003) finds that information complexity imposes sufficient costs even on expert users and reduces their use hereof. Therefore, analysts’ abilities to incorporate complex information in their analyses are a decreasing function of complexity and information processing costs. For instance, Bukh (2003, 53) argues that disclosing intellectual capital indicators without disclosing the business model that explains their interconnectedness leaves the analysts to do all the interpretation; something which they are not capable of. Garcia-Ayuso (2003, pp 60-61) questions the credibility of analyst recommendations in this light, vindicating for a bounded rationality perspective on analysts’ cognitive abilities.

Investors and companies rank analysts differently, and even though some analysts are not the most accurate, they can still have the highest rating because their competitive edge comes from their ability to provide e.g. a new perspective on the firm (Beunza & Garud 2004, 14). Therefore, having a perspective edge, also termed ‘a unique case’, is a source of competitive edge. Beunza & Garud (2004) conceive analysts as makers of calculative frames. Analysts calculate, but they do so within a framework. According to Beunza & Garud (2004), analysts may appear to conform, but they also deviate from the pack to generate original perspectives on the value of a security, and, occasional y, displace prevailing frames.

The analysts rely on the factors mentioned above to gain an advantageous standing in the eyes of the investors, who then, in turn, trade through the analysts’ investment banks and furthermore participate in rating the analysts among one another (Phillips & Zuckerman 2001). Typical y, analyst ratings are a proxy for how much of their trading volume the investors will place at the respective investment banks, and as trading volume is what pays for the analyst services provided, the analysts live and die by their rating; hence the degree of competitiveness between analysts. Because analysts are dependent upon their customers, the investors, for their survival, it is appropriate to consider analyst reports as proxies for investors’ information demands.

From the analyst point of view, indicators disclosed in the annual report or in a supplementary report only constitute one part, maybe even an inferior part, of the information needed to make recommendations to clients, because they are in a privileged position to “get more information – and sooner – than all except the very largest investors” (Eccles et al. 2001, 274) . It might be that the information has value relevance, but the analysts have already a much more detailed understanding about e.g. the research and development activities, than that which can be gained from reading about the aggregated research and development expenses.

Taking the above description of the different angles towards gaining competitive advantage as the point of departure, let us briefly reflect upon how different ‘types’ of analysts position themselves accordingly within the market for financial analysis. Analysts are not a homogenous group of people (cf. Day 1986), although it has been suggested that their behaviour and understanding of social norms are indeed extremely similar (cf. Norberg 2001, Hol and & Johanson 2003). In the following, let us distinguish between two types of analysts, namely the small cluster and the large cluster analysts, where cluster refers to the amount of companies they actively follow on a daily basis. The large cluster analysts typical y focus on 10-20 different companies, whereas the small cluster analysts concentrate on 4-8 companies.

There are large discrepancies between their job descriptions, i.e. their client contact activities, and also with respect to the customer segments that they serve, i.e. private or institutional investors. General y, the large cluster analysts have more and smaller clients, while the small cluster analysts general y serve fewer and larger institutional clients. Also, the large cluster analysts have a closer connection with the traders of their respective investment banks – some of them even taking orders from clients.

These differences also have an effect on the type and detail of the research that they conduct and the thoroughness of the analyst reports in which they disseminate their results. Like with the analysts, there are also two types of analyst reports; the scheduled or earnings analyst report, and the fundamental analyst report, where fundamental analysis can be described as determining the value of corporate securities by a careful examination of key value drivers such as earnings, risk, growth and competitive position (Lev & Thiagarajan 1993, 190). Not all analysts conduct the so-called fundamental analyses, as it is not a part of their job descriptions. This typical y relates to the type of analyst in question. This will be discussed further in connection with evidence provided in the empirical analysis below. As this paper focuses on gaining knowledge about how corporate reporting can be enhanced by investigating the types of information analysts consider important in their fundamental research, the point of departure for the empirical analysis will be fundamental analyst reports.

Studying financial data in relation to analysts’ decision-making processes, Gniewosz (1990, 227) finds that the annual report is still considered the most important source of information (see also Brown 1997), although it is seen as having mainly a confirmatory function, rather than a primary information function, and a disciplinary effect on other corporate disclosure media (Christensen 2003). A number of studies have likewise examined the analysts’ decision-making processes (cf. Schipper 1991) e.g. in connection with screening of prospective investments (Bouwman et al. 1987; Bouwman et al. 1995). A number of different foci have been uncovered, for example how analysts’ decisions are products of group environments (Francis & Philbrick 1993), the identification of the most widely used valuation practices among analysts (Block 1999, 91; Plenborg 2002), and the uncovering of the various stages in the valuation process (Gniewosz 1990, Mouritsen et al. 2002a).

There seems to be some evidence pointing towards a context-specific use of valuation metrics. It has been indicated that fundamental strategic analysis is more appropriate for valuing younger firms but also more specifical y new ventures, while the more capital-based valuation metrics, such as discounted cash-flow and Price/Earnings, are more aptly applied to mature firms.

Confirming the greater difficulties of valuating relatively new investment objects (the capital market’s version of the company), be they companies, new ventures or spin-off projects, and also investment objects characterized by consisting to a great extent of intangible assets, Mouritsen et al. (2002a) depict a seven-stage model whereby the valuation process of such “businesses” can take place. In relation to this challenge, Hägglund (2001) describes more closely how investors and analysts work together in this process. Hägglund’s research, focusing on the conceptualization of the company rather than its value, il ustrates the complexity of the flow of funds to companies through the capital market and that the process also encompasses social and behavioural aspects.

Luehrman (1997) states that traditional valuation approaches may have become obsolete in the light of the recent changes in the nature of value creation from tangible to being predominately intangible of nature. However, the market for information participants still need relevant information in order to enable correct and accurate valuations of the firms, i.e. to get as close to intrinsic value as possible. On the basis of these facts, Mouritsen et al. (2001) suggest that three different types of capital must be valuated in order to get a correct picture of the value of the company. These are social capital, financial capital and “wise” capital, the latter including factors such as strategic knowledge and knowledge on organization and control.

10.4 Information trigger-points for investors

Events that cause significant movements in the stock price are called triggers. The term trigger is used in relation to initiating research and valuation of the company. Applying analyst terminology, trigger points are typical y fundamental changes that alter the value of the company, e.g. changes to growth and value drivers or changes in the macroeconomic environment. In a sense, triggers represent possibilities for earnings surprises.