Here’s the key to The Barefoot Retirement Plan. It’s based off of a little known unique variation of an asset that has been in existence for over 150 years called dividend-paying life insurance.

It’s all made possible by a congressionally approved IRS Tax Code # 7702 that allows us to have all the amazing benefits of the Guaranteed Index Account mentioned above through the use of Indexed Universal Life. Otherwise known as an IUL. Who would have thought that the Government allows all of these benefits through the use of Index Universal Life? However, keep in mind, this is NOT like anything else you’ve ever seen.

So yes, we are talking about a form of life insurance. But it’s a highly specialized form of insurance. What we’re doing is using a form of permanent life insurance as a savings vehicle the same ways the largest banks in the world are using it.

Don’t be surprised if you’ve never heard of it. As a general rule, most insurance agents, financial planners, financial media “experts” and stock brokers don’t have a clue about this nor do they even come close to understanding it. The masses know nothing about this. You know what they say, “If you follow the masses, you’ll end up in the same place as the masses.” Believe me, retirement wise… you don’t want to end up where the masses are.

The first thing that pops into a lot of people’s heads is something like this, “Hey, my brother-in-law sells insurance, so I’ll talk with him about this and see what he thinks.” That’s fine, but keep this in mind.

Probably less than 1 in a thousand insurance agents has even heard of this concept and far, far fewer of them have any specialized knowledge about this at all. Plus, this specific product is 100% EXCLUSIVE to our private distribution channel. Anyone outside of our distribution channel CANNOT offer this program and does not have access to it.

Out of approximately 1,000 major life insurance companies, only a small handful of them offer policies that have features similar to the ones we offer. When you couple this with the fact that there are advertising limitations on these types of policies and with the fact that agents typically make 50% to 70% less commission when selling these policies, it’s easy to understand why most people have never heard of this.

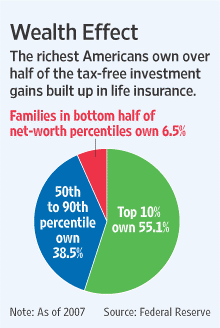

As you can see in this pie chart created by the Federal Reserve, the top 10% of the wealthiest Americans own over 55% of some form of this type of insurance. Furthermore, not shown on the chart but reported in the Federal Reserve findings was the fact that the wealthiest 1% own 22% of this type of insurance. That tells you a lot right there. The average person is never going to hear about the strategies the rich use to grow their wealth.

Setting up one of these policies is a lot like going to a medical specialist. If you have a problem with your heart, you’re not going to go to a general practitioner, right? You’re going to go to a heart specialist. You wouldn’t go ask your brother-in-law about your heart, unless of course, he/she happened to be a heart specialist. The same is true in this case.

If you go to someone who does not specialize in this form of IULs, you can risk everything. There are lots of variables, options and sophisticated strategies that need to be considered and specifically used to set these up properly. If they are not set up correctly, you can open yourself up to having the policy fail altogether or even open yourself up to large unnecessary tax liabilities.

Our Barefoot Retirement team specializes in setting up these unique and specialized policies. We’re happy to schedule a free strategy session with you, discuss your needs and options in great detail and produce various illustrations that will clearly show you how a properly structured IUL policy can have an amazingly positive impact on your retirement. It can even allow you to have a barefoot lifestyle retirement, living life on your own terms.

Fox Business published an article by Scott Mann titled “(Legally) Cutting Out the Tax Man in Retirement. The article states, “The life insurance industry has the best IRS-approved retirement savings plan today—, and most investors know nothing about it.” “Despite sales of well over $1 Billion in 2011 for the top 39 carriers surveyed, it is the financial industry’s No. 1 secret—Indexed Universal Life (IUL).”

The article went on to say, “To explain why IUL is a powerful supplemental savings vehicle to an employer’s 401(k) plan, and a replacement for those whose employers don’t offer one or for some people who don’t trust the market, we need to start with the fact that after a generation of use, qualified plans - comprised of equity-based investments - are generally acknowledged as failures.”

Fox Business published an article by Tim Fussell titled, “Is There Really A Perfect Life Insurance Contract?” The article concluded that there was no one perfect policy that can solve everyone’s needs and there are trade offs with each one. However, it went on to say, “But an emerging and fast-growing contract design - the indexed universal life (IUL) policy - may come very close to being the ideal contract for most consumers in today’s interest and overall market environment.”

Timothy R. Fussell also published another excellent article on Fox Business titled, “Indexed Universal Life Insurance Policies: The Perfect Option for Professionals and Business Owners.” In this article, he states, “For a professional such as a doctor, attorney or CPA, the Indexed Universal Life policy is perfect for your retirement needs. Often as a professional, you operate as a P.A. being taxed as a sole proprietor, an S Corporation or a C Corporation, and under the tax codes you are limited to retirement account choices. The SEP IRA, Solo-401k or the UNI-401k, all allow you to save on a tax-deferred basis; but the maximum contribution limit is still the same, $49,000.”

“Now let’s explore the IUL (indexed universal life) and why it is a better choice. As a professional of these types, your income level is much higher than average, so you max out your contribution very early in the year. With the IUL, there is no limit on how much money you can contribute…”

You may have heard of a variation of this concept before. It’s sometimes called things like; Bank On Yourself, Becoming Your Own Banker, a 770 Account, Tax-Free Retirement, etc. The HUGE majority of plans like this rely on a form of Whole Life Insurance. The “special” version of Indexed Universal Life (IUL) that we use for our program is vastly different and easily outperforms these other plans by a mile. I mean it’s not even close, and we’ll prove it to you in black and white.

Most of these other insurance policies focus on the Death Benefit. While that’s important, and it’s definitely part of our program, it makes the insurance part of the policy VERY EXPENSIVE.

When an insured person dies, all the other life insurance policies are structured to offer beneficiaries a choice of a Lump Sum Payout OR Payments Over Time. It’s just been that way for well over a hundred years, and it has always worked well. So if someone died with a million-dollar life insurance policy, the beneficiary could choose to either take the million dollars in a lump sum, all at one time, OR they could choose to receive payments over time, per a schedule they choose for payments.

If you were the insurance company, you would need to accrue to have the million dollars available to give the beneficiary if they choose the lump sum option, and it’s very expensive to do that. However, if the insurance company did not have to make that lump sum of money available, they could keep that million dollars invested in other, longer term, productive assets and growing much faster.

A very wise man who is part of our association came up with a brilliantly simple idea that changed everything. He developed this concept; IF you did not give the beneficiary an option to choose a lump-sum payment, and only gave them the option to receive payments over time, this one little change would greatly reduce the cost of insurance and thus allow clients to put a much greater amount of capital to work for them, growing their retirement assets even more.

This may seem like a small thing, but the results it yields are huge! You’ll see just how huge it can be shortly, when we show you some scenarios.

This little change can reduce the cost of the insurance by up to 70%! That makes this type of IUL MUCH Less Expensive.

(Note: If the policy holder wishes, we can still structure an IUL policy that does offer a lump sum payout if they choose it, but it does make the cost of insurance greater. We have the flexibility to structure any type of insurance program that best suits our client’s individual needs.)

Trust me when I tell you how much less expensive our choice is. Many of the people out there who sell Whole Life Insurance are quick to tell you theirs is similar in price. It’s not. Not by a long shot. If you are considering a Whole Life product or ANY other type of insurance product, I challenge you to carefully compare prices. You will be shocked at the difference! Ours offers much more value and benefits, for much less cost! Our version of IUL is like buying a Lamborghini at bargain basement costs.

You may have heard one of the complaints about the “regular” type of Whole Life Policies is that the agents make a TON of money on them. It’s true. Agents make a lot of commissions on them, and I’m sure you know; those commissions come from somewhere, right?

When agents sell the specialized type of policy that we are talking about here, they usually make 50% to 75% LESS, than the guys selling the Whole Life.

Almost every week we meet with other insurance agents who are interested in joining our team, so they can gain access to this specialized program and offer it to their clients. Sadly, a few of them actually turn us down from time to time. Most of the ones who turn it down do so because there isn’t enough profit in it for them.

The most common statement we hear from these people is, “Why would I want to sell something that I would make up to 75% less on? Are you nuts? My clients will buy anything I sell them, and I would rather sell them a product that’s more profitable for me. I’ve got to take care of me and my family, not theirs.” Wow! Not exactly what you want to hear from an agent, right?

By the way, if you’re an insurance agent reading this book, and you don’t mind putting your clients’ needs first and earning a lower commission to be able to offer them the finest product they will ever see, give us a call. We license other agents and agencies all the time.

Our philosophy is and always has been 100% customer focused. We always put our customer’s needs FIRST, and then everything else works out. Just like my old friend Zig Ziglar used to say, “You can get everything in life you want, if you will just help enough other people get what they want.”

Besides, if we can give our clients a superior product, that’s a far better value than anyone else can offer, they’ll tell their friends and bring us referral customers, and that’s the way we want it.

Policies like IULs and Whole Life policies have a rating system called an IRR or Internal Rate of Return. When you look at the IRR, it’s like looking underneath the hood of that car you are considering purchasing. It shows you how the policy will perform, based on the assumptions you’ve made and the other variables such as age, amount invested, and years until withdrawal, estimated market returns, etc.

If you are considering purchasing a Whole Life policy, ask the agent to give you the IRR of the policy you’re considering. Sometimes it may be difficult to get them to show this to you. Do you know why? It’s because their IRR compared to their illustrated rate of return isn’t so hot. We will gladly give you this information because we know ours is superior and can’t be beat! We’re proud to show this and give it to you.

Our cost of insurance is the lowest you will find for programs like this. There are even ways we can structure your policy where your cost of insurance can completely stop. When that happens, one of your largest internal costs is removed, and your IRR goes through the roof. That’s why our program can’t be beat.

This program truly gives you the best of both worlds. You get very affordable permanent life insurance to take care of your family, and you also get tax-free income for retirement. This plan offers you the best combination of safety, flexibility, guarantees, control, liquidity, and tax advantages that’s ever been created. It helps you Protect, Grow and Leverage your retirement savings.

The specialized IUL product we offer outperforms the competition by drastically increasing the internal efficiency of the policy. By increasing the efficiency, it means you have a lower expense ratio, a higher account value, and significantly higher amounts you can take as income distributions.

That’s a very important question. Let’s break it down and look at it. There are basically two different types of insurance companies. Stock companies and Mutual companies.

Stock Companies: Stock companies are publicly traded. They must always have their “shareholders” best interest in mind more-so than their policy holders. They must focus on the short-terms demands of Wall Street, and their values are subject to the ups and downs of the stock market.

Mutual Companies: Mutual insurance companies are not publicly traded and do not have stocks or shareholders. They pay out their profits in the form of dividends to their policy holders. They always have their policy holder’s long-term best interest in mind. The payout of dividends is not guaranteed, however, of all the mutual insurance companies that we work with, not one of them has missed a single payment, EVER.

Most of these companies are over a hundred years old, and they are among the financially strongest companies in the world. Warren Buffet is even on record for saying that this business model of mutual insurance companies is one of the safest businesses in the world. In 2008 during the banking crisis studies indicate that 12% of banks failed and only .08% of life insurance companies failed.

The primary company we work with for our flagship IUL product is a mutual insurance company and has been in business since the 1880s (over 130 years). They have over 13 million policy holders. Their stellar record of financial strength and claims-paying ability positions them as one of the most highly rated companies in America. In fact, they have nearly $970 billion of life insurance in force. So the issuing company is as solid of a company that you would ever hope to work with.

In the book Money, Bank Credit and Economic Cycles, the author Jesus Huerta de Soto reported that, “In the last two hundred years, a negligible number of life insurance companies have disappeared due to financial difficulties.” In his book, he contrasts this to the high ‘financial death rate’ of banks, which can systematically suspend their payments and can fail without the support of the central banks.

We simply don’t think you can find a safer place on Planet Earth for your retirement funds!