Now we’re going to really get into the strategies that the ultra-rich have been using for centuries to massively grow their wealth. For the most part, these strategies have been largely unknown and unavailable to the average investor. Up until now, there’s simply been few easy and affordable vehicles available for the average person to participate in this type of thing unless you had an army of attorneys and the best financial minds on the planet devising and implementing these types of multiplication strategies.

Lucky for us, the Government has granted these amazing options as part of the specialized benefits of IUL policies. If you work with a skilled and specially trained advisor, and set up and fund your IUL policy correctly…

This is such a powerful program! When you fully understand how much of a difference it can make in your retirement program, you will lose some sleep thinking about it for sure.

Our clients are absolutely delighted with this option. It gives them diversification and outstanding peace of mind. They know their IUL retirement program has the potential to grow and grow with no market downside risk, while they invest those same funds into other areas.

Some clients are content to just stay with core part of the IUL program and not take advantage of the leveraging options the program offers. And that’s perfectly fine. It’s your choice.

Everyone has different needs and tolerances, and you should always do what you’re comfortable with. However, if you’re looking for a way to possibly put your retirement on steroids, you’re going to love Part 2.

Often when clients first come to us, they plug their numbers into our custom Barefoot Retirement calculator that we give you and discover that they’re not going to have near enough to retire the way they want to.

Their options are often limited to;

(a) Keep doing what they have been doing and make the decision to continue working during retirement.

(b) Decide to retire at a much lower standard of living than they had hoped to.

(c) Choose to utilize the power of leverage and put their retirement funds to work for them, on double duty, to potentially make up lost ground and still be able to reach their retirement goals.

We use a number of different names to describe the concept, but one of the main ones is:

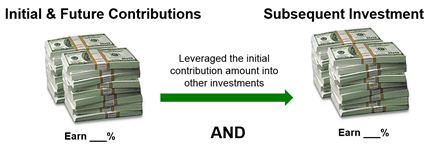

The Power of LEVERAGE is amazing! Now, you don’t have to settle for either/or if you don’t want to. This strategy gives you the power to employ 2 different investment options, with the same money, at the same time, and earn returns on BOTH of them. And before you ask, of course this is 100% legal, ethical, moral and doable.

First let me give you a simplified general idea of the strategy, then I’ll break it down into detail of how it works within our strategy.

Let’s just say you had $100,000, and you put it into our blended index fund. This concept allows you to keep the initial $100,000 working and earning for you, but allows you to borrow against it and invest the majority of those same funds into any type of investment you wish. Any type! And it gives you the potential to earn two different returns on the same money.

So if your investments perform well, you have the potential to earn two different returns on the SAME funds. Pretty amazing, right? Can you imagine how much faster your retirement funds could grow if you had them working for you in two different places at the same time?

To put this in perspective, let’s compare this to a regular IRA or 401k. Try calling up your broker and saying something like this, “He Bill. You know the 100k I invested in my IRA? I want to take most of it out and invest it in something else, but I want to keep earning the standard returns you get for me on the 100k in my IRA. That’s okay, right? I mean, you can do that for me, right?” Just try that and see what happens.

First off, it’s important to know that a life insurance policy is by definition tax-deferred, it’s not tax-free. The cash value of an IUL policy grows without being taxed. However, IF the money is “withdrawn,” then all the gains within the policy (the amount earned in addition to the total premiums paid) will be taxed as income and not as capital gains. Rest assured that our strategy does not involve ‘withdrawing’ your funds nor having to pay taxes on them.

Our method gives you Tax-Free Access to your funds. The key is doing it correctly, and that’s why it is so important to work with people who are specifically skilled on these exact types of policies like our team is.

Our clients use a contractual policy feature that allows a policy holder to have access to tax-free money in their policy by using their life insurance cash value as collateral. It’s called a Policy Loan Provision and is one of the most valuable and amazing aspects of this program. When executed correctly, the policy owner is able to avoid any and ALL taxes on the funds they receive. The distinction here is that it is simply a loan from a financial institution and NOT a withdrawal from an insurance policy.

(Note, a policy holder is able to take a tax-free withdrawal from their policy only up to the amount of total premiums paid into the policy to date, subject to surrender charges, because those funds were taxed before they went into the policy. If you choose to withdraw funds above the total premiums paid, the withdrawal of the gain is taxed as income. When using our strategy correctly, you will not be withdrawing funds.)

When you use the policy loan provision correctly, as we advise you, you take out a loan AGAINST the cash value in the policy. You are not taking out a loan FROM the cash value and there is a huge difference here. The cash value within the policy is the collateral for the loan.

Remember when you borrowed money to buy your last car? Was the loan that you got from the bank taxed? No. Loans are not taxed. Yes, you probably paid tax on the car when you bought it but the loan itself was not taxed. The distinction here is that loans are not taxed. When you buy goods and services, they are taxed, but not loans.

Also, when you borrow money in the form of a loan, you have to pay interest on the loan, right? Correct. That’s true. When setting up your IUL and structuring policy loans, there are quite a few different options available and your advisor will give you great advice in this area. At the time this book is being written, the average amount charged for policy loans by the issuing insurance company is around 4.5%.

As you may have guessed by now, there are lots of different options here.

Option 1: You NEVER have to pay it back during your lifetime. That’s right? If you don’t pay the interest back the insurance company will simply deduct it from your death benefit amount. They policy should still be monitored carefully each year to ensure the ratios are fine, but as long as you do this correctly, you can take out a lone against your policy and never, ever have to pay it back if you don’t wish to. I’ll show you an example of how this works in just a moment.

Option 2: You can pay back as much as you wish, when you wish. You have total flexibility here. You get to choose if you want to pay back the interest charges and if so, how much you want to pay back and when you want to pay them back. (Don’t you wish your bank was this easy to work with?)

Option 3: Wash Loan Provision. One of your options is to choose a fixed indexed return on the cash value of your account. Currently, the fixed return is around 3.5%. These amounts do vary from time to time but generally speaking, if it cost you 4.5% to borrow the funds, and if you can choose to receive a 3.5% fixed return, then the net cost of your loan is only about 1%. Plus, with our flagship product, after 10 years the company drops the wash loan amount down to .1%.

While most people borrow the funds against their policies from the insurance company itself, you always have to option to go to any outside institution and borrow the funds from them. Some of our clients are doing this right now and are borrowing from banks at rates around 2% to 3%. Why you may ask would a bank give a borrower such a low rate? It’s because the loan is collateralized by the cash value of the life insurance policy, and that’s one of the most secure forms of collateral a lender can have. Note, getting a lone from a bank is not guaranteed and may require work than just calling the insurance company.

Most similar policies and most Whole Life policies require that you wait many years before you can begin to borrow funds from your policy.

However, some of our clients choose to purchase a rider on their policy that enables them to borrow up to approximately 80% of the cash value of their policy beginning in the very first month that your policy is taken out. This can be a huge benefit. (Note: There are lots of options when setting up these policies so the percentage amount that can be borrowed can vary depending on many variables.)

The great news is that since the funds are distributed as a loan, they DO NOT show up in any tax reporting, and they will NOT be shown on your tax returns.

Hence, it's PRIVATE!

For most of the people I know and talk with, privacy is a huge issue these days. The more they can stay off the grid, the better!

It’s important to note that you shouldn’t take too much money out of your policy to the point that the policy becomes non self-sustaining. Again, this is where your advisor and help keep your policy safeguarded and functioning correctly. It’s not hard to do at all, but you should just be aware of it and monitor it from time to time.

Some people initially have a hard time wrapping their mind around this concept. It just doesn’t seem plausible that you can borrow the money from your policy, not pay a single penny back, and still have your policy give you a great lifetime, tax-free income… Plus have the money you borrowed out of it to boot. Right? Well, I totally understand that. I’ll prove it to you right now with an actual IUL illustration.

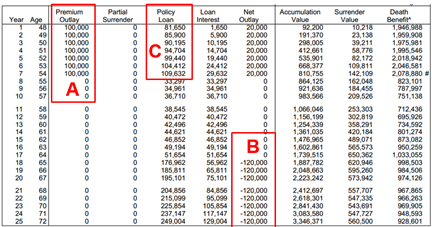

In this illustration below we took a 48-year-old man whom we will call Don and structured the policy where he would invest $100,000 per year, each year, for 7 years. After the 7th year, Don would NEVER have to put another penny into the policy, ever.

(If you happen not to be a high-income earner or don’t have a larger amount to invest, please don’t let the $100,000 example scare you. It’s an easy round number to demonstrate this with. If you only have several hundred dollars a month to put into a policy, you can still participate and still get ALL of the awesome benefits of this program.)

Without getting into all of the details of the illustration below, let’s just focus on a few main points.

A. In the red box area where you see the A, that shows where the policy holder invests $100,000 per year for 7 years. That was his premium outlay amount.

B. In the red box area where you see the B, that shows where the policy holder borrowed $80,000 a year from his policy, each year, for 7 years. Over 7 years Don borrows $560,000 from the policy. (More detail on this in a moment. We can also structure policies where you can borrow over 90% however, we wanted to keep this example somewhat conservative.)

C. In the red box area where you see the C, that shows where the policy holder, at age 65 starts borrowing $120,000 of tax-free money, each and every year, until he dies or until he reaches 120 years old.

Here the policy holder borrows $80,000 a year for each of the 7 years. He can choose to borrow nothing, or chose to borrow any amount he wishes per year, up to the $80,000 amount shown in this illustration. He can take that $80,000 a year and invest it in ANYTHING he wants to. He does not have to ask anyone for permission, and he does not have to abide by any guidelines that dictate where he can put the money.

This is your retirement fund so it is serious business, and you should only invest these funds into solid and safe investments that you believe will serve you the best. But just to be crystal clear and to make a point, if you want to borrow those funds and take a vacation around the world, you could. You could choose to spend it all on a new home or boat, plane, on medical costs, give it to charity, or buy anything your heart desires. The point is, YOU get to choose. Neither the Government nor any other entity is there to tell you what you can and cannot do with your money.

Hopefully, the policy holder will choose wisely and make wise investments that will help fund the retirement of his dreams. If he makes some wise investment decisions, he could turn that $560,000 into millions, by the time he retires.

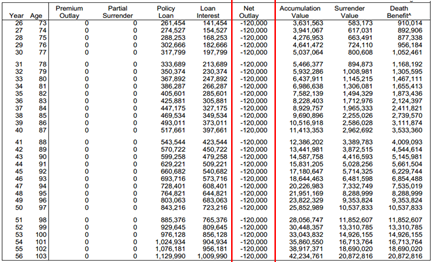

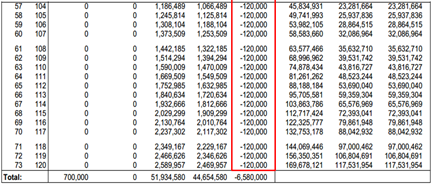

Here is the great part. It doesn’t matter if he makes millions with the funds borrowed, or if he lost it all on a wild weekend in Las Vegas. As long as the policy continues to perform as illustrated above, when he turns age 65, he will get to take $120,000 of tax-free income out per year, each and every year, until he either dies or reaches age 120. How powerful is that? Imagine the peace-of-mind you could have with a safety-net like this?

By the way, if the policy holder happened to be in a 38% tax bracket when he started taking out the funds, the $120,000 tax-free dollars a year would be approximately the equivalent of $210,000 taxable dollars.

Lastly, the illustration above shows how the policy performs if he chooses to never pay back a single penny of the funds he borrowed. If he did choose to pay back some or all of the borrowed funds, the more he pays back, the larger the Net Outlay is or the amount of tax-free dollars that he gets to take out during retirement, each and every year until he dies or reaches 120 years old.

In the example above, if Don paid back the loans he borrowed each year, his net outlay would increase to approximately $240,000 per year until he reaches 120 years old.

That’s always a great question that comes up. The reason it comes up so frequently is because most people are so “conditioned” by the rules, regulations and restrictions of qualified retirement plans like IRAs, 401(k), etc., they are just accustomed to having strict limitation’s dictating what you can invest in and what you can’t invest in.

This is totally different.

With a properly structured IUL, you can invest in ANYTHING you want. Anything! There are no limitations what-so-ever. You can keep your IUL locked up, in the blended index account, earning 0% to 17% a year, with zero chance of losing a penny due to market downturns, and then take out a lone against your policy and invest it in anything you wish.

• Businesses, business equipment, sustaining and growing your business, business loans, etc.

• Real Estate of any type, notes and mortgages

• Precious Metals of any type (gold, silver, platinum, palladium, etc.)

• Oil & Gas

• Stocks, Bonds, Mutual Funds, ETFs, etc.

• Art & Collectibles of any type

• Cars, boats, airplanes, etc. (It’s usually better to choose assets that are likely to increase in value.)

With this program, you can invest in anything that makes sense to you, that you believe you can make a positive return on, and that you believe is wise and safe.