A real economy is vastly more complex than our simple economy and its money is also more complex. Perhaps the biggest difference is that in the simple economy (with jewellery as money) money was itself wealth - created by labour - and the money supply could be expanded or contracted at will simply by producing more or less of it. That was a great strength. The money supply could respond quickly and easily to any shortage or oversupply, so the quantity in circulation remained close to the level that the economy required. Money in a real economy is very different in that it is not wealth and not a product of labour, so there is nothing that ordinary people can do to bring more into circulation except by borrowing from banks, and that incurs heavy penalties in the form of interest payments - more on that in Part 2. Nevertheless in spite of major differences there are similarities. Saving money has a similar effect and is discussed in the following two chapters. The required quantity and rate of spend of money are also similar, in that they should be sufficient to allow all transactions to take place that people want and have the means for - meaning that sellers have goods or services to sell, and buyers have saleable assets (including their own future labour) equal to or in excess of the transaction value - we'll refer to these as legitimate transactions. Indeed this is precisely what money is for, to enable people to exchange different forms of wealth with each other.

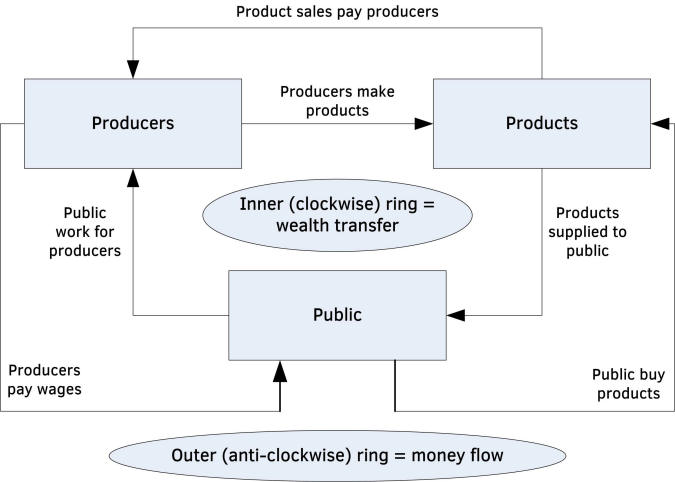

A simple diagram illustrates the flow of money and transfer of wealth when the economy is working properly.

Figure 14.1: Wealth transfer and money circulation

Although it is the same money that circulates continually around the economy, it is new wealth that is created in each transaction. Money circulates but isn't consumed, whereas wealth is consumed or utilised but doesn't circulate. For wealth to be created, traded, consumed and utilised money MUST circulate.

A simple story illustrates this important effect. A person loses a £10 note in a pub one night. When clearing up the landlord finds it and pockets it. Next morning he spends it on a haircut and the barber then uses it to buy his lunch from the lady who owns the local cafe. The cafe owner gives the note to the window cleaner in return for his services, and in the evening the window cleaner buys a round of drinks with it in the pub. Later that night the person who lost the note returns and asks the landlord if anyone found it. The landlord, being honest, says that he found it, and returns it to its original owner. The £10 note is now back where it started from, having circulated around the local economy and made possible the creation of £40 worth of wealth in the form of a haircut, a lunch, window cleaning and a round of drinks. It is the same money that changes hands in each transaction, but it is new wealth that is created and consumed. Money's role as a lubricant is clearly seen in this story - it is the same money that enables every transaction just as it is the same oil that lubricates the moving parts in every engine revolution.

If we remove the money from the story we can see what each person gets and gives. The landlord gives a round of drinks and gets a haircut; the barber gives a haircut and gets a lunch; the cafe owner gives a lunch and gets her windows cleaned; and the window cleaner cleans windows and gets a round of drinks. The notable feature is that what everyone gets is from a different person than the person they gave something to, which is exactly how the real economy works. It is money that allows multi-person exchanges, which is quite marvellous when you stop to think about it. We are so used to it that we take it for granted, but without money it would be impossible to keep track of who owed what to whom, and therefore very many fewer transactions would be possible.

What is really happening is that we are all working for each other, both in this story and in the real economy, and money is the lubricant that makes it possible.

The above story illustrates another important point. For the economy to benefit new wealth must be created and become available for use. Money for new wealth is payment for the time, effort and expense involved in creating it. When existing wealth is bought (wealth that has already been bought by someone else when it was new) it doesn't affect the economy because the economy has just as much wealth after the exchange as before it. All that happens is that money and existing wealth change owners.

All wealth in the story is new wealth. When existing products are exchanged the only new wealth, if any, is the service of making the products available to buy, not the products themselves. Therefore a good second-hand car dealer provides the service of bringing a range of cars together, cleaning, repairing and servicing them, having them tested and provided with roadworthiness certificates, providing warranties and advertising them for sale. This service represents the new wealth that is created, which is exchanged for an income when buyers buy the cars. The dealer's profit is the excess of income over the cost of the cars together with all other associated expenses and that profit represents payment for the service that the dealer provides. In this case the service (new wealth) provided by the dealer for a particular car is consumed as soon as the car is bought, as are many services, but it nevertheless added to total wealth prior to its consumption - as indeed does all wealth. The cars themselves don't represent new wealth because when they were new they were sold to someone else, who merely transferred them to the dealer in exchange for money.

It is important to separate spending on new wealth creation from spending on existing wealth transfer. Only the first adds to total wealth and therefore benefits the economy. The second adds no new wealth so it does nothing for the economy though it does benefit the parties directly involved.

If I sell my car to a friend then no new wealth is created, all that happens is that the car (existing wealth) and money change hands. The economy isn't affected by this exchange. This also applies if the car I sell to my friend has serious faults that I keep quiet about and charge twice the price it is really worth. I have made a profit by deception but that profit isn't income in exchange for new wealth because my friend, who is now my ex-friend, hasn't received anything in exchange for it except perhaps the satisfaction of giving me a black eye! In effect the profit represents a money transfer (extraction) by exploitation. In this case my deception becomes clear soon enough, but in many transactions deception or information hiding is much more subtle, especially in banking and financial trading as will be explained later, and as a result the bulk of what is thought to be new wealth represented by the services that those sectors provide is really extraction of existing wealth from others by exploitation. This is considered in detail in Part 2.

Making a profit from another's ignorance is not wealth creation; it is wealth extraction by exploitation.

Recall that wealth extraction is charging more for a product or service than a fully informed and unexploited buyer would be willing to pay.

When money is taken out of the picture and wealth alone is considered it is clear that the economy is a giant human-powered wealth creating and using machine, where people work continuously to produce the products that people need and want, and people continuously use them. Provided that the machine keeps on producing and using then all is well. To keep the machine working we need a means of persuading people to create wealth and to part with it to others without immediately receiving an equivalent quantity of wealth in return (that would be barter and as already discussed barter is very difficult and usually impractical). Hence what is needed is trust, the giver of wealth needs to trust that he or she will receive back the value of that wealth in due course, and that's what money provides. As long as people believe that money will retain its value then to an individual or business money is just as good as wealth and people have no difficulty in exchanging wealth for money. All that is needed therefore is for there to be sufficient trust, embodied in money, to allow all legitimate transactions to take place. It sounds simple - and it could be - but it isn't.

Sadly controlling the money supply in a real economy, given the way the system works, is very difficult indeed. This is why inflation and deflation strike such fear into all participants in the economy, especially governments, which can stand or fall on the behaviour of the money supply, as indeed can businesses, families and individuals.

This is a very peculiar situation. We have a system that has been invented and designed by humans - there is nothing natural about money - and yet it behaves as though it was a natural phenomenon like the weather, beyond human control. Governments try to exercise a measure of control in the form of fiscal policy - taxing, borrowing and spending; and central banks try to exercise a measure of control in the form of monetary policy - setting the bank rate (the interest rate charged to commercial banks for BoE reserves - see chapters 39 and 41) and buying and selling securities such as government bonds and sometimes other assets in the market. However these merely provide fine-tuning and are only successful in the absence of major economic turbulence brought on by external shocks (natural disasters, raw material shortages, pandemics etc.) and internal events (asset bubbles bursting, excessive lending and borrowing, major debt defaults, currency attacks by speculators etc.). In these circumstances the levers available to government and central banks prove hopelessly inadequate, and the economy and everyone in it are tossed about like small boats on a stormy sea. The means by which governments and central banks try to control the money supply, why they are inadequate, and how it could be made so much better are examined in chapters 86 and 100.