It will be useful to consider all the main transactions that a bank (i.e. a retail bank) undertakes, to see when and how money is created and destroyed. It will be useful also to explore the main transactions of government in the same way, because government transactions usually involve banks, and the insights gained can be used in Part 4 to examine how the government currently raises money and to consider how it might raise money more beneficially.

The major point to bear in mind is:

New bank money comes into existence whenever a bank makes a payment in bank money (increase in customer liabilities) and goes out of existence whenever a bank receives payment in bank money (decrease in customer liabilities).

Given the above basic principle we can set out the various transactions that banks undertake:

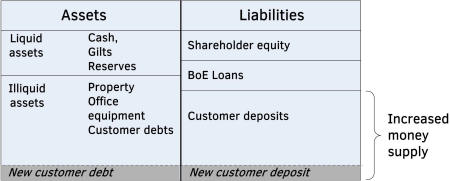

i. Bank loan to a borrower with an account at the lending bank (figure 44.1): a loan agreement signed by the borrower is received by the bank's loan account (account debited), creating an asset for the bank. At the same time bank money is made available to the customer and recorded as a bank debt in the customer's deposit account (account credited), creating a liability for the bank. It might appear that since bank money has been received by the customer the deposit account should be debited, but remember that it is the customer who has received the money and the customer is external to the bank. In order for the customer to receive the money the bank must take it from somewhere, and that somewhere is the customer's deposit account, so the account is credited.

Figure 44.1: Balance sheet expands, new asset balances new liability.

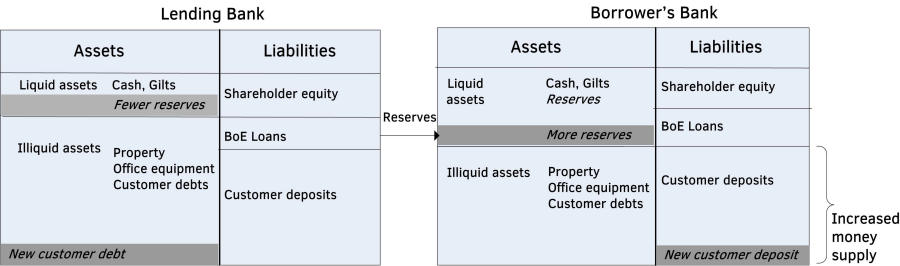

ii. Bank loan to a borrower with an account at another bank (figure 44.2): the lending bank sends BoE reserves to the borrower's bank (lending bank reserve account credited so an asset is destroyed), and the loan agreement signed by the borrower is received by the lending bank' loan account, which is debited (an equivalent bank asset is created). When the borrower's bank receives the reserves its reserve account is debited (an asset is created), and a new debt to the borrower recorded as a credit in the borrower's deposit account (an equivalent bank liability is created). The net effect is exactly the same as in case (i): bank money (a liability) has been created and an equivalent asset in the form of the loan agreement has also been created. The borrower's bank merely acts as an intermediary in the process, receiving reserves in return for crediting the borrower's account.

In this case the lending bank doesn't create money; it 'buys' the new customer debt with state money - BoE reserves. But, importantly, that state money isn't given to the customer who takes on the debt; it is passed to another bank to compensate it for creating money and thereby taking on a new liability to the customer. Bank money has still been created, but not by the lending bank. In reality all banks lend money all the time, so for almost every loan that bank A gives and sends reserves to bank B, bank B also gives a similar loan and sends reserves to bank A, so the net effect is very many loans and very little reserve transfer.

Figure 44.2: No change in lending bank balance sheet; it gains one asset (customer debt) and loses another (reserves). Borrower's bank balance sheet expands; it gains an asset (reserves) and a new balancing liability (customer deposit).

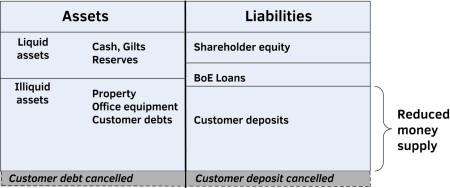

iii. A borrower with an account at the lending bank repays a loan (figure 44.3): the customer pays the bank which passes that value to the customer's deposit account (account debited - bank money representing a bank liability is destroyed), the original loan agreement is stamped as paid (in effect sold back to the borrower in return for the repayment) and the bank's loan account is credited (an equivalent asset is destroyed).

Figure 44.3: Balance sheet shrinks, an asset loss balances a liability loss.

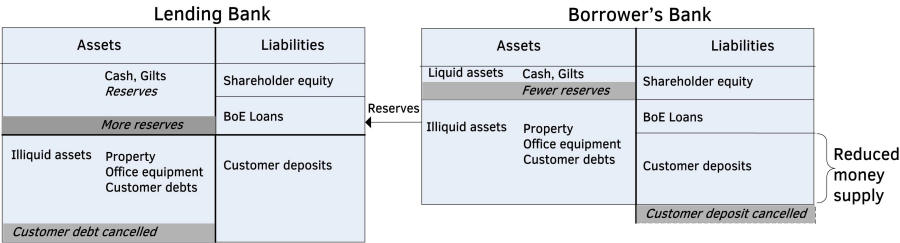

iv. A borrower with an account at a bank other than the lending bank repays a loan (figure 44.4): the borrower transfers money from their bank account to the lending bank, which receives reserves from the borrower's bank and debits its reserve account accordingly (an asset is created). The original loan agreement is stamped as paid and the bank's loan account is credited (an equivalent asset is destroyed). The borrower's bank credits its reserve account (an asset is destroyed) and debits the borrowers account (an equivalent liability is destroyed). The net effect is exactly the same as in case (iii): bank money (a liability) has been destroyed and an equivalent asset in the form of the loan agreement has also been destroyed. The borrower's bank merely acts as an intermediary in the process, sending reserves in return for debiting the borrower's account.

Figure 44.4: No change in lending bank's balance sheet, it gains one asset (reserves) and loses another (customer debt). Borrower's balance sheet shrinks; it loses an asset (reserves) and loses a liability (customer deposit).

For simplicity the remainder of these examples will just involve a single bank, other banks may be involved in reality but as above they only act as intermediaries. Also the effects on assets and liabilities and the money supply will just be stated rather than illustrated.

v. A borrower pays interest on a loan: bank money is received by the bank (debited from the borrower's account - a liability is destroyed), and the bank gives its shareholders the equivalent value (the shareholders' account is credited - an equivalent liability is created). Recall that the shareholder equity account is a liability of the bank because it 'owes' this amount to the shareholders.

vi. A bank pays an employee's salary: bank money is made available to the employee and the bank debt recorded in the employee's deposit account (account credited - liability created), and value is received (debited) from the shareholders' equity account (an equivalent liability is destroyed). In effect the shareholders have taken on the debt represented by the employee's salary by reducing their holdings in the bank.

vii. A bank buys office equipment: bank money is made available to the supplier and the bank debt recorded in the supplier's deposit account (account credited - liability created), and the bank's asset account is debited (office equipment received - an equivalent asset is created).

viii. A bank pays a dividend to its shareholders: bank money is made available to the shareholders and the bank debt recorded in the shareholders' deposit accounts (accounts credited - liabilities created), and value is received by the bank from the shareholders (their equity account is debited - an equivalent liability is destroyed). In effect the shareholders have been given value in the form of bank money and in return reduce their holdings in the bank.

For vi, vii, and viii recall what was said in chapter 39: bank money created for a bank's own purchases (salaries, bonuses, dividends, goods and services) is taken from debt interest payments that were destroyed when received, so there is no net creation of new money for these purchases.

ix. A customer withdraws cash from an ATM: bank money is received by the bank (debited from the customer's account - a liability is destroyed), and cash is given to the customer (credited to its cash account - an equivalent asset is destroyed). Note that a bank can only obtain cash from the BoE by paying reserves for it; it can't create and use bank money for the purpose because the BoE doesn't accept bank money. Similarly if a bank pays cash to the BoE then it receives reserves in exchange. Note that in this case the bank discharges it's liability to the customer by paying out state money.

x. A customer pays cash into a bank account: bank money is made available to the customer and the bank debt recorded in the customer's deposit account (account credited - liability created), and cash is received by the bank's cash account (account debited - an equivalent asset is created).

xi. A customer repays a bank loan with cash: this is an interesting case in that no bank money is involved; one bank asset (the customer debt) is exchanged for a new asset (the cash). The bank money that was created when the loan was originally taken out was destroyed when the cash was handed over from a bank to a customer, regardless of who got it and how it found its way to the borrower to repay the bank.

xii. A borrower defaults on a loan repayment: this is another interesting case in that again no bank money is involved. The bank money created in response to the original loan remains in the banking system, but not in the borrower's account because he or she can't pay. The asset in the form of the loan agreement that the bank thought had value is now seen to have none, so on the balance sheet the loan account is credited (an asset is destroyed), and to balance it the shareholder equity account is debited (an equivalent liability is also destroyed). In effect the debt is transferred from the original borrower to the shareholders and the bank itself has lost that amount of value.

The remaining transactions involve government borrowing by selling and repaying bonds (gilts) to banks and others. They are quite complex but are included to show the mechanisms involved, and to show that to banks gilts are just the same as any other debt that they own, in that when banks buy gilts they do so with created bank money - not as individual banks but in conjunction with other banks. This will be taken up in chapter 89 on government borrowing.

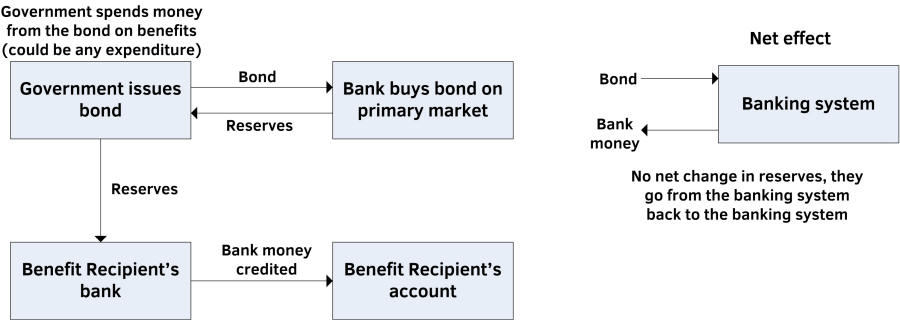

xiii. A bank buys a government bond directly from the government (i.e. on the primary market): government bond purchase is very important for banks because they can be used as collateral for loans of reserves, so if the bank can create money to buy them then it is in effect able to create the means to obtain reserves at no cost. However, since one organisation with a reserve account (the bank) is dealing with another organisation with a reserve account (the government), no bank money is involved. The bank merely transfers reserves to the government in return for the bond (its reserve account is credited (an asset is destroyed) and its bond account is debited (an equivalent asset is created). It seems therefore that a bank can't create money to buy a bond. However, if we pursue the matter further we see that the government wants the money in order to spend it in the economy, on public servant salaries, benefits, the NHS, subsidies and many other things. When it spends this money bank money is created - reserves are transferred from government to the recipient's bank (increase in bank assets), and the bank credits the recipient's account with new bank money (increase in bank liabilities). Hence the banking system as a whole can create money to buy bonds, though the original bank that bought the bond won't necessarily be the bank that creates the money. What has happened, after the money from the bond has been spent by the government, is that the banking system has created the money to buy the bond, and thereafter enjoys the interest that is paid on the bond from the taxpayer - for nothing in return - nice! Also, perhaps even more importantly, it has increased its stock of high quality assets, and thereby improved its position with respect to the capital and liquidity ratios that banks are bound by, and as a result it can lend more and further increase profits. Although this process involves the banking system as a whole, all the players are involved so they all share the benefits. This is shown in figure 44.5.

Figure 44.5: How the banking system creates the money to buy government bonds on the primary market.

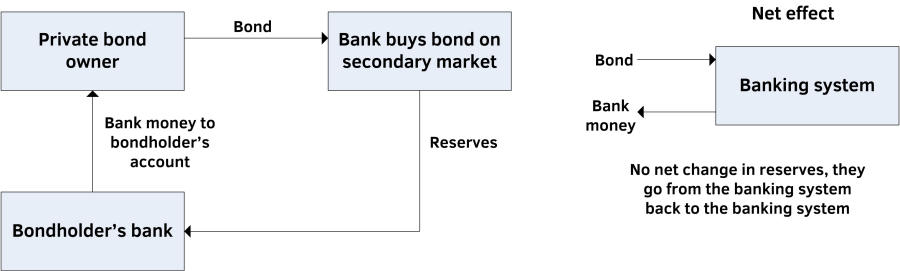

xiv. A bank buys a bond on the secondary market (i.e. from someone other than the government): here the bank creates the money directly by crediting the account of the seller (a liability is created), and debits its bond account (an equivalent asset is created). The bond seller might well bank with a different bank than the bank that buys the bond, as shown in figure 44.6, in which case reserves are transferred to the seller's bank which then creates the money to credit the seller's account. In either case money has been created by the banking system, although the bond buying bank might well not be the bank that creates it.

Figure 44.6: How the banking system creates the money to buy government bonds on the secondary market.

However the banking system obtains government bonds, either on the primary or secondary market, it has created the money to buy them. As a result it gets interest from the taxpayer on a zero risk asset, the taxpayer gets nothing in return, and at the same time the banking system is able to increase its lending.

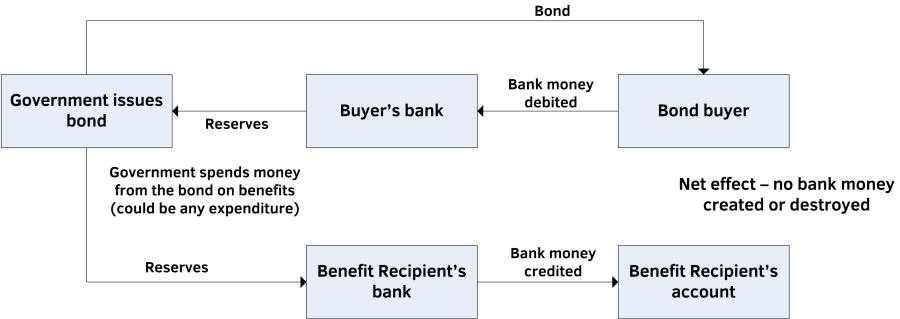

xv. A non-bank company buys a bond on the primary market: the company pays money to the government and its bank transfers the corresponding reserves. Bank money is destroyed in this process, but is recreated when the government spends the money raised in the economy. Hence there is no net effect on the money supply in this process. The same applies if a non-bank company (or individual) buys a bond on the secondary market. Here bank money merely changes hands and the bond also changes hands. See figure 44.7.

Figure 44.7: If a non-bank company buys a bond on the primary market then there is no effect on the money supply. The same applies if it is bought on the secondary market.

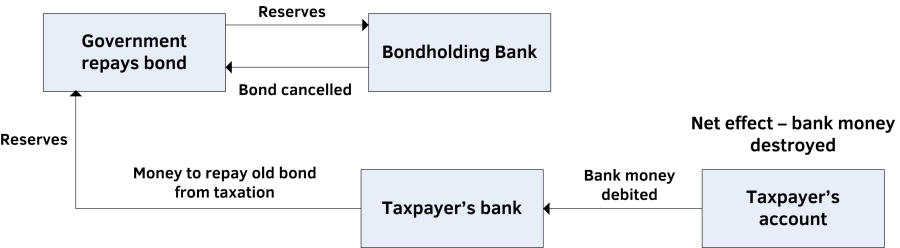

xvi. The government repays a bond owned by a bank on maturity: the government transfers reserves to the bank and the bond is cancelled. The bank's reserve account is debited (an asset is created) and its bond account credited (an equivalent asset is destroyed). Hence no bank money is involved directly, but in order to repay the bond the government has to raise the money, either by issuing a new equivalent value bond or by taxation. Figure 44.8 shows the effect if the money is raised from taxation. Here bank money is destroyed because bank money is debited from the taxpayers' account, but isn't credited anywhere else. If the money to repay the bond is raised by issuing a new bond, then the overall effect depends on whether it is bought by a bank or a non-bank. If bought by a bank then there is no net change (no bank money is involved, reserves are transferred from the new bond-buying bank to the government which transfers them to the bank holding the maturing bond), and if bought by a non-bank then money is destroyed in the same way as it is if taken from taxation.

Figure 44.8: Government repays a bond held by a bank from taxation - bank money is destroyed.

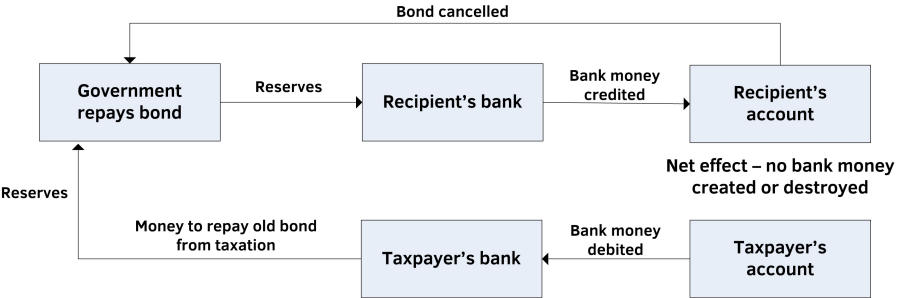

xvii. The government repays a bond owned by someone other than a bank on maturity: the government cancels the bond and transfers reserves to the bank of the bond owner which debits its reserve account (an asset is created), and the bond owner's bank creates bank money by crediting the bond owner's account (an equivalent liability is created). Hence bank money has been created. However, again the government must raise the money to repay the bond as above. Figure 44.9 shows the effect if the money is raised from taxation. Here bank money is destroyed as before so there is no net effect - bank money is created for the maturing bond holder and destroyed for the taxpayer. If the money to repay the bond is raised by issuing a new bond, then the same applies as discussed above - the overall effect being to create money if it is bought by a bank but no effect if bought by a non-bank.

Figure 44.9: Government repays a bond held by a non-bank from taxation. No bank money is created or destroyed.

Isn't it strange that the state refuses to create money for itself, preferring instead to borrow money created out of thin air by private companies, when taxpayers have to pay heavily for this 'service'? See also chapter 89.

Although the mechanisms of bond sale and repayment when banks are and are not involved are complex, the overall outcome is simple and exactly the same as when a bank buys or sells any other type of debt other than when dealing with another bank - banks don't create bank money for each other. The point made earlier about new bank money coming into existence whenever a bank makes a payment in bank money and going out of existence whenever a bank receives payment in bank money can now be restated in terms of debts:

When a bank buys a debt from anyone other than another bank, bank money is created and lasts as long as the debt lasts. When a bank sells such a debt then bank money is destroyed. If any other person or organisation buys or sells a debt then there is no net effect on bank money.

A bank buying a debt includes accepting a signed mortgage or other form of loan agreement as well as buying a government bond, and selling a debt includes a mortgage or other debt being paid off (in effect the bank sells the original agreement back to the borrower in return for the repayment), and in the case of a government bond the bank sells the maturing bond back to the government in return for reserves.