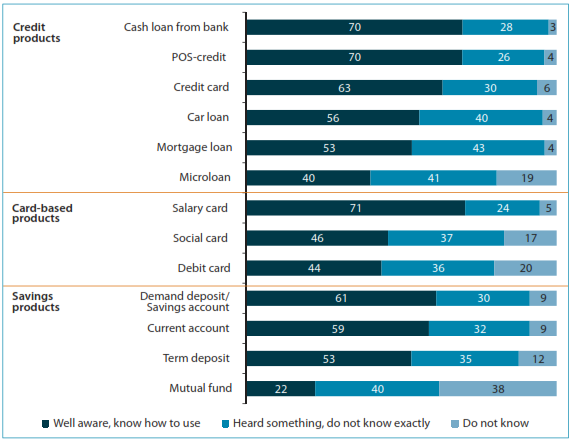

One of the objectives of this research was to establish how awareness levels about financial products correlate with usage levels. Figure 9 presents an overview of awareness levels with respect to credit, card-based, and savings products.

Figure 9. Awareness about credit, card-based and savings products

Note: Distribution of answers to the question “Which of the financial products (services) do you know?” (percentage of total respondents, n = 2800).

Overall, the levels of awareness are much higher than those of usage in absolute percentages. With a few exceptions discussed below, a vast majority of respondents believe they are either well aware and know how to use the products, or at least they have heard something about most of the products. This indicates that low usage levels are not due to the fact that people do not know about the existence of certain products, but there are other factors affecting their decision not to use them. In particular, the research revealed that many people thought they know and understand some product, but actually they confused it with a similar one. This and other factors preventing people from making the most use of financial services is discussed in more detail in Chapter 3.

Respondents showed the lowest awareness levels about mutual funds and microloans. This can be explained by the relatively short history of these products in Russia: the first mutual funds were established in Russia about 15 years ago, and the first official microfinance institutions

(MFIs) started providing services in January 2011 (see Chapter 1).

As is the case with usage, there are regional differences in awareness levels — generally corresponding with usage patterns, but with a few exceptions:

Other sociodemographic characteristics that influence awareness levels about credit, card-based, and savings products include the following:

Detailed breakdowns of the survey results on the awareness about credit, card-based, and savings products are presented in Annex 3.

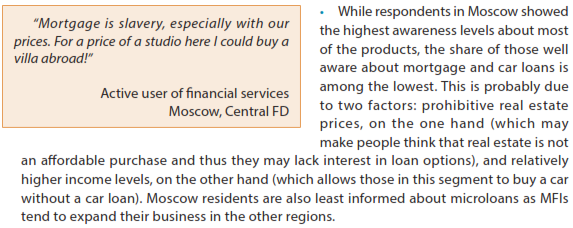

Insurance products

The overall level of awareness about insurance products is generally lower than that about credit, card-based, and savings products: the awareness about the most popular products does not exceed 58 percent (Figure 10). As discussed, Russians are most aware of those products that are either required by law (e.g., mandatory MTPL insurance) or provided to them by a third party (e.g., employer-issued voluntary health insurance). The latter is best known to residents of large cities where large corporate employers operate.

Figure 10. Awareness about insurance products

Note: Distribution of answers to the question “What insurance products do you know?” (percentage of total respondents, n = 2800).

The products people are the least aware of include Green Card insurance and insurance for traveling abroad: both are issued only to those who travel abroad by car or to certain countries (e.g., Schengen), respectively, and it seems not many Russians do so (e.g., according to a recent national poll only 6 percent of Russians plan to travel abroad in 2014).36

This part of the research revealed the highest degree of confusion with various insurance products among respondents: for example, many of them were not sure about the differences among health insurance products (and the public medical care program as discussed above), or among mandatory and voluntary products (e.g., mandatory and voluntary MTPL insurance and motor hull insurance).

In contrast with credit, card-based, and savings products, there are no significant regional variations in awareness levels with respect to insurance products. Awareness about car insurance is slightly higher in Southern FD, which corresponds with the higher usage rates of these products in this region. In North Caucasian FD, certain types of personal insurance (such as disability and risk life insurance) are better known to respondents due to higher personal security risks as a result of military conflicts in this area in the late 1990s and early 2000s; however, this does not translate into higher usage rates for these products.

The factors influencing awareness levels about insurance products include the following:

Detailed breakdowns of the survey results on the awareness about insurance products are presented in Annex 3.

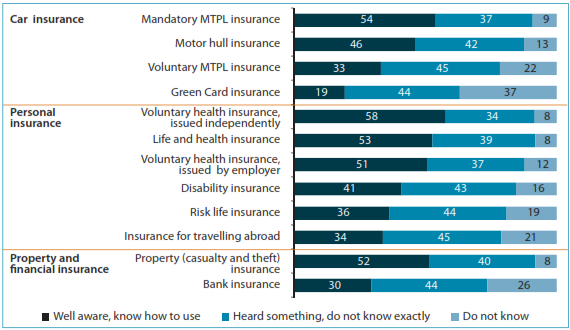

Delivery channels

As could be expected based on usage patterns, Russians are the most familiar with traditional channels (81–91 percent of respondents are well informed), and the least familiar with innovative channels (33–43 percent believe they are well informed). Lower awareness and usage levels of innovative delivery channels may have to do, inter alia, with high prevalence of cash transactions: only 16 percent of Russians regularly use noncash transactions, and 50 percent use cash transactions exclusively (Central Bank of the Russian Federation 2014). Figure 11 provides a summary of the awareness levels on the various channels.

Figure 11. Awareness about delivery channels

Note: Distribution of answers to the question “What financial service delivery channels do you know?” (percentage of total respondents, n = 2800).

There are no significant variations in awareness levels in terms of regions or types of settlement, though Moscow, as is the case with most financial products, again shows the highest average awareness levels about all channels (54 percent versus 42 percent Russia-wide). Among a few notable exceptions are the following:

The factors influencing awareness levels about delivery channels include the following:

Detailed breakdowns of the survey results on awareness about financial service delivery channels are presented in Annex 3.