There is no question that a person’s personal credit profile is of utmost concern to a mortgage lender. And yet, there is a basic idiocy to this. If I am borrowing the money in order to buy a house, that property is a tangible asset with a specific value. The house itself is the collateral. What I earn as a plumber or as a secretary is irrelevant. Whether I had a rough patch two years ago where I had trouble paying my bills on time should also be irrelevant. In a perfect world, if I am borrowing money to buy a house, the lender should be comfortable in knowing that if I squander the money and fail to make my payments, they can always take the house.

But this is not a perfect world.

Yet when we purchase investment property rather than a home to live in, the world becomes just a little more perfect. When you go in to plead your investment property case to a mortgage lender, you will be going in with a “business plan,” not simply your personal credit score. If the numbers work on your “business plan,” you will most likely get approved for a mortgage loan—even with less than perfect credit. This is far less true if you plan on living in the place yourself. In a sense, then, the income a property can produce exceeds the value a lender will even place on YOU.

But let’s get back to the bold statement in the bold type at the beginning of this chapter. In investment property, the kind of rent the property can produce is the magic number. If you buy a $500,000 property that you can only rent for $250 below its monthly overhead (mortgage, taxes, insurance, upkeep, etc.), that property has no positive value to you or to your lender. Even if one may speculate that the property in question may (because everything in speculation is uncertain) increase, or in the very least hold value, you are still losing $250 per month, every month. On the other hand, a $115,000 property that rents for $250 above its monthly overhead is a gem! Crazy, huh? But bear with me; this program will turn a lot of your long-held perceptions upside down.

The reason lenders look at all of this differently is that if you disappeared tomorrow instead of trying to sell your income property at a foreclosure sale—which they hate to do because they inevitably end up selling it at a loss—they can hold on to that property and manage it to a profit just as you had done, or else sell it to an investor, using the same “business plan” to seal the deal. Thus, the idea here is simple—find properties that can be rented for a profit. Nothing else matters at all.

These facts have never been disputed by anyone when the subject is purely commercial property, such as an office building or a storefront. But the average person finds it surprising when I tell them it holds true for residential income properties as well. The reason for this is emotion. Homes are an emotional purchase. We are used to buying them because we fall in love with them and we can picture our kiddies frolicking on the swing set in the back yard while we care for the flowers we just planted in the front yard.

With the current investment climate I am asked often, “Sean, how low do you think my property will go?” I often respond the same. Your property value will reset to a value that is once again supported by the rental income for your neighborhood. With residential rental property, no such illusions need exist. Our personal tastes mean nothing. Don’t look for the type of place where you would want to live. That’s irrelevant now. This is nothing more than a math problem. Either the numbers work or they don’t. So if the current rents in your neighborhood are $1700 a month and your current property values are $330,000 you may lose another $100,000 in value since $1700 a month will only support $230,000 in mortgage. Understanding, that the low property may not be yours but a similar property in your neighborhood will reach that value, thus resetting the value of your property for that moment.

One of the major problems with using a standard real estate agent to help you find investment properties is that they’re programmed—just as you, the formally-traditional home buyer—to seek out the “desirable” house. That house is pretty, in good shape, has lots of amenities, and is close to schools, shopping, and public transportation. The neighborhood is quiet and the neighbors have lived there a long time; they all know one another.

What the heck does this have to do with making money in rental housing?

Here’s what I do instead. Once I have identified an area, I get a copy of the local newspaper. Sure, there is the temptation to use the Internet, and believe me, that temptation will be strong if you are trying to buy a couple of states away from where you yourself live. But I’ve found that the local paper is actually a little easier to navigate, gives me just the amount of data I want to begin with, and will often have listings

I won’t find on the ’Net, such as “For Sale By Owners.”I look through the “Rental” section first—not the “For Sale” section. I look for a 3-bed, 2-bath, 2-car garage property, preferably built within the last decade. Why do I target this type of property? Because, it makes an easy comparison, plus it makes for a good rental property. It usually attracts a strong tenant and might also make a decent property to appreciate in value over time. Furthermore, being rather new, it is more likely not to be facing major repairs and upgrades, such as a new roof or a new heating system during the time that you own it.

Older buildings are a poor market indicator because even when there is little inventory on the market, old places still take a while to move. 1950s and older construction tends to always be undesirable. It is very common for the newer

development to have no vacancies, but an older development to be giving away units with three months free rent. Your market indicator is the newer, nicer place. Post-war construction with ten by twelve rooms and one bath are difficult rental investments because even when you can rent them, they will turn over constantly. Who wants to stay in those kinds of places? Thus, you could easily find yourself stuck with long periods of vacancy, which will kill your budget.

On the other hand, in some areas the best and most plentiful, rentable, and desirable properties are newer vintage condos and “townhomes.” If so, redirect your attentions there. Just bear in mind, you have to do your homework

and factor in Common Area Maintenance fees (CAM fees). These will add to your monthly expenses and must be considered when doing cap rate analysis. Homes for sale will usually list their approximate age. Rentals rarely do. What can you do? Call them! Pretend you’re a renter and ask how old the property is. An even quicker method is if you are in an area where the local Multiple Listings Service (MLS—a co-operative of the local Realtors’ Association where all homes listed by local Realtors are put into a master database) allows “civilians” (people like you) to look up listings. MLS will almost always list the age of properties, sometimes even rentals.

Next, I flip to the For Sale section and look for the same category of house.

Then I use the “Rental Multiplier of One Hundred.” I may not know the mortgage terms I can get, but I know if the price is lower that one hundred times the rent I will cash flow with most current financing.

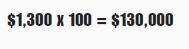

Thus, if I find that type of home for SALE for, say, $150,000, I will be looking to see if there are any rentals for that same type of home for $1,500 per month. If I can, I not only know I’m in the right state, town, and neighborhood, I know I may have even found the exact property worth purchasing.

$150,000 (purchase price) divided by one hundred = $1,500 (monthly rent)Obviously, if the monthly rent is even higher, I’m even MORE excited. And to tell you the truth, when it gets down and dirty and I’m actually ready to pull the trigger and buy a property, I’m really looking at a factor of less than one hundred, eighty five or ninety depending in the location. But that math is harder to do in your head when you’re evaluating two hundred or so properties, so I round it off to one hundred, then hope I find a number of properties that are doing a little better than that (Example: $150,000 sales price, renting for $1,525 per month).

The key here is not to just find one of anything. I’d prefer to find a number of homes for sale in that same category (three-bed, two-bath, two-car garage, recent vintage) and average out the prices. This tells me the true sales market. If I find one at $150,000, but everything else in that category seems to be up around $250,000, I must assume that one property must be unique—a real dog—what they call an “outlier” in our calculations. Yes, I might still buy it—it may be a bank-owned

foreclosure—but I still have to know for certain that I can get the kind of rent that makes my numbers sing.

From there, I hope to find, again, a number of properties in this same category renting for that “Factor of one hundred,” as well as a number that are selling and fit into that same formula correctly. If I do, I know I’m in the right market at the right time.

Now, I mentioned that I rely a lot on newspapers versus the Internet. Don’t ask me why; I have no scientific answer for this, but I always seem to find higher rents in newspapers than on Internet listings. I believe when you place a newspaper ad you have to predict what the market will bring in a week from now; conversely, the Internet you can change as often as you like. So, I believe the Internet ads tend to reduce prices quicker because of the nervousness of the landlord. The exceptions to this, of course, are the listings from a local newspaper that also has an on-line presence (which most now do). The comparison I’m drawing here is between newspapers (paper or electronic) versus large national Internet home rental sites (do a web search—there’re a lot of them out there). Why this is important is that you want an honest look at the rental market—high or low. You want reality. You plan on entering this market and you want the highest rent possible. You want to identify the property you can buy for the lowest possible price and rent for the highest possible price.

Make no assumptions! A lot of people will be so eager to enter a market that they will try to make up their own financial formulas. They’ll only find a lot of different properties with prices all over the place—a duplex here, a three-bed, two-bath with a one-car garage there, something else somewhere else, etc. From that they’ll try to conjecture things like, “Well, if a three-bed, two-bath, with a one-car garage and is forty years old rents for x, then a three-bed, two-bath, two-car recent vintage will rent for x + something.” Sorry, but it doesn’t work that way. Math is math and prognostication is prognostication. I want you to be conservative mathematicians, not

Madam Marie, the Fortuneteller.

quickly and efficiently get me down to only having to consider a handful of properties. If I can’t even find that many, I’m also being told that this is the wrong market at the wrong point in its cycle.

Despite all that I’ve proselytized about not being afraid to move outside your geographic comfort zone, I still suggest that if you are targeting multiple markets, you begin with the one closest to you, and then move outward. This is common sense. If you can buy in a market that is close enough to where you live so that you can act as your own property manager, this fact can save you some money in the long run. If you have to go visit the area from time to time, it cuts down on time and traveling costs. Pennies add up, my friends.

Also bear in mind the market factors and the ripple effects I mentioned earlier. If you are, say, looking at the greater Cleveland, Ohio, market, lay your data on maps so that you can identify the geographic area around there—perhaps a certain neighborhood or suburb—where the factors all overlay. Try this section first—it should be the place where you stand to make your most prudent investments. If you cannot find what you are looking for there, then gradually move outward from that epicenter. Let me remind you, I’m not telling you to find the geometric epicenter of a town, city, or county. I’m telling you to use the factors of shopping, transportation, employment, entertainment, schools etc. Be careful and watch for the negative stimulants and ripple blockers like railroad tracks, divided highways, and rivers that limit transportation routes from your positive stimulants.

In some cases, you may have to do an entire city or metro area in order to get to what I call my magic number—ten properties for potential purchase. That’s what I want you to refine your search to. Once you start going miles and miles away in order to accumulate ten properties worth considering for purchase, again, you are probably in the wrong market at the wrong time. But ten is what I would like you to get—ten where you have run your quickie formula and discovered that yes, you have probably found something here that will cash-flow for you.

Something I do at this point is a kind of “reconnaissance.” Now, so I don’t confuse you, I am looking to purchase properties, but I am also studying existing rental properties, to learn about the local rental climate. Sometimes people have existing rentals that they are looking to sell, but you may ask yourself this question—if they are selling a rental property, why would they do that if it was cash-flowing for them? Answer: It probably wasn’t. They may have purchased it in the prior boom, and they may be struggling to maintain the higher mortgage amount. Your job is to find out why. Are they selling for the prior reason or did they recently purchase the property, and if so, what is their experience? There could be a myriad of reasons, but existing residential rental properties on the market are rarely a good sign—unless it is someone who bought at the wrong time and is carrying a huge mortgage that their rents can no longer sustain. If they are forced into selling, and they are willing to sell to you at the price where the numbers work in your favor, then you’re where you want to be. Existing rental properties and their owners may eventually become my competition, but until they realize that, I’m going to pump the owners of those properties for information. When I see property for rent, I’ll call up and see what kind of reception I get. If they say, “Oh my God! Thank you so much for calling. Please, please, come over and see the place today. If you do, I’ll throw in the first month’s rent for free,” hang up and start looking in another market. This is bad, bad news. What you really want is someone who tells you, “Sorry, that unit is already rented.”

“But it was only listed this morning.”“Yep. That’s the way it is around here. If you see another somewhere, better call up first thing in the morning or it’ll be gone. I know some people who are going down to the local newspaper plant to get the paper the moment it comes off the press at four-thirty am just so they can beat the rush.”

If you hear that, you are in the right market at the right time—IF you can find properties to buy where the numbers jump in your favor.

Speaking of competition, just so you know—there’s a kind of “a rising tide lifts all boats” sort of situation when it comes to real estate investment. See, no one wants to own a property in the middle of an area where all the other buildings are vacant and boarded up. And no one wants to rent in an area like that, either. Real estate investment is successful due to investment volume, just like the stock market. It’s not simply a matter of one person paying a very high price for a large number of shares of stock. It’s far better if a LOT of people are buying shares at a reasonable price.

For this reason, I often go on road trips with a whole bunch of potential real estate investors all at the same time. Are they competitors of each other? Well, yes, in a sense. But envision this: We come to a city block. Fifty percent of the homes are vacant and for sale. If I have enough people in the back of my van—and I’ve been known to rent a van and cart around eight investors at a time on these road trips— to buy up all the vacant properties on that block, everyone wins. The existing owners on that block win, and my new investors who have just bought into that block win. Why? Now the entire block will be occupied. Vacancies breed crime and urban decay. Tenancy puts an end to those negative things.

So there I’ll be, driving my big ol’ van around, showing my people properties, and each will be saying, “I’ll take this one.”“Okay, then I’ll take this one.”

“This one’s got my name on it.”

And on and on. They all make their purchases at a low price because what they were buying into was a neighborhood with a fifty percent foreclosure vacancy rate. Once they close, they will be renting to people in a one hundred percent occupied neighborhood, which will obviously garner them a much better rate of rent. The owners who were there before will now have homes of greater value. Everybody wins!