Below is a list of some of the questions that are asked most frequently by our clients.

Q. Can I own more than one IUL policy?

A. Yes. Any individual can own multiple different IUL policies. And, each policy can have a different owner, insured and beneficiary. A family could have a policy for each spouse and one for each of the children, grandchildren, etc. Plus you can set up policies for your businesses as well.

Q. I’m stuck in a bad insurance policy. Can I switch over to an IUL?

A. Yes. You can easily use a 1035 exchange to do this. It allows you to move your money from your poorly performing policy to another better performing policy, while keeping your tax basis the same.

Q. Most of my retirement funds are tied up in my IRA and 401(k). Can I switch them from those programs, to and IUL?

A. Yes. It is important to keep in mind that there are different tax ramifications depending on your age and income. It’s always best to consult your tax and securities advisor prior to liquidating any qualified funds. We do have clients who are so frustrated with the performance of their current retirement programs that they are willing to take the tax hit now, to be able to sleep better at night.

Q. Can I really miss or skip premium payments and still keep my policy intact?

A. Yes. This is a BIG benefit to the IUL. When you have a properly structured policy, you have almost infinite flexibility with your annual contribution amounts. When we design your custom plan, we do analysis to determine the appropriate death benefit amount. The death benefit has two important minimum and maximum numbers. In between those numbers is the flexibility you have.

There is a minimum amount you can contribute per year. This is what the insurance company defines as the minimum amount needed to pay for their cost to insure you. The maximum amount is defined by the IRS, and it’s based on the amount of death benefit attached to your plan. We’re happy to run some analysis for you to show you what your numbers look like.

Life is full of surprises and changes, so it’s comforting to know that you have tremendous flexibility with your IUL contributions, without having to worry about negative effects to your policy.

Often, just the first few months of contributions is WELL over the minimum annual amount necessary to keep your plan active. This premium flexibility is something our clients really appreciate. Other plans require set premiums, and if they aren’t paid, it can have VERY negative effects on the policy’s performance.

Q. How safe is my money in an IUL policy?

A. As discussed earlier, we work with the highest rated Mutual Insurance companies. Most of these companies have been in business over 100 years. They have withstood the test of time, and survived and thrived. In today’s crazy financial markets, we believe these companies are among the safest companies in the world. Plus, since they are mutual companies, and not publicly owned stock companies, they are not as subject to much of the madness of Wall Street.

Q. What are the downsides to an IUL?

A. The IUL has the same downsides and risks that are associated with any retirement plan, but on a much smaller scale due to the floors, caps, and other protections that are in place. When you understand the benefits of an IUL, you’ll find that almost all the “downsides” are associated with short-term pain to receive long-term gain. IE: Short Term ‘cost of insurance’ expense, to receive long-term, tax-free income, and death benefit.

Q. Can Canadians use this same Barefoot Retirement Plan, eh?

A. Yes. Not all of the Insurance providers we work, offer policies that will work in Canada, but we do have some great providers that will.

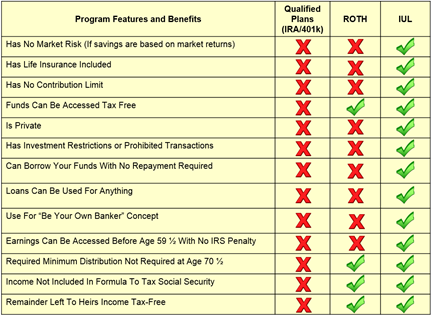

Q. How does an IUL compare overall to an IRA, 401(k) and ROTH account?

A. Good question. We thought the easiest way to show this would be in the chart below. We simply took the most important, key factors of retirement plans, and compared them all together. We think the chart speaks for itself.